10 Undervalued Stocks!

Excellent Balance Sheets Too!

Market Latest

Year to date, the S&P 500 is up 15%, although this gain is really being driven by some of the larger tech holdings, notably Nvidia which is up 156% and accounts for 6.11% of the index fund.

When you remove tech stocks from the S&P 500 you can see that the rest of the market is trading at historic lows in relation to tech.

What does this mean for us?

Well, this gives us an opportunity to look for beaten down compressed stocks that show massive signs of undervaluation whilst everyone else is chasing tech stocks that are trading at some significant valuations.

Just last week I posted on X (formerly Twitter) the below:

Now whilst you shouldn’t analyse Companies purely based off one valuation metric, I think you understand the point.

So What Should We Look For?

First, we need to identify our criteria for high quality undervalued stocks:

Net Debt to EBITDA (<1.5)

We want this to be very low (below 1.5). What this metric shows us as per below is the number of years it would take a Company to pay off all of it’s debt, net of cash on hand.

So, for example, if we see 0 it means it will not even take this Company 1 day to pay off all of their debt.

Why this is important is because it correlates to both the Balance Sheet strength and Dividend Safety of a Company.

The lower the better.

Undervaluation (per Dividend Yield Theory and on a P/E basis).

What do we mean by this?

As per the below we want Companies that have a current yield higher than the 5-Year Average as this is one undervaluation signal per DYT and to make it a double undervaluation signal, we want to see the forward P/E below the 5-Year Average.

Upside > 15%

We want Companies where Wall Street see over 15% upside over the next 12 months. Now whilst this is not an important criterion, it is reassuring to see that Wall Street see upside to Stocks we are reviewing.

These upside calculations will be coming from Wall Street analysts, so whilst we would say to take them with a pinch of salt, we will be screening for those that meet all criteria’s today as well as predicted upside of more than 15%.

Free Cash Flow Yield > 3%

Free Cash Flow (FCF) Yield ultimately shows us how much cash a Company has generated from its core operations relative to its share price.

The higher the FCF yield the lower the payback period as we can see below.

10 Undervalued Dividend Stocks

So which stocks meet these criteria?

Let’s take a look below:

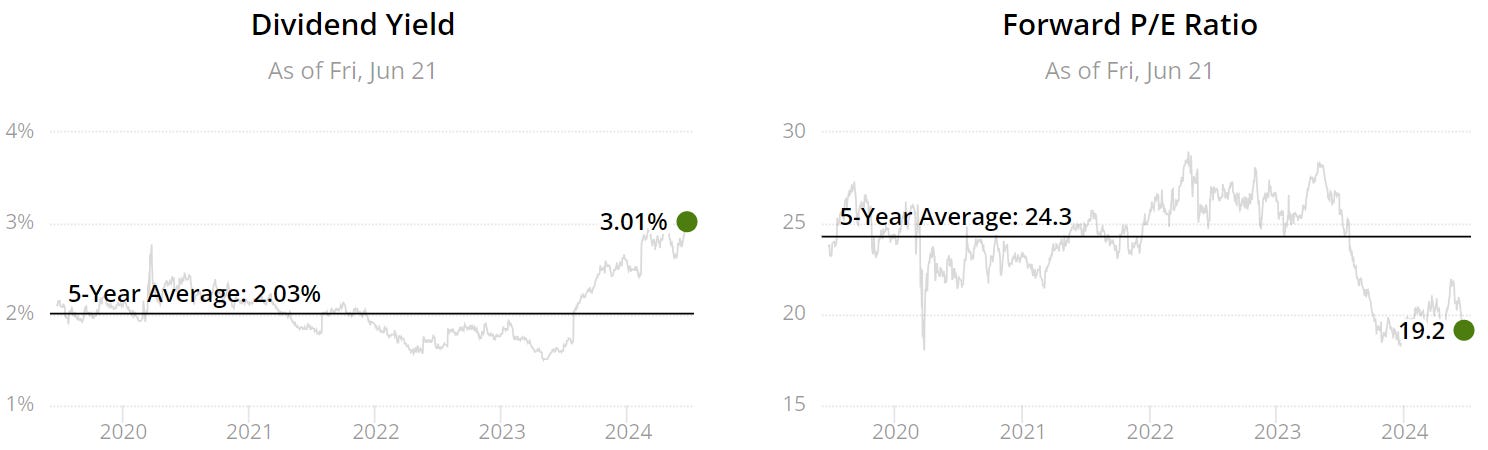

1 - Hershey (HSY)

Net Debt to EBITDA = 1.49

Undervaluation = As per graph below, undervalued on both dividend yield theory and on a forward p/e basis.

Upside > 15% = 16%

FCF Yield > 3% = 4.3%

If you want to see a deeper dive into Hershey we have covered it on our channel below:

2 - Old Dominion (ODFL)

Net Debt to EBITDA = 0

Undervaluation = As per graph below, undervalued on both dividend yield theory and on a forward p/e basis.

Upside > 15% = 20%

FCF Yield > 3% = 3.75%

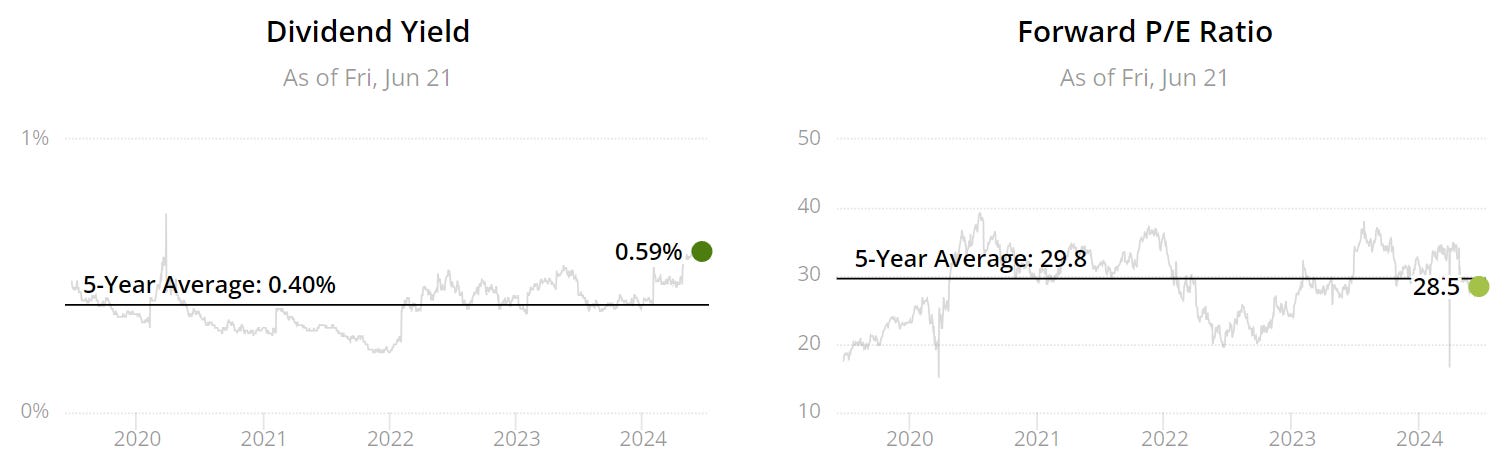

3 - Accenture (ACN)

Net Debt to EBITDA = 0

Undervaluation = As per graph below, undervalued on both dividend yield theory and on a forward p/e basis.

Upside > 15% = 16%

FCF Yield > 3% = 4.6%

4 - Sanofi (SNY)

Net Debt to EBITDA = 0.84

Undervaluation = As per graph below, undervalued on both dividend yield theory and on a forward p/e basis.

Upside > 15% = 18%

FCF Yield > 3% = 4.6%

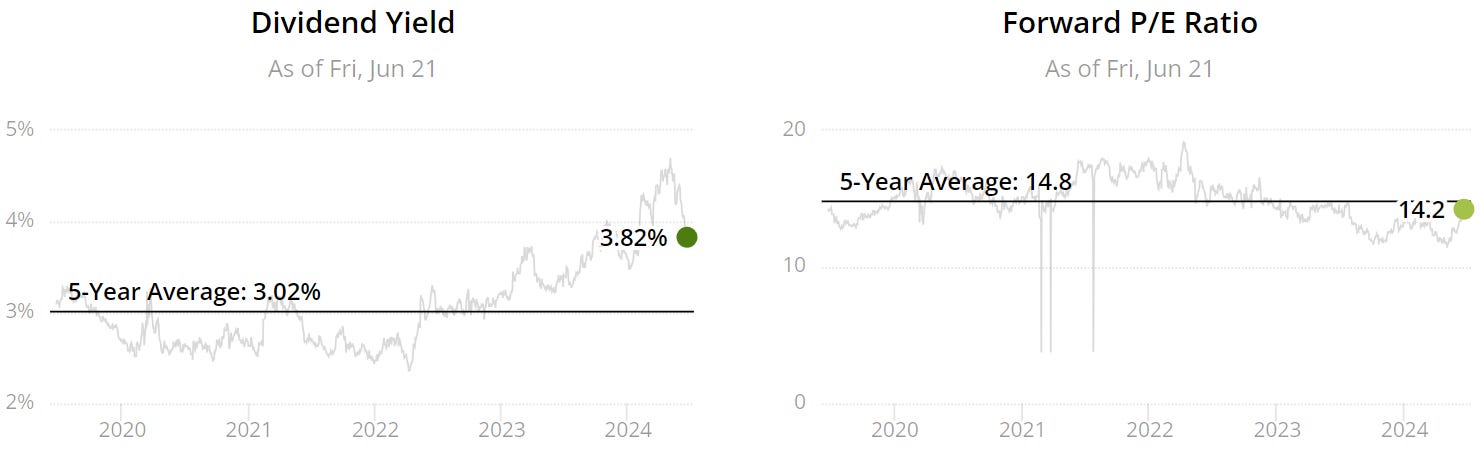

5 - Roche Holding AG (RHHBY)

Net Debt to EBITDA = 1.06

Undervaluation = As per graph below, undervalued on both dividend yield theory and on a forward p/e basis.

Upside > 15% = 16%

FCF Yield > 3% = 6.3%

6 - Visa (V)

Net Debt to EBITDA = 0.05

Undervaluation = As per graph below, undervalued on both dividend yield theory and on a forward p/e basis.

Upside > 15% = 16%

FCF Yield > 3% = 3.6%

3 weeks ago we did a deep dive on Visa below:

7 - UnitedHealth Group (UNH)

Net Debt to EBITDA = 1.00

Undervaluation = As per graph below, undervalued on both dividend yield theory and on a forward p/e basis.

Upside > 15% = 18%

FCF Yield > 3% = 4.9%

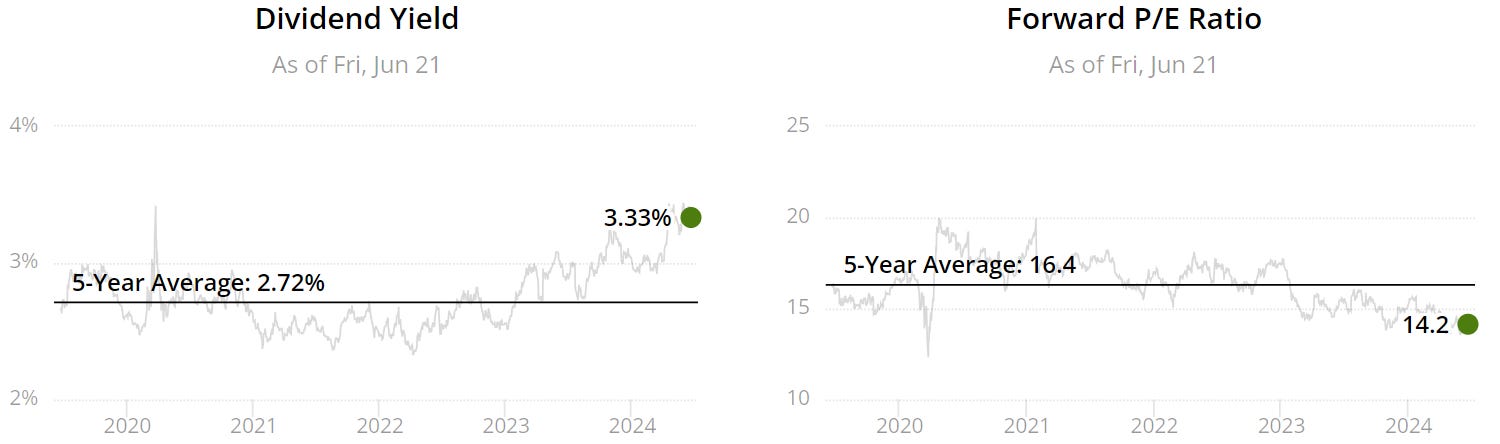

8 - Johnson & Johnson (JNJ)

Net Debt to EBITDA = 0.25

Undervaluation = As per graph below, undervalued on both dividend yield theory and on a forward p/e basis.

Upside > 15% = 19%

FCF Yield > 3% = 4.89%

9 - Cisco Systems (CSCO)

Net Debt to EBITDA = 0.00

Undervaluation = As per graph below, undervalued on both dividend yield theory and on a forward p/e basis.

Upside > 15% = 16%

FCF Yield > 3% = 7.2%

10 - Nike (NKE)

Net Debt to EBITDA = 0.19

Undervaluation = As per graph below, undervalued on both dividend yield theory and on a forward p/e basis.

Upside > 15% = 16%

FCF Yield > 3% = 4.3%

Latest YouTube Videos!

Over the last week we have covered a few videos looking at undervalued dividend stocks as per below:

6 Undervalued Dividend Stocks At 52 Week Lows:

4 Dividend Stocks At 52 Week Lows That No One Is Talking About:

Massive Insider Buying With These 5 Stocks:

If you are interested in valuing stocks yourself we have created a valuation model below which you can pick up:

Conclusion

Whilst we have ran through these dividend stocks which meet our high quality criteria including dividend yield theory, you should always do your own due diligence.

This can however be used as an initial starting point for identifying stocks that could be undervalued.

Happy to hear your thoughts too.

Thanks For Reading!

If you’d like to support this work feel free to buy me a coffee. The proceeds will contribute to the running costs of the newsletter.

Join the community of investors - subscribe now to receive the latest content straight to your inbox each week and never miss out on valuable investment insights.

If you found today’s newsletter helpful, please consider sharing it with your friends and colleagues on social media or via email. Your support helps to continue to provide this newsletter for FREE!

Note

I am not a financial advisor or licensed professional. Nothing I say or produce anywhere, should be considered as advice. All content is for educational purposes only. I am not responsible for any financial losses or gains. Invest and trade at your own risk.