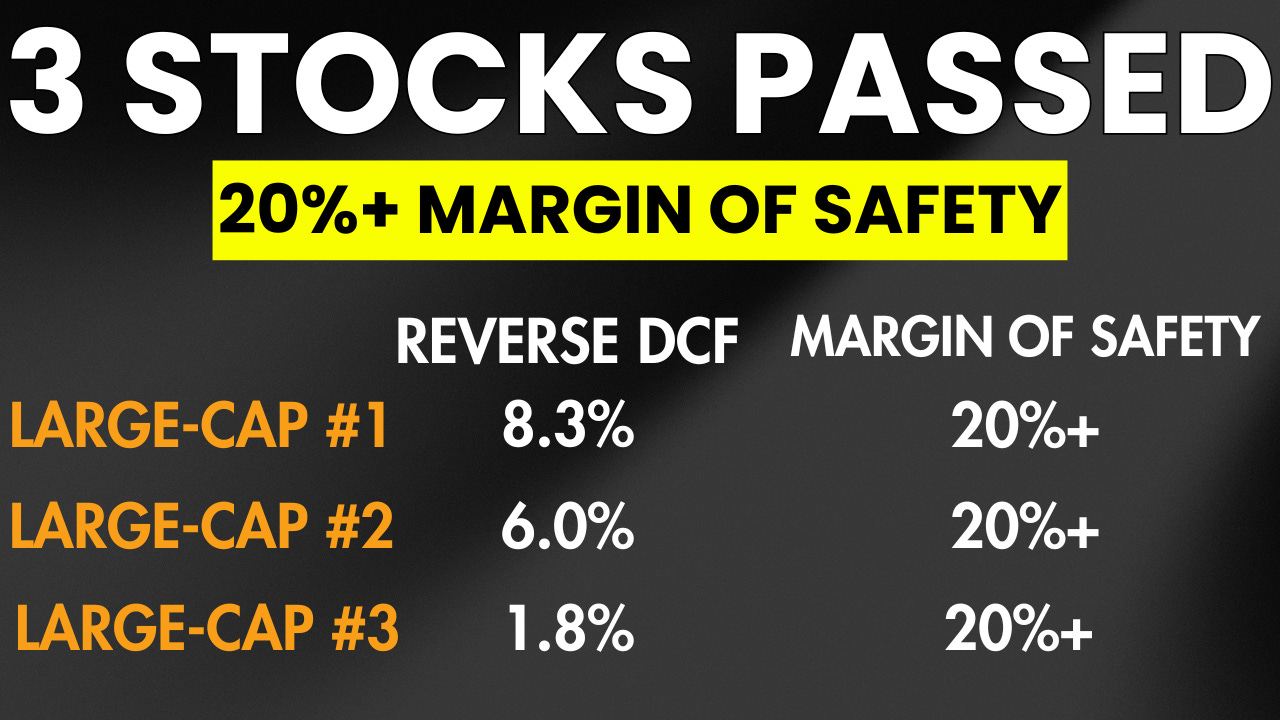

3 High-Quality Stocks at 52-Week Lows That Cleared My 20% Margin of Safety Filter

Not every 52-week low is a buy. These three passed my valuation model. Two didn’t.

The market doesn’t reward bravery.

It rewards discipline.

Over the past few months, several high-quality large caps have quietly drifted toward 52-week lows. When that happens, most investors assume opportunity.

But price alone isn’t opportunity.

Sometimes a 52-week low is a gift.

Sometimes it’s a warning.

This week, I ran five widely followed large-cap names through my discounted cash flow framework.

Three cleared my 20%+ margin of safety requirement.

Two failed - despite looking “cheap” on the surface.

Here’s what the numbers actually say.

Why 52-Week Lows Can Be Dangerous

A stock hitting a 52-week low tells you one thing:

Sentiment is weak.

It tells you nothing about intrinsic value.

To qualify as a buy in my framework, a stock must:

• Trade at least 20% below conservative intrinsic value

• Show forward P/E compression vs its 5-year average

• Have implied growth expectations below historical compounding

• Show no structural business deterioration

This week, three names passed.

Let’s start with the first.

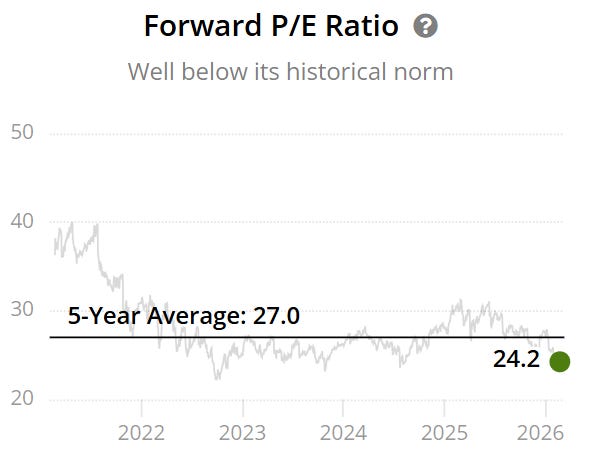

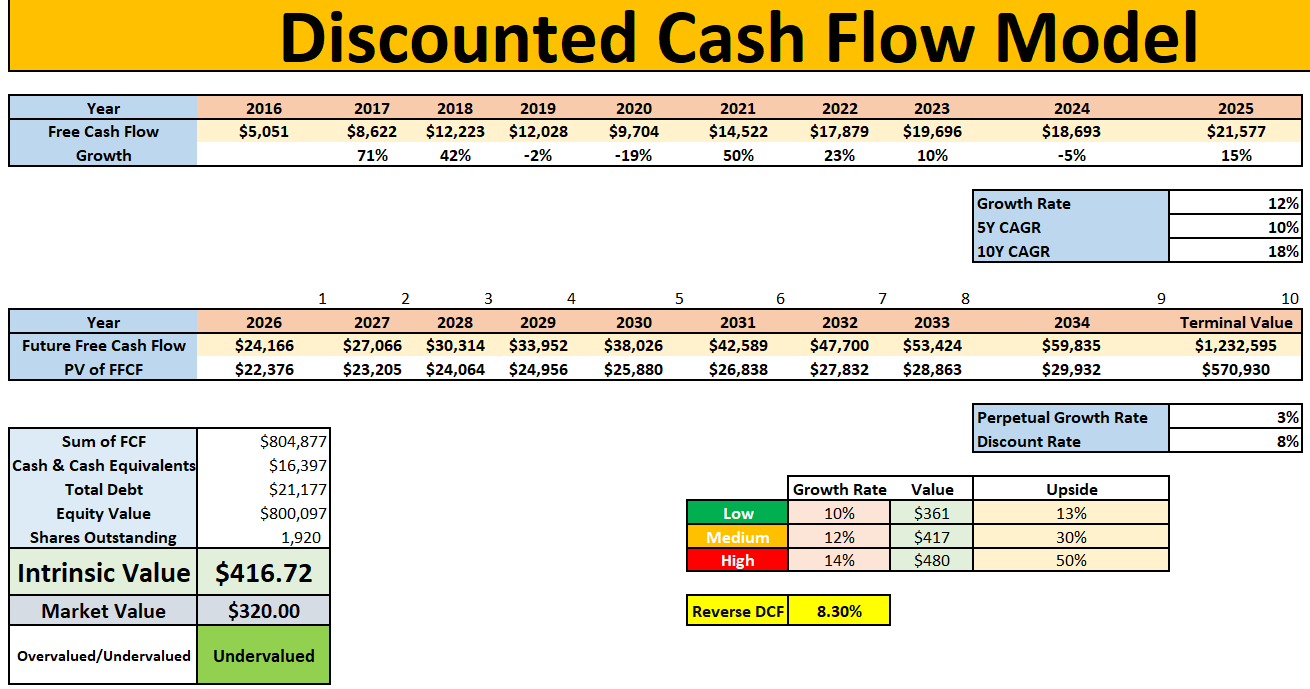

1️⃣ Visa (V)

Current Price: $320

Reverse DCF Implied Growth: 8.3%

5Y FCF CAGR: 10%

10Y FCF CAGR: 18%

Forward P/E: 24

5Y Avg Forward P/E: 27

The market is currently pricing Visa as if it will grow free cash flow at roughly 8% long term.

That’s below its 5-year history.

Well below its 10-year compounding rate.

Meanwhile, the forward multiple sits below its historical average - despite no structural damage to the business.

Intrinsic Value Sensitivity

10% growth → $361 (13% upside)

12% growth → $417 (30% upside)

14% growth → $480 (50% upside)

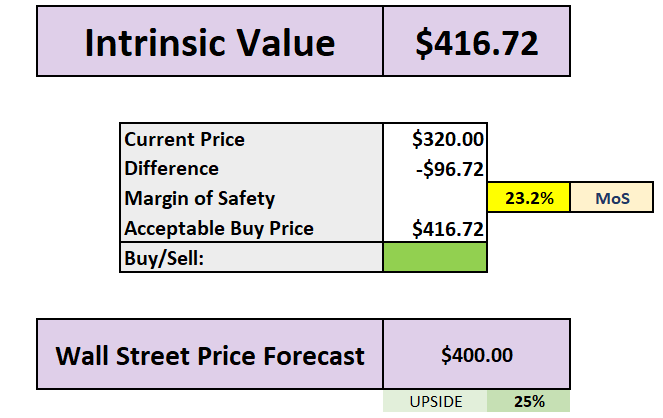

Under a conservative 12% base case, intrinsic value is ~$417.

That implies ~30% upside from current levels.

Visa cleared my 20% margin of safety threshold.

Model Status: BUY

🔒 Before continuing:

Starting March 1st, annual membership will increase from £120 to £200.

Over the coming months, I’ll be expanding the depth of each report - including:

• Full DCF models for every highlighted stock

• Reverse DCF expectation analysis

• Bear / base / bull scenario modeling

• Probability-weighted return frameworks

• More detailed downside sensitivity work

If you’re already a member, your rate remains locked in.

If you’ve been considering upgrading, you can secure the current £120/year pricing before March 1st.

The full breakdown continues below.