3 Stocks to Buy Before the Fed Cuts Rates

Powell’s Jackson Hole speech hints at lower rates ahead—here’s how to position your portfolio before the market moves.

Market Update

Markets got a boost on Friday after Fed Chair Jerome Powell spoke at the Jackson Hole symposium, nudging the S&P 500 into a small weekly gain.

But behind the headlines, there was a subtle shuffle: mega-cap tech lagged, while value and cyclical stocks finally caught up.

At the Fed’s Jackson Hole symposium on Friday, Chair Powell hinted that upcoming data could lead to a change in interest rates.

While the Fed is still watching for inflation, it’s also wary that the labour market could weaken quickly. Markets seemed to take comfort in the idea that rates might be heading lower.

Last week, big retailers like Walmart, Target, and Home Depot reported earnings.

The message? Consumers are still spending - especially on value and discount items - even with tariffs and economic uncertainty looming.

Winners and Losers This Week

Top performers:

Analog Devices (+9%)

Caterpillar (+7%)

Texas Instruments (+6%)

Bank of America (+5%)

Uber (+5%)

Biggest drops:

Palantir (-10%)

Intuit (-8%)

CSX (-5%)

AMD (-5%)

Oracle (-5%)

Notable News

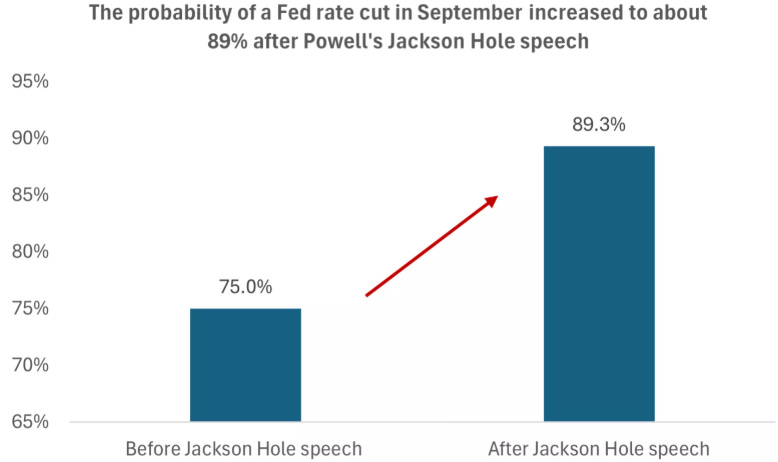

September rate cut inbound?

Powell’s speech gave both stocks and bonds a lift.

The S&P 500 jumped over 1.5%, led by sectors sensitive to interest rates - consumer discretionary, industrials, and real estate.

Bond yields fell too, easing borrowing costs for consumers and businesses.

The odds of a September rate cut climbed from roughly 75% to 89%, and markets are now pricing in two cuts this year, in September and December - a scenario that feels like a reasonable baseline.

Retail earnings show a resilient consumer

This past week, investors also digested earnings from major retailers.

Walmart and Target beat expectations, even amid tariff concerns and worries that consumers might pull back.

Amazon saw strong 11% growth in North American retail sales for Q2, while Home Depot and Lowe’s confirmed that shoppers are still spending on small home -improvement projects.

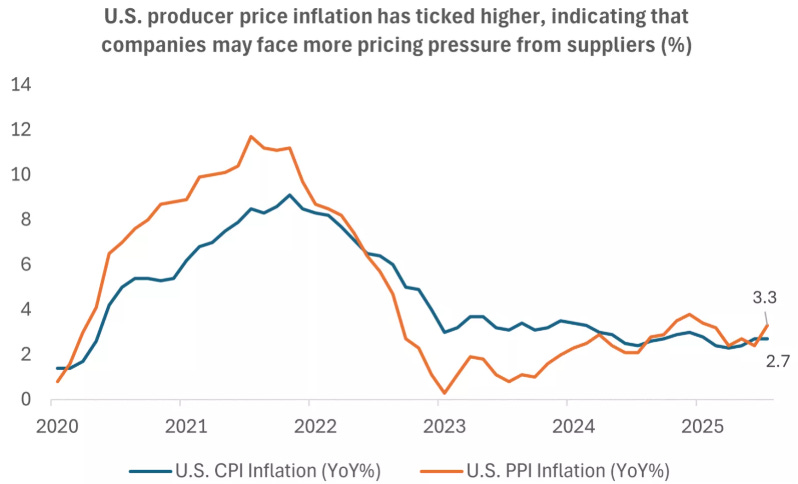

On tariffs, Walmart absorbed price increases on lower-ticket items but passed some costs onto higher-margin products, signaling that costs will gradually rise as inventory replenishes.

This mirrors the Fed’s caution on near-term inflation.

Overall, the picture points to a U.S. consumer holding strong for now. Retailers are navigating higher costs by absorbing some, diversifying supply chains, and passing others onto suppliers.

While prices for goods may trend higher in the months ahead, these look likely to be one-time bumps rather than ongoing inflationary pressure.

Shift by the Fed?

Fed Chair Jerome Powell delivered his annual speech at Jackson Hole on Friday, hinting that the Fed might adjust its policy rate from 4.25–4.5%.

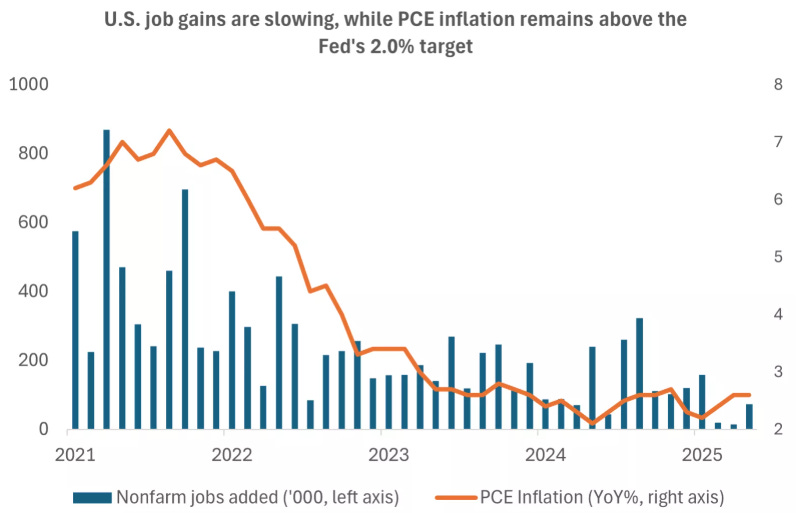

He acknowledged the tricky balancing act: inflation could rise in the months ahead, while the labour market is showing early signs of cooling.

Powell described inflation as possibly a short-lived bump, especially if tariffs don’t keep climbing.

On jobs, he noted a “curious balance”: demand and supply of labour are softening, keeping unemployment at 4.2%, but downside risks are growing and could hit quickly.

This tension underlines why the Fed might start moving rates lower.

Earnings This Week

Join 109,000+ investors on YouTube! 🎥

We break down earnings, market moves, and exclusive insights you won’t find anywhere else.

Don’t miss out — hit the button below to watch and subscribe now! 👇

YouTube Channel 🔔

Subscribe today and stay ahead of the market!

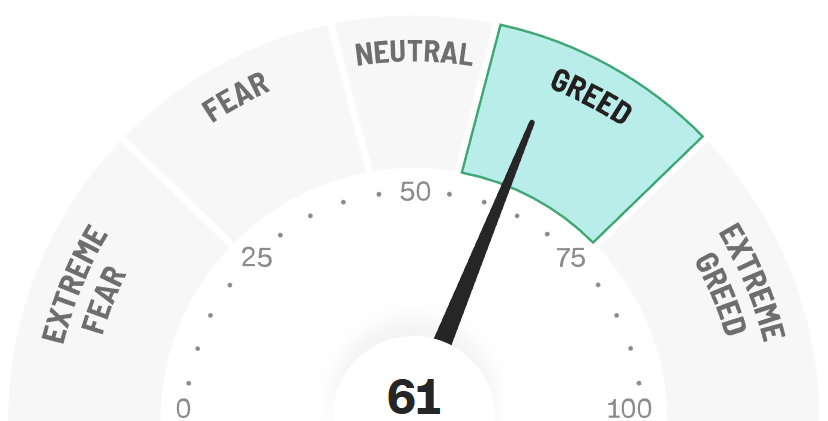

Fear & Greed Index

3 Stocks to Buy Before Rate Cuts

As the Fed signals potential rate cuts ahead, certain sectors are poised to benefit more than others - and REITs (real estate investment trusts) are near the top of that list.

When interest rates fall, borrowing costs for property owners drop, making it cheaper to finance new projects and refinance existing debt.

At the same time, lower rates often make REIT dividends more attractive compared with bonds, drawing in more investor demand.

This combination of lower financing costs and higher relative yields tends to lift REIT share prices when rate cuts are on the horizon.

That’s why, as we look at positioning portfolios ahead of potential Fed moves, including select REITs makes strategic sense. In addition, other sectors sensitive to interest rates - like consumer discretionary and industrials - can also see upside as lower rates support spending and investment.

By focusing on these opportunities now, investors have a chance to capture early gains before the broader market fully reacts to lower interest rates.

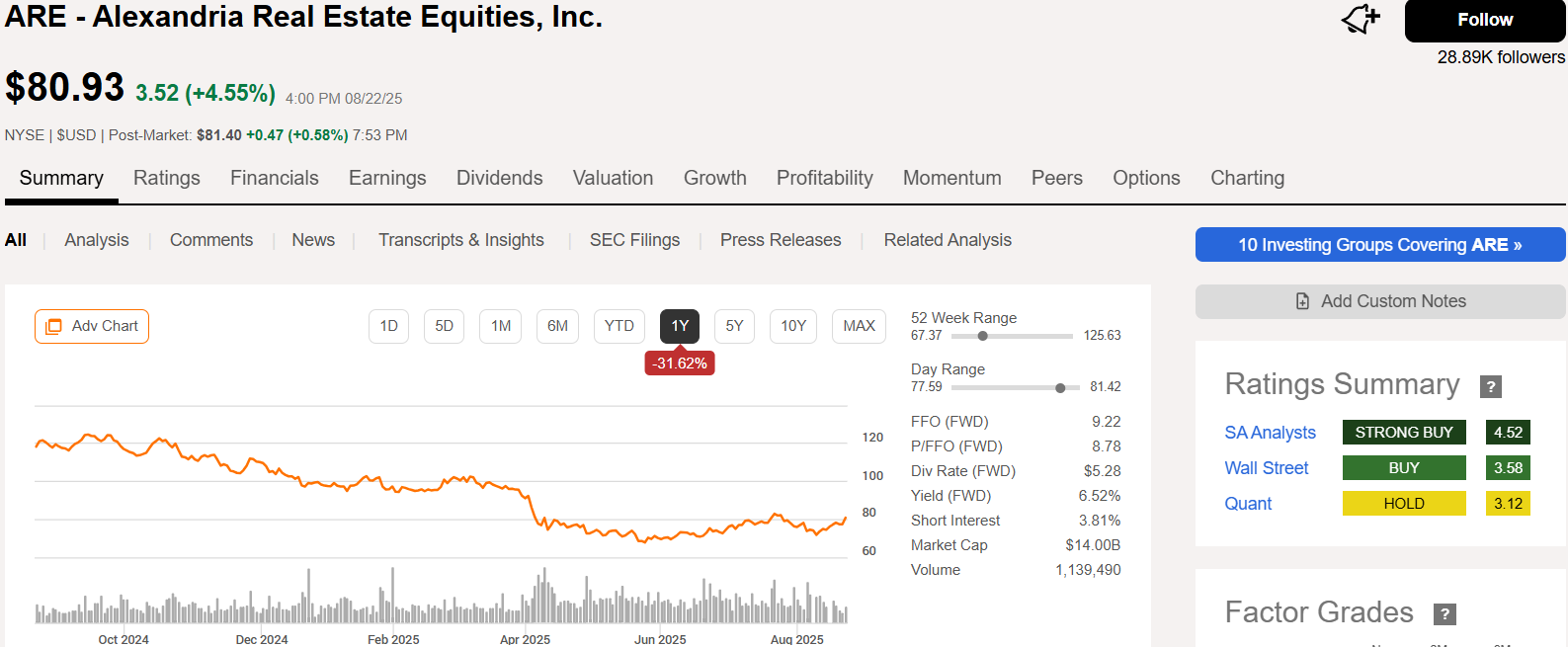

1. Alexandria Real Estate Equities (ARE)

Alexandria is a REIT focused on life sciences and biotech office and lab spaces -essentially the backbone of innovation hubs in cities like Boston, San Francisco, and San Diego.

Why Alexandria Has Been Down - and Why It Could Bounce Back

Alexandria Real Estate Equities has seen its share price fall about 32% over the past year, and several factors explain the decline. Its focus on life sciences and biotech properties, while a long-term strength, also exposes it to sector-specific risks - like regulatory shifts or funding slowdowns for startups- that can affect tenant demand.

Broader market volatility has also weighed on REITs, with investors adjusting to economic uncertainties and shifting interest rate expectations. REITs are especially sensitive to rates: higher rates can hurt valuations, while lower rates, like the ones the Fed may soon deliver, can give them a boost.

Despite the pullback, Alexandria remains a leader in life sciences real estate, with long-term leases in high-demand innovation hubs and a resilient income stream. If the Fed moves to cut rates, ARE could be well-positioned for a rebound, making now a potentially attractive entry point -but investors should be aware of the sector-specific risks and market volatility that remain.

Why Alexandria Could Be One of the Best REITs to Buy

Alexandria stands out in the REIT space for a few key reasons.

First, it specialises in life sciences and biotech properties - an area with high demand and limited supply. These tenants often sign long-term leases, providing stable, predictable cash flow that can weather market swings better than traditional office or retail REITs.

Second, Alexandria’s focus on innovation hubs means its properties are in prime locations where companies can’t easily relocate. When interest rates fall, financing costs for both Alexandria and its tenants decrease, making it cheaper to expand lab and office space - potentially boosting occupancy and rental income.

Finally, Alexandria offers a compelling dividend compared with traditional fixed-income options. As rates trend lower, its yield becomes even more attractive, drawing income-focused investors. Taken together, these factors make ARE a strong candidate for investors looking to position themselves ahead of potential Fed rate cuts.

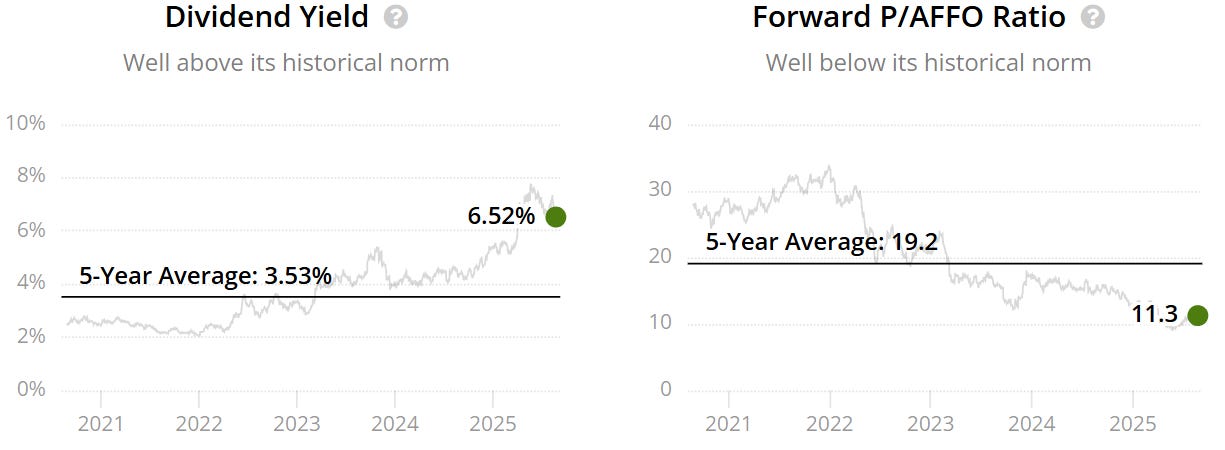

Valuation

It currently trades at a Forward P/AFFO of 11.3x vs it’s historical 19.2x, whilst also offering a yield of 6.52% vs historical 3.53%.

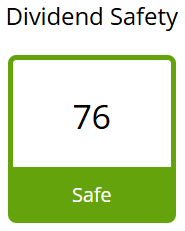

The high yield also comes with a safe dividend score.

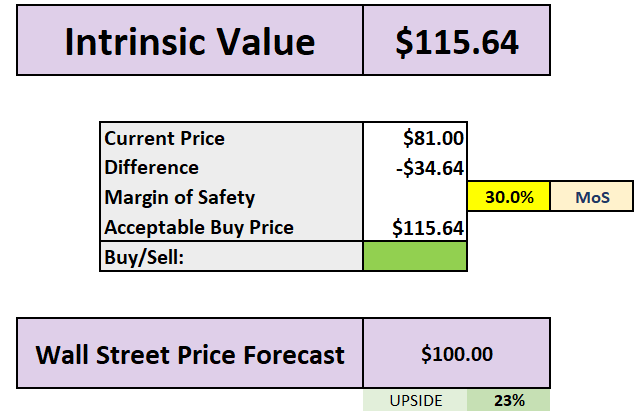

Our valuation model brings the intrinsic value to $116 giving a 30% margin of safety, with Wall Street seeing this at $100 into 2026.

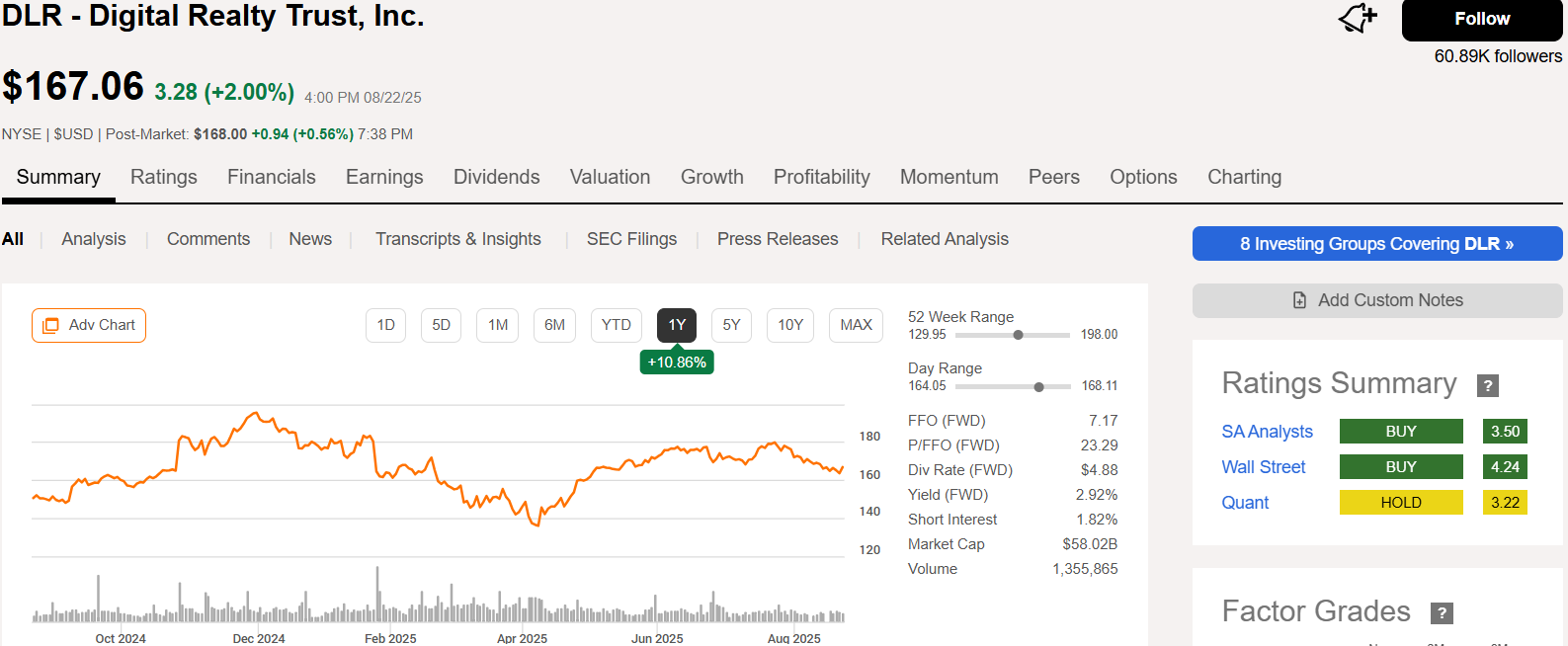

2. Digital Realty Trust (DLR)

Digital Realty is a leading data center REIT, providing the backbone for cloud computing, digital infrastructure, and enterprise IT.

As businesses continue to migrate workloads to the cloud, demand for high-quality data center space remains strong.

Why Digital Realty Has Lagged - and Why It Could Outperform

DLR has slightly underperformed the S&P 500 over the past year, and a few factors help explain why.

Rising interest rates earlier in the cycle put pressure on all REITs, as higher borrowing costs can weigh on valuations and slow expansion plans.

In addition, concerns about tech spending and a potential slowdown in enterprise IT budgets created uncertainty around demand for data center space.

That said, the long-term fundamentals for DLR remain strong. The shift to cloud computing and digital infrastructure continues unabated, driving steady demand for high-quality data centers.

With the Fed signaling potential rate cuts ahead, borrowing costs for expansion and acquisitions could drop, while DLR’s dividend becomes increasingly attractive relative to bonds.

Combined, these factors position Digital Realty to potentially outperform the broader market as interest rates ease and investor focus returns to growth and yield fundamentals.

Why Digital Realty Could Be One of the Best REITs to Buy

Digital Realty stands out for its focus on data centers - a sector that continues to see robust, long-term demand as businesses move more workloads to the cloud. Unlike traditional office or retail REITs, its tenants often have long-term contracts, providing predictable and stable cash flow even during economic uncertainty.

Lower interest rates would be an additional tailwind, reducing borrowing costs for both Digital Realty and its tenants, and making its dividend yield more attractive relative to bonds. Furthermore, the company’s global footprint in key tech hubs positions it to capture growth from the ongoing digital transformation across industries.

Of course, investors should be mindful of potential challenges, such as slower enterprise IT spending or competition from newer data center developers. Still, with strong fundamentals, predictable cash flow, and a favorable interest-rate environment on the horizon, Digital Realty is well-positioned to be one of the best REITs to consider ahead of potential Fed rate cuts.

Valuation

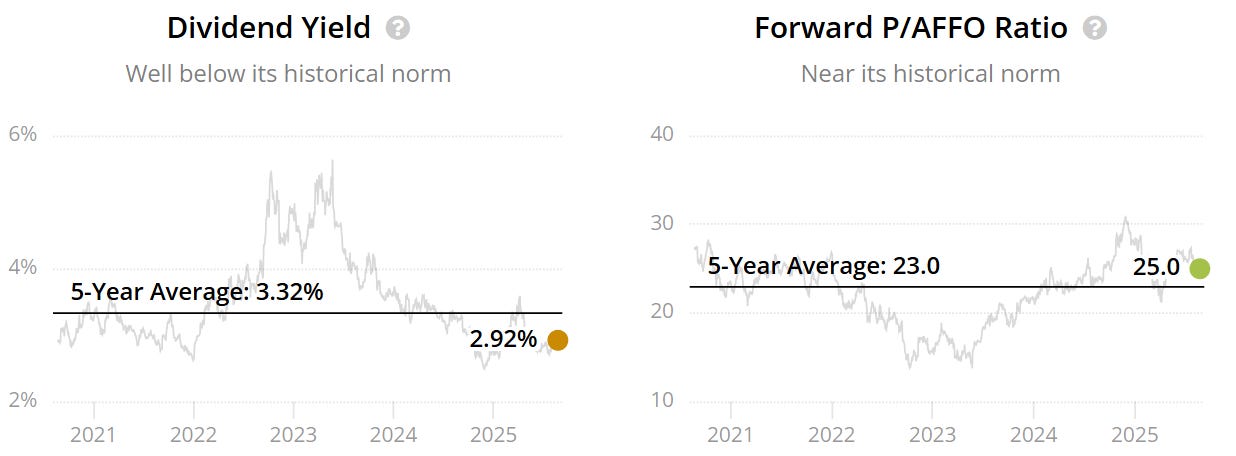

It currently trades at a Forward P/AFFO of 25x vs it’s historical 23x, whilst also offering a yield of 2.92% vs historical 3.32%.

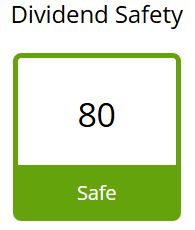

The near 3% yield also comes with a safe dividend score.

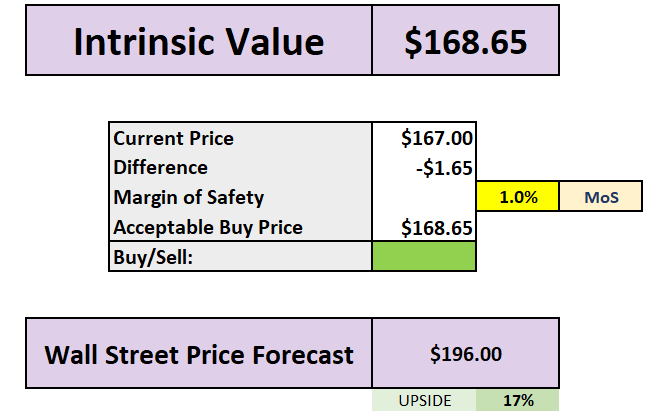

Our valuation model brings the intrinsic value to $169 highlighting we see it trading around fair value, with Wall Street seeing this at $196 into 2026.

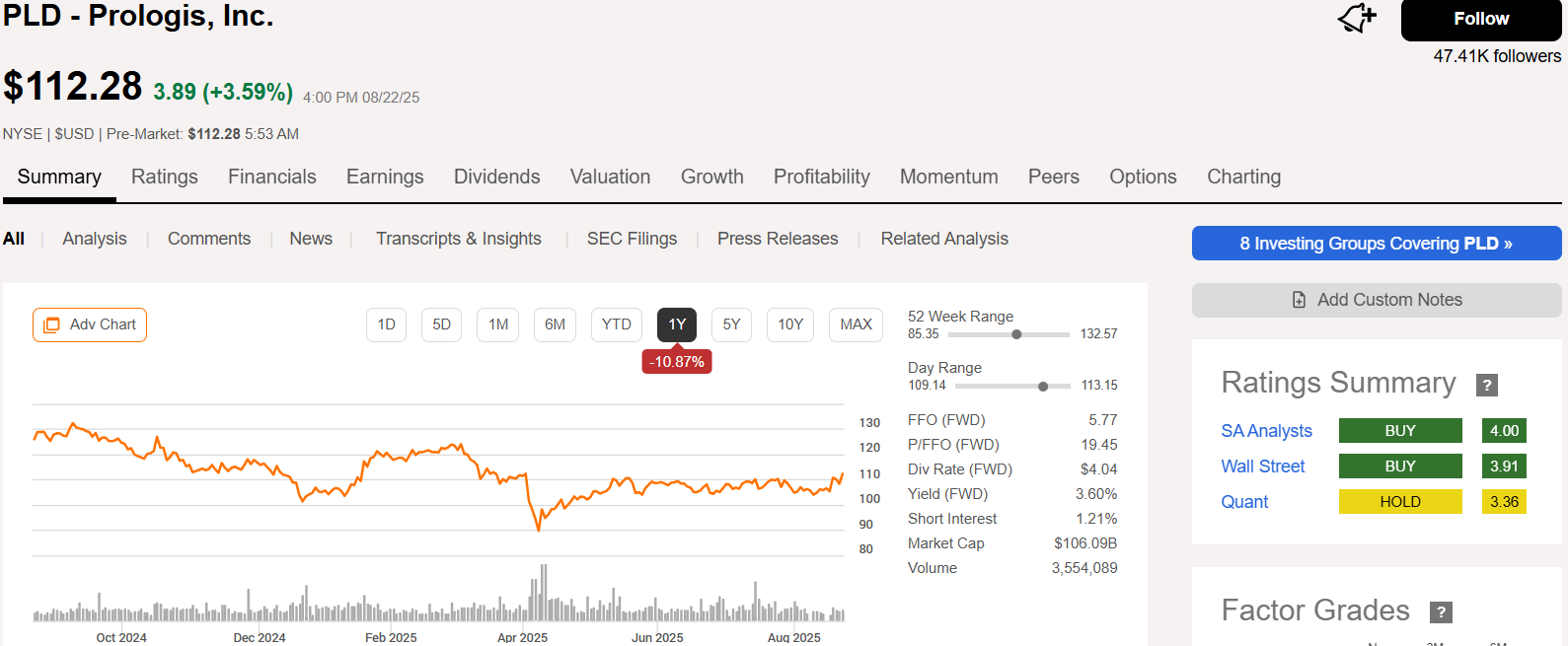

3. Prologis (PLD)

Prologis is the world’s largest logistics and industrial REIT, specialising in warehouses and distribution centers that power e-commerce and global supply chains.

As online shopping continues to grow, demand for modern logistics space remains strong.

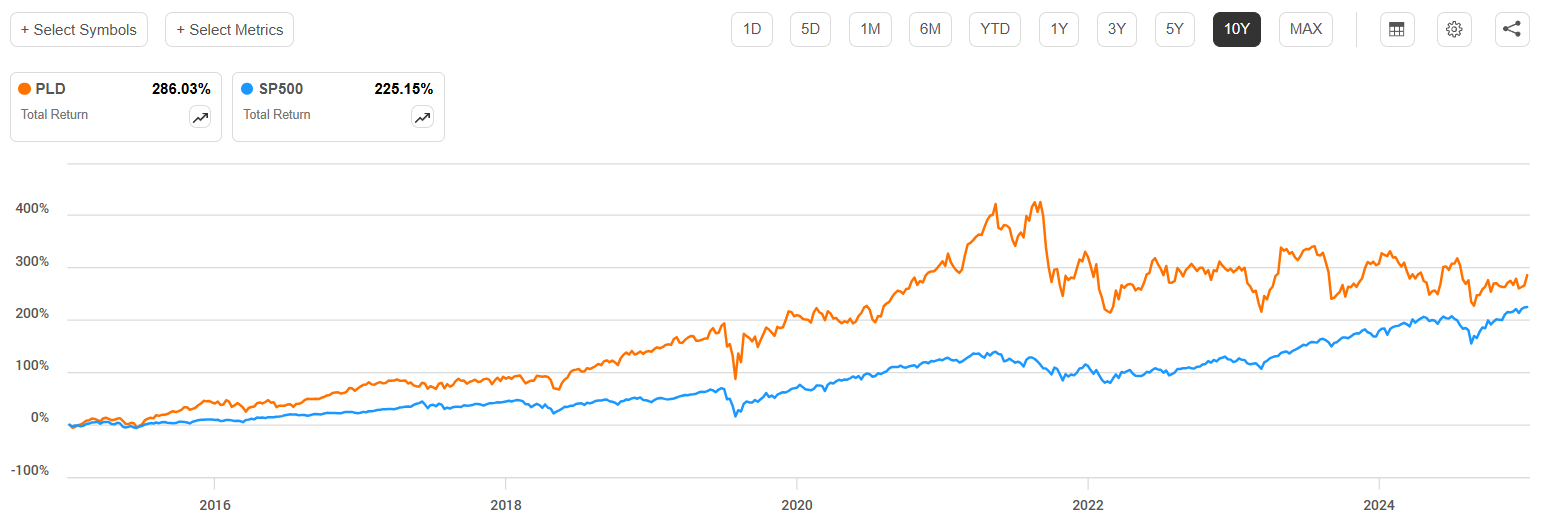

Why Prologis Has Outperformed - and Why It Could Keep Going

Over the past decade, Prologis has consistently outperformed the S&P 500, driven by the unstoppable growth of e-commerce and global logistics. Its focus on high-quality warehouses and distribution centers in prime locations has allowed it to capture long-term leases with reliable tenants, creating steady and growing cash flow even during economic swings.

Looking ahead, the trends that fueled this outperformance aren’t slowing down. Online shopping, supply chain modernization, and global trade continue to drive demand for modern logistics space. Coupled with potential Fed rate cuts, which could lower borrowing costs and make its dividend more attractive, Prologis is well-positioned to keep delivering strong returns relative to the broader market.

That said, investors should remain aware of potential challenges, including economic slowdowns that could impact leasing activity and rising construction costs. Even so, the company’s scale, quality of assets, and structural tailwinds give it a compelling edge for long-term growth.

Why Prologis Could Be One of the Best REITs to Buy

Prologis stands out in the REIT world for several reasons. As the global leader in logistics and industrial real estate, it owns modern warehouses and distribution centers that power e-commerce and supply chains worldwide - sectors with durable, long-term growth. Its tenants often sign long-term leases, providing predictable cash flow even during economic uncertainty.

Lower interest rates would be another tailwind, reducing Prologis’ borrowing costs and making its dividend yield increasingly attractive relative to bonds. On top of that, ongoing trends in online shopping, supply chain modernization, and global trade provide structural support for rental growth and occupancy.

Of course, no investment is without risks. Slower economic growth or rising construction costs could weigh on results. But Prologis’ scale, high-quality assets, and exposure to structural growth trends make it a compelling candidate for investors looking to position themselves ahead of potential Fed rate cuts.

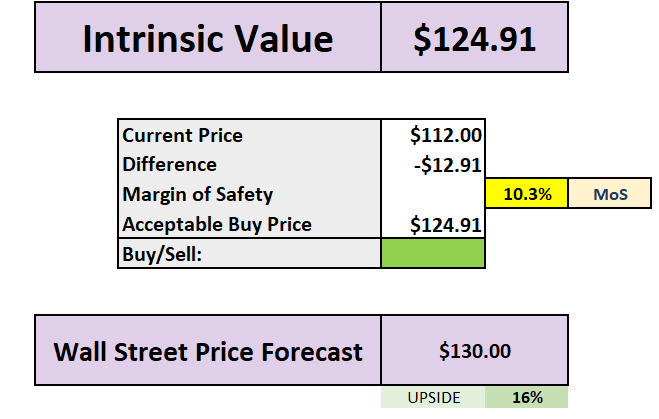

Valuation

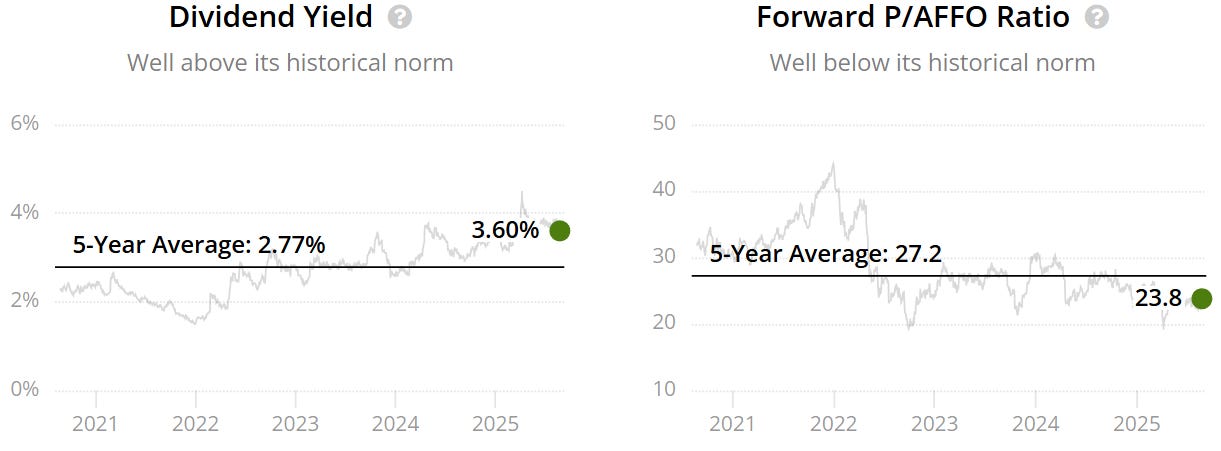

It currently trades at a Forward P/AFFO of 23.8x vs it’s historical 27.2x, whilst also offering a yield of 3.6% vs historical 2.77%.

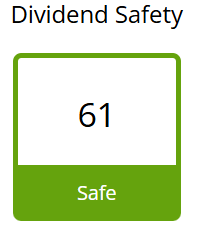

Dividend also looks to be safe.

Our valuation model brings the intrinsic value to $125, giving us a margin of safety of 10%, with Wall Street seeing this at $130 into 2026.

Stock Resources

Stock Valuation Model 📊 (Unlock my stock valuation model as seen on YouTube)

Seeking Alpha 💵 ($30 off stock research tools I use daily.)

TipRanks 📈 (40% off expert stock research tools)

YouTube 🎥 (Join 109,000+ investors on YouTube!)

Patreon 👥 (Join my community for exclusive content)

Snowball Analytic (30% off portfolio tracker)

I hope you all have a great week ahead! 🌟

Dividend Talks💰

Note:

I’m not a financial advisor. All content is for educational purposes only. Invest and trade at your own risk—I'm not responsible for any financial outcomes.