5 Bargain Stocks Near 52-Week Lows

These high-quality businesses have been repriced hard — and a few now look far more attractive than the market seems to realise.

Most stocks trading near 52-week lows are not bargains.

They are there for a reason.

Sometimes that reason is slowing growth.

Sometimes it is deteriorating fundamentals.

Sometimes the market is simply correcting a valuation that had drifted too far from reality.

That is what makes this part of the market so dangerous.

But it is also what makes it interesting.

Because every now and then, fear does not just hit weak businesses.

It hits strong ones too.

Market Update

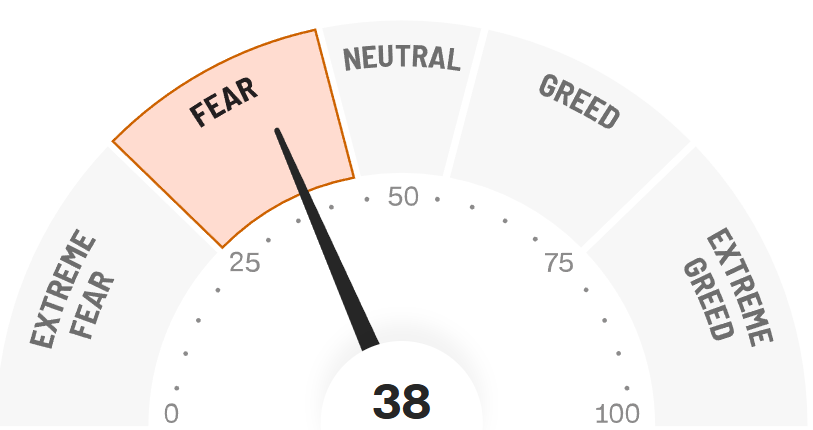

The past few weeks have been a reminder that this market is still being driven as much by fear as by fundamentals.

Last 30 days S&P 500 Heatmap

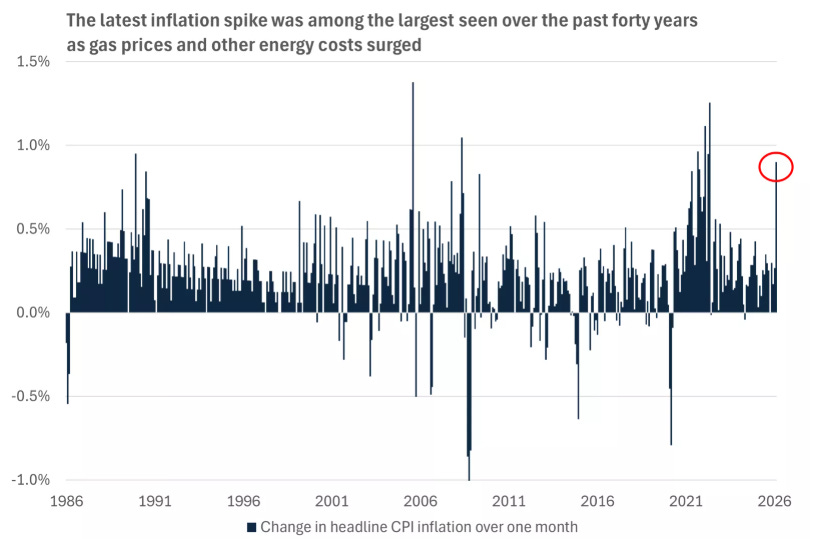

What started as a geopolitical shock quickly spilled into everything else. Oil surged as tensions in the Middle East escalated and investors rushed to price in the risk of a wider disruption.

That immediately brought inflation back into focus:

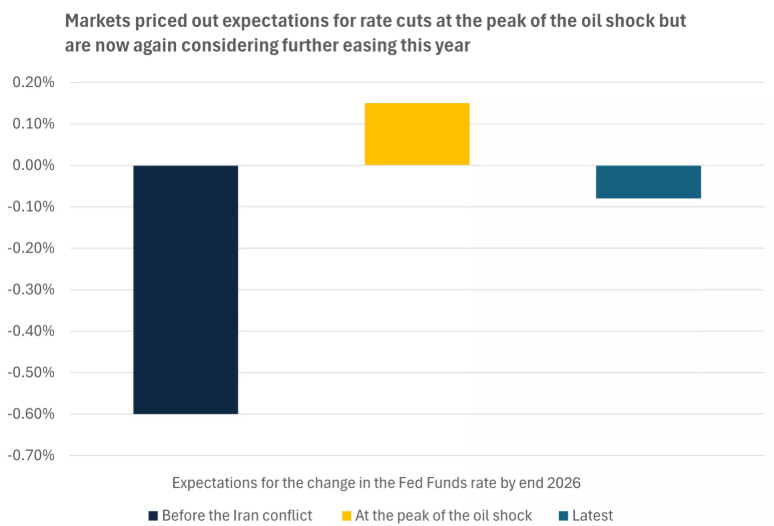

…pushed rate-cut expectations around:

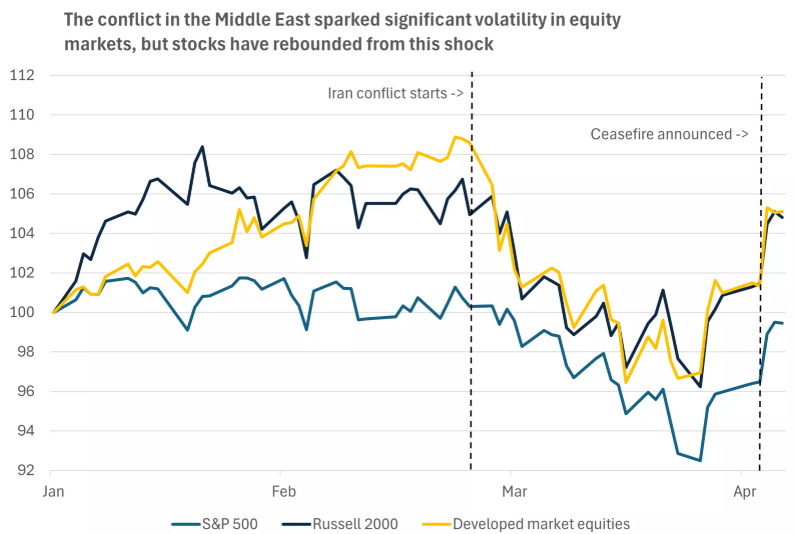

….and created another burst of volatility across equities.

Since then, sentiment has improved.

Signs of de-escalation and ceasefire hopes have helped cool some of the panic. Oil has come off its highs, markets have bounced, and investors have started to price out the worst-case scenario. But while the headlines have become less severe, the reset in valuations has already happened.

And that is the part that matters.

When markets go through this kind of repricing, they do not always separate weak businesses from strong ones very well. In the short term, premium multiples get compressed, quality gets sold alongside everything else, and stocks that looked untouchably expensive a few months ago can suddenly start to look much more reasonable.

That does not mean every stock near a 52-week low is worth buying.

Far from it.

In many cases, the market is correctly identifying a weaker business, a fading growth story, or a stock that simply never deserved the valuation it once had.

But every now and then, macro fear creates a different kind of setup.

Not in broken businesses.

In strong ones.

That is the focus of this article.

The question is not which stocks are down.

Plenty of stocks are down.

The real question is:

Which high-quality businesses are now trading near 52-week lows for reasons that matter less over the long term than the market currently believes?

And with earnings season starting to build again, this is exactly the kind of setup worth paying attention to.

What I Looked For

I was not looking for the ugliest charts or the biggest drawdowns.

I was looking for something much more specific:

High-quality businesses with durable competitive advantages

Stocks near 52-week lows after a meaningful valuation reset

Setups where the long-term thesis still looks intact, even if short-term sentiment has clearly weakened

In other words, I was not trying to find broken companies.

I was trying to find strong companies that the market has become much less willing to pay up for.

That distinction matters.

Because a stock can be down for good reason.

And a stock can be near its lows without offering any real margin of safety at all.

The opportunity only starts to become interesting when three things happen at once:

The business remains strong

Expectations come down

The starting valuation improves enough to lift forward returns

That is where selective buying starts to make sense.

And that is also why this is not really a screen for “cheap stocks.”

It is a screen for premium businesses with lower expectations.

Some of the names below are not screaming bargains.

Some are closer to fair value than deep value.

But all five, in my view, have become more interesting because the market is no longer pricing them with the same confidence it was just a few months ago.

Below are the 5 bargain stocks near 52-week lows that stand out most to me right now.

1. S&P Global (SPGI)

What S&P Global Actually Does

S&P Global is one of those businesses that looks simple on the surface, but becomes much more powerful the closer you look.

Most investors know the company for its credit ratings business. That alone is a major franchise. Through S&P Global Ratings, the company plays a central role in global debt markets, helping issuers access capital and giving investors a standardized view of credit risk.

But S&P Global is much more than a ratings agency.

The business also owns leading positions in market data, benchmarks, index licensing, and analytics. That includes well-known assets tied to the S&P 500, commodity and mobility data, and a broader ecosystem of financial intelligence tools used across capital markets.

In other words, this is not a cyclical commodity business or a disposable software tool.

It is a deeply embedded information business with recurring revenues, strong pricing power, high margins, and an increasingly important role in how global markets function.

That is why it has historically commanded a premium valuation.

And also why it becomes interesting when that premium starts to compress.

Why SPGI Has Struggled and Is Sitting Near a 52-Week Low

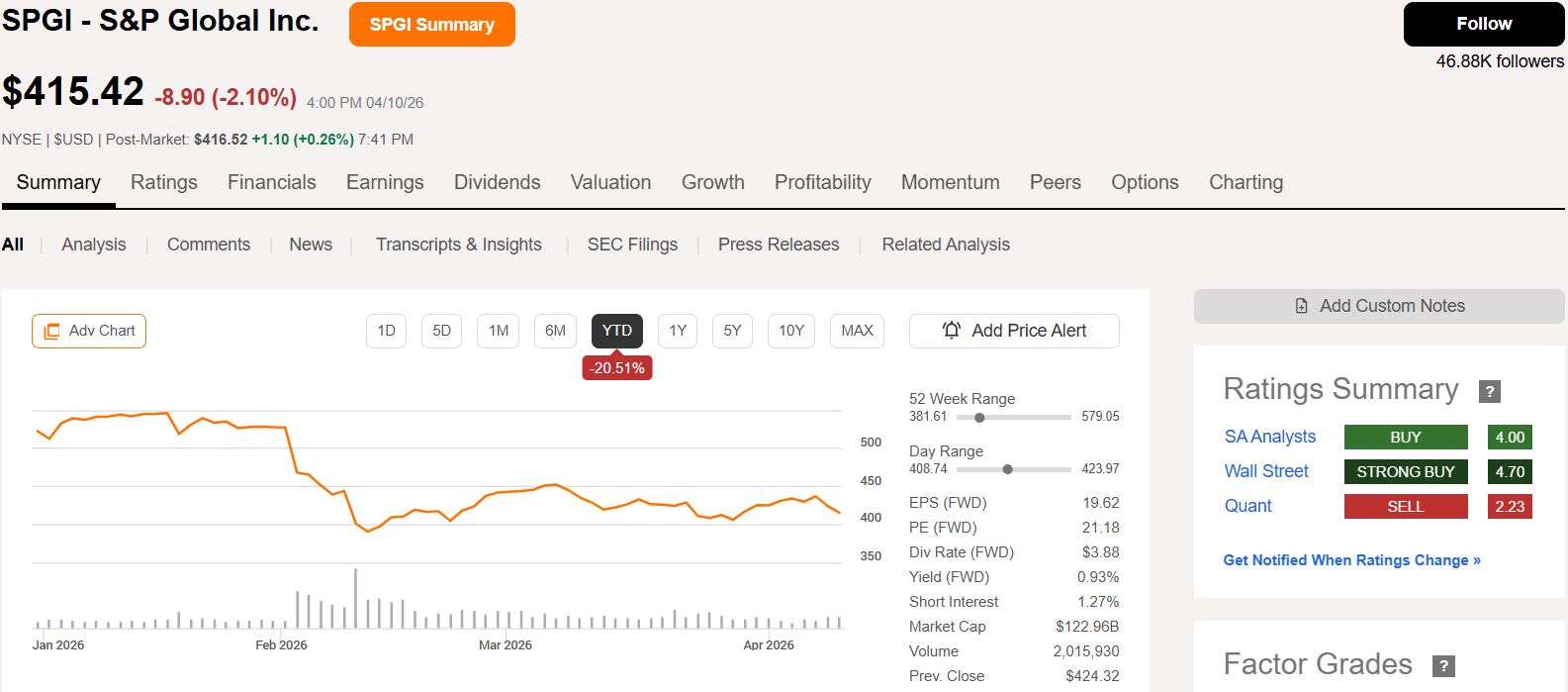

S&P Global is down 20% year to date, with the stock now trading around $415, much closer to its 52-week low of roughly $382 than its high near $579.

At first glance, that kind of drawdown can look unusual for a business of this quality.

But the explanation is fairly straightforward.

The market has become much less willing to pay peak multiples for high-quality compounders, especially those with premium valuations and some sensitivity to macro conditions. In SPGI’s case, the recent backdrop of higher oil prices, renewed geopolitical stress, hotter inflation data, and shifting rate expectations has added another layer of caution across financials and information businesses tied to capital markets activity.

That matters because while S&P Global is an exceptional business, it is not completely immune to macro slowdowns.

Debt issuance can cool. Transaction activity can slow. Sentiment around financial-market-linked businesses can weaken. And when that happens, even elite franchises can go through a valuation reset.

That looks like exactly what has happened here.

Importantly, this does not look like a broken business.

Analysts still expect EPS of $19.62 in 2026 and $22.07 in 2027, implying a healthy growth path from here. Quarterly results have also remained solid overall, with the company beating expectations in three of the last four quarters, and long-term EPS growth expectations still sit around the mid-teens.

So the issue here is not that the business has fallen apart.

The issue is that the stock has been repriced.

Why Now May Be a Great Time to Buy S&P Global

This is where the setup starts to get more interesting.

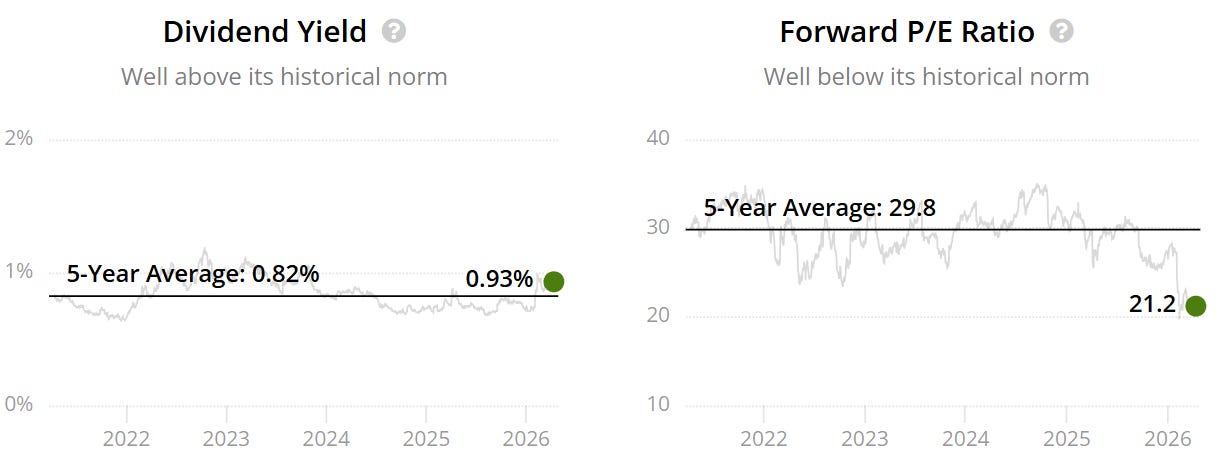

Even after years of premium treatment, SPGI now trades at roughly 21x forward earnings, well below its 5-year average of 30x.

That is a very meaningful reset for a business with this kind of margin profile, competitive positioning, and historical compounding record.

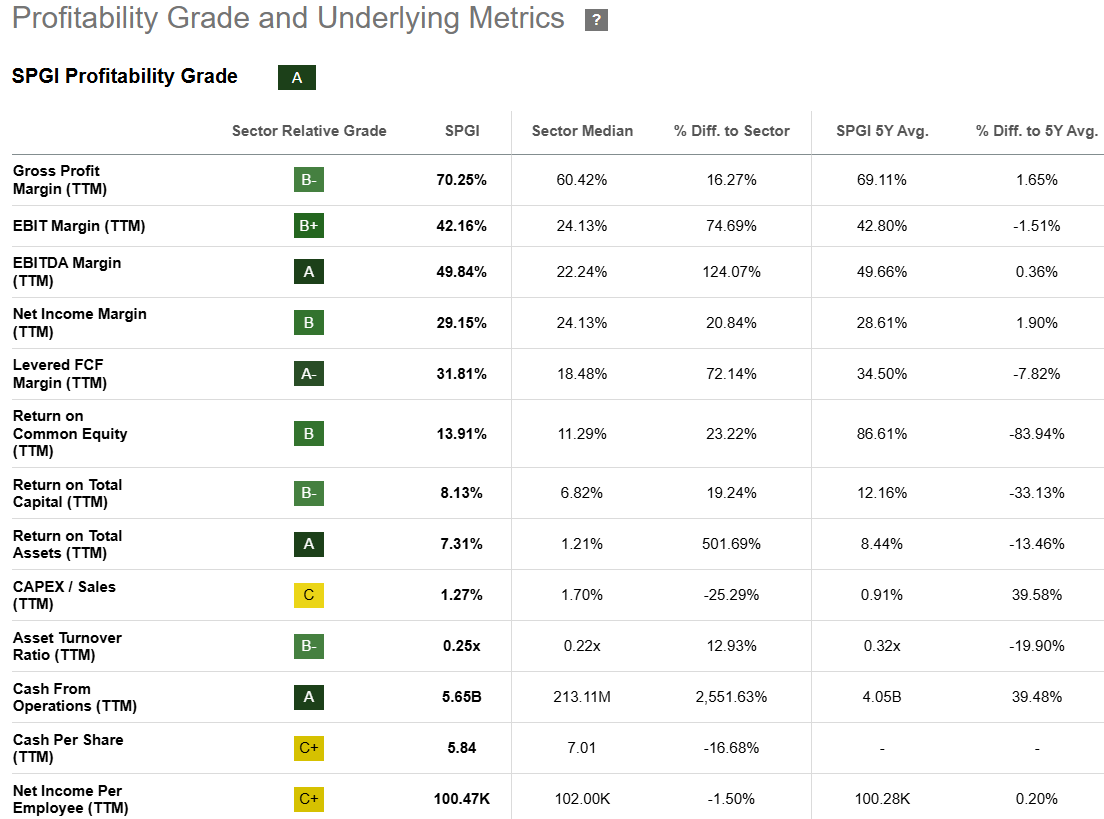

The profitability remains excellent.

Gross margins sit above 70%.

EBIT margins are above 42%.

EBITDA margins are close to 50%.

Levered free cash flow margins remain above 31%.

Those are elite numbers.

This is still a business with strong pricing power, high recurring revenue, and a role in the financial system that is extremely difficult to replicate. The ratings franchise alone benefits from enormous trust, scale, and relevance. Layer on top the index business, analytics, and market intelligence capabilities, and you have a company that still looks far more like a long-term compounder than a business facing structural decline.

That is what makes the current valuation more compelling.

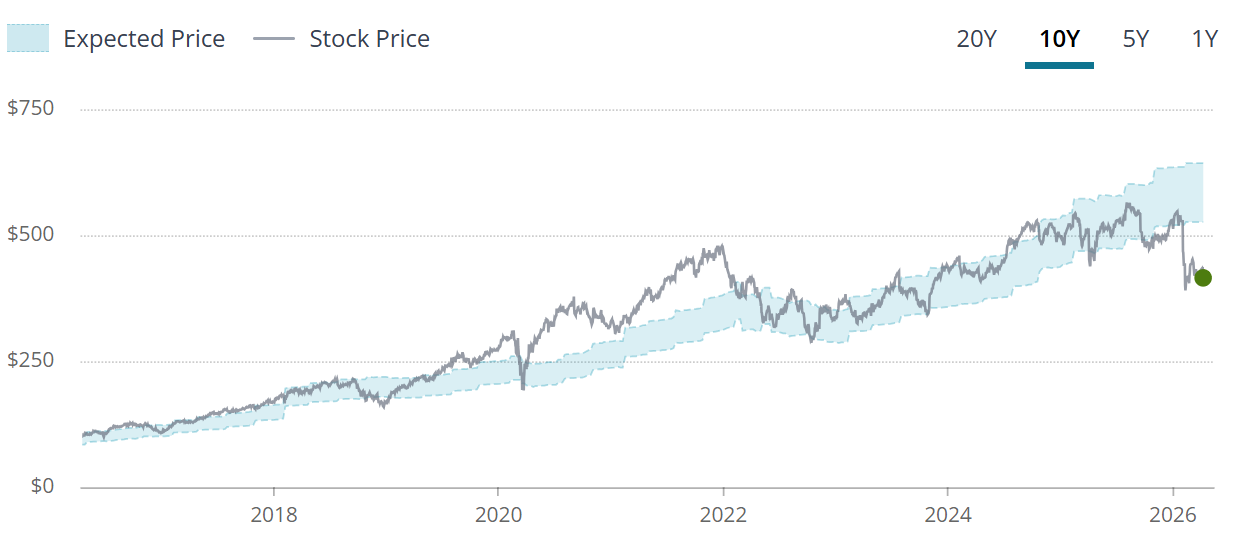

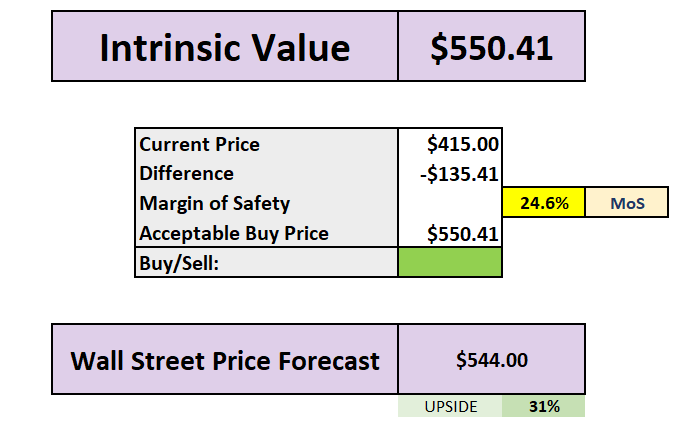

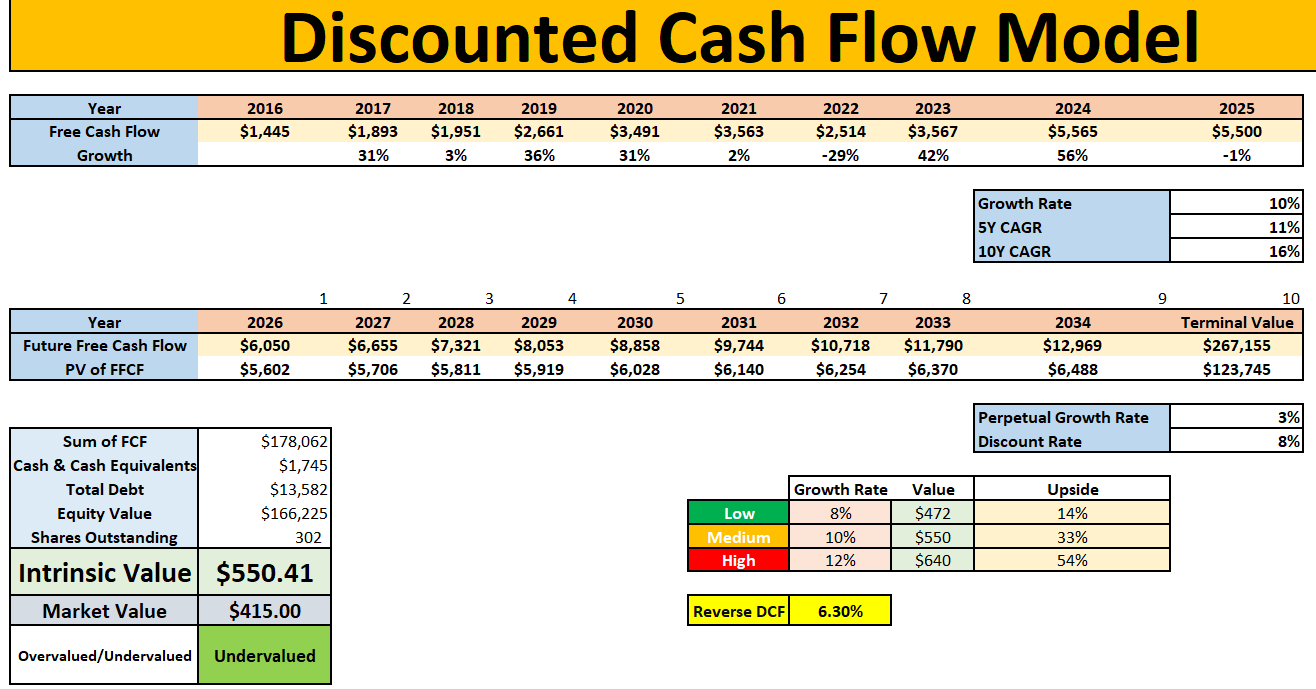

The intrinsic value work points to a fair value of roughly $550, implying about a 25% margin of safety from current levels. Wall Street’s target near $544 also suggests roughly 31% upside.

And perhaps most interestingly, the reverse DCF implies the market is only pricing in around 6.3% growth from here.

For a company with a 5-year free cash flow CAGR of 11% and a 10-year CAGR of 16%, that hurdle does not look especially demanding.

Valuation

The forward P/E now sits around 21x, versus a 5-year average of 30x.

The DCF arrives at an intrinsic value of roughly $550, with the following range:

Low case: $472

Base case: $550

High case: $640

At a current price near $415, that implies:

roughly 25% margin of safety to base value

around 33% upside in the medium case

and a setup that now looks materially more attractive than it did when the market was still willing to pay close to 30x earnings for the same business

The reverse DCF is also telling.

At today’s price, the market appears to be pricing in only about 6.3% long-term growth.

For a company with SPGI’s asset quality, moat, and long-term cash flow profile, that looks more conservative than excessive.

My Take

S&P Global is exactly the kind of stock I want to pay attention to when markets get more fearful.

Not because it is a deep-value name.

And not because it suddenly became statistically cheap against low-quality peers.

But because this is a premium business that the market has become much less willing to pay peak multiples for, even though the long-term thesis still looks very much intact.

The business remains highly profitable, deeply entrenched, and difficult to replicate. Growth is not explosive, but it does not need to be. When a company of this quality goes from nearly 30x forward earnings to just over 21x, while still offering solid earnings growth and robust cash generation, the forward setup starts to look much more compelling.

For investors willing to focus on quality first and valuation second, SPGI looks like one of the more interesting 52-week-low setups in the market right now.

Verdict

BUY

S&P Global is a good example of what happens when the market stops paying peak multiples for quality. The business remains strong, but the valuation has reset enough to make the setup much more interesting.

Across the rest of this list, the same pattern shows up in different ways - from elite compounders with more obvious consumer or software exposure, to under-the-radar names where expectations now look materially lower than the underlying business quality.

Paid members get the remaining 4 picks, full valuation breakdowns, and my final ranking.