500 Stocks Screened — Only 58 Qualified. These 5 Rank Highest (One Still Shows ~50% Upside)

The market has already bounced, but a small group of large-cap S&P 500 names still trade at meaningful discounts to consensus value — ranked by quality, valuation, and downside support.

S&P 500 Performance in April so far

Markets have already bounced.

That usually convinces investors the opportunity is gone.

Often, it is.

Broad selloffs create broad discounts at first. But once the rebound begins, the market stops rewarding everything equally. The easy upside disappears quickly. What remains is narrower, more selective, and often far more interesting.

That is the setup this month.

The S&P 500 has recovered sharply from its recent lows, and sentiment has improved across several parts of the market. But even after that rebound, a small group of large-cap companies still trade at meaningful discounts to consensus value.

This report focuses on those remaining gaps.

Not where prices have already recovered, but where valuation still appears disconnected from business quality, earnings power, and long-term upside.

Large-cap opportunities rarely stay obvious for long.

Once markets stabilize, the broad repricing phase ends. What remains is a narrower group of companies where the valuation reset has not fully reversed despite durable fundamentals, strong cash generation, and analyst expectations that still point materially higher.

Rather than chasing what has already bounced hardest, this report isolates the remaining S&P 500 names where upside still appears asymmetric relative to downside risk.

This Month’s Screening Framework

To identify those opportunities, I screened the S&P 500 for large-cap companies meeting the following criteria:

Market capitalisation above $10B

Minimum 20% projected 12-month upside

Analyst consensus of Moderate Buy or Strong Buy

Durable underlying business quality

Balance sheet and cash flow profile strong enough to support real capital allocation

After applying those filters, 500 companies were screened.

From those, 58 qualified.

That matters.

In a broad selloff, many stocks can look optically cheap. After a rebound, far fewer still do. That makes this month’s list more selective and, in many cases, more actionable.

Some names have already seen their valuation gaps close. Others have not. In several cases, the market appears to have moved on faster than the fundamentals have changed.

Those are the opportunities this report aims to isolate.

April at a Glance

Companies screened: 500

Final qualifying stocks: 58

Minimum projected upside: 20%

Universe: S&P 500, market caps above $10B

Objective: identify large-cap companies where valuation, quality, and forward upside still diverge meaningfully even after the rebound

From the final qualifying group, a smaller subset stands out most clearly based on:

valuation support

business durability

analyst alignment

risk-adjusted upside

downside support from current levels

Five stand out most clearly this month.

They are ranked based on:

Upside potential

Business quality

Valuation compression

Downside support levels

How actionable the setup still looks after the recent rebound

The companies below represent the clearest remaining opportunities currently screening in the S&P 500.

This Month’s Top 5 High-Upside S&P 500 Stocks

Several names have already bounced sharply from the lows.

These five still stand out because the upside has not fully closed.

The lower-ranked names are interesting.

The top-ranked names still look actionable.

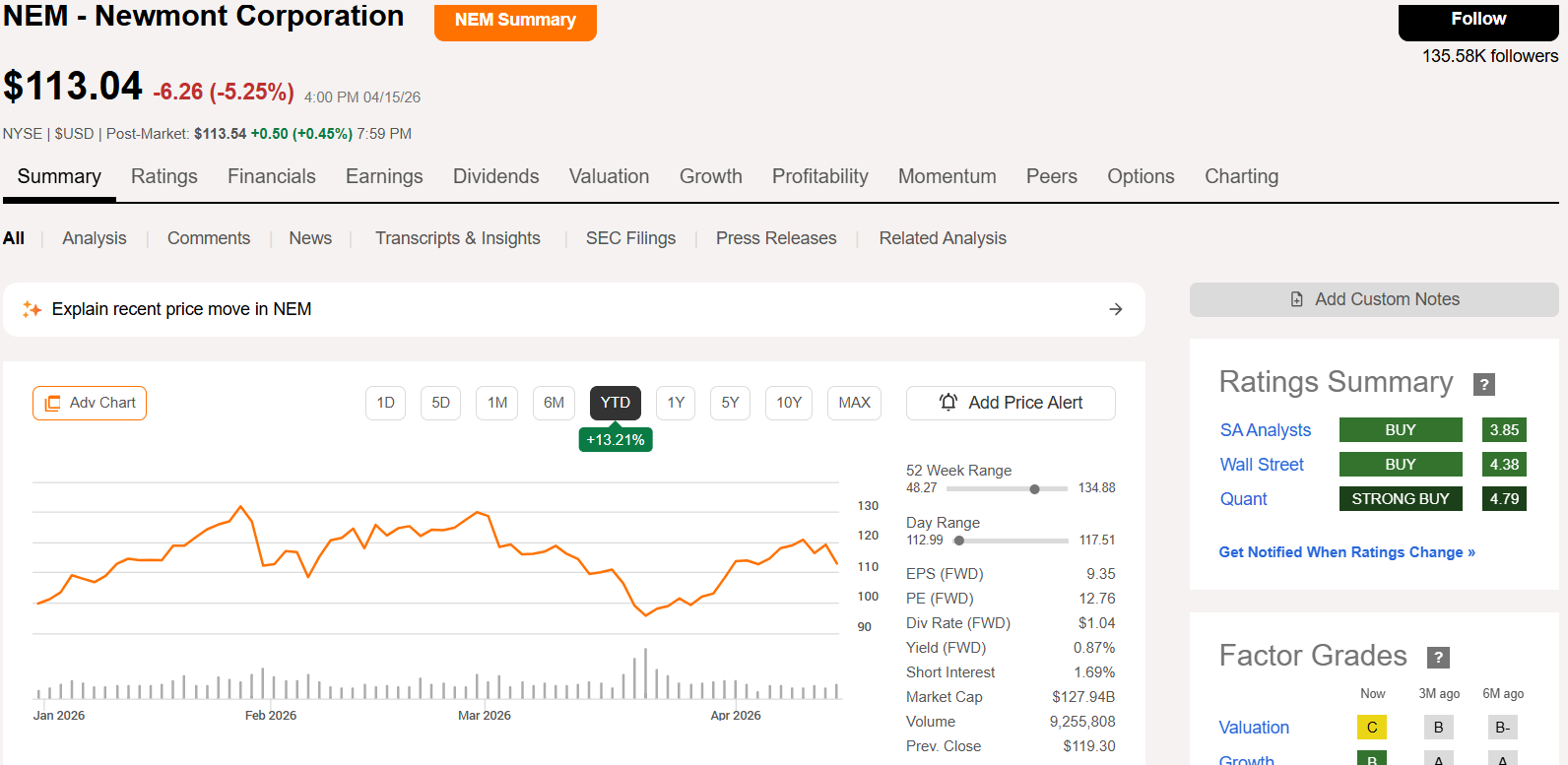

#5 — Newmont Corporation (NEM)

Newmont stands out this month for a different reason than the other names on this list.

The opportunity here is not being driven by a high-growth technology narrative or a temporary sentiment reset around software or financials.

Instead, it comes from a large-cap, cash-generative business where the market still appears to be underestimating the combination of earnings power, margin strength, and valuation support.

That makes Newmont one of the more interesting remaining setups in the screen.

What the Market Is Pricing In

At current levels, investors still appear cautious on the broader gold and mining complex.

That hesitation is understandable.

Mining businesses are cyclical, operationally intensive, and often treated as lower-quality opportunities than asset-light compounders. They also tend to screen cheaply for a reason when commodity expectations are unstable.

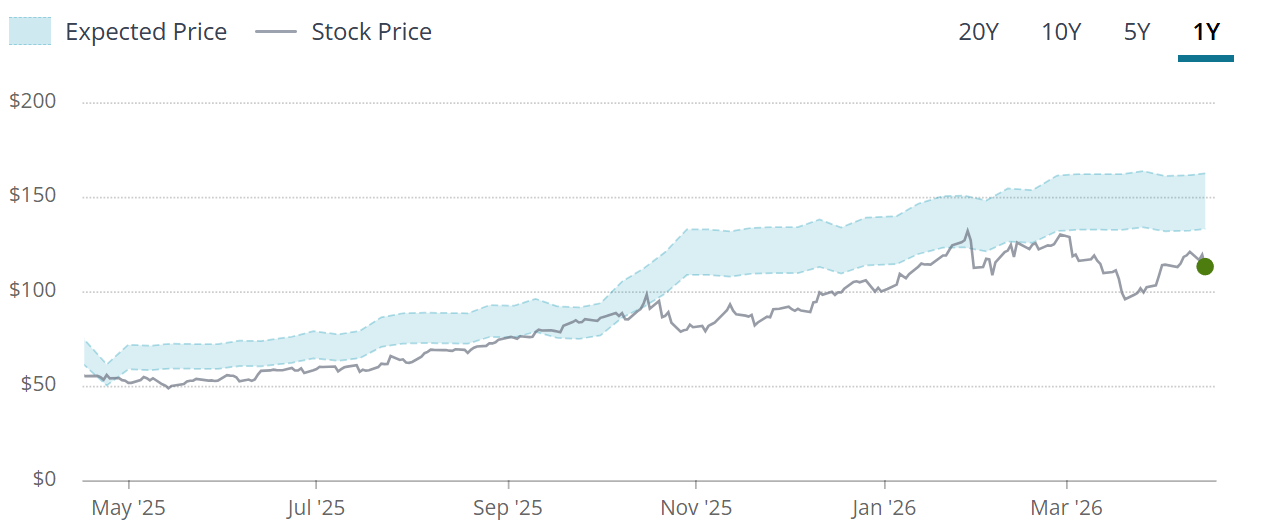

But Newmont’s current setup looks stronger than that broad market perception suggests.

The company remains the clear scale leader in the space, and the underlying financial profile has improved materially.

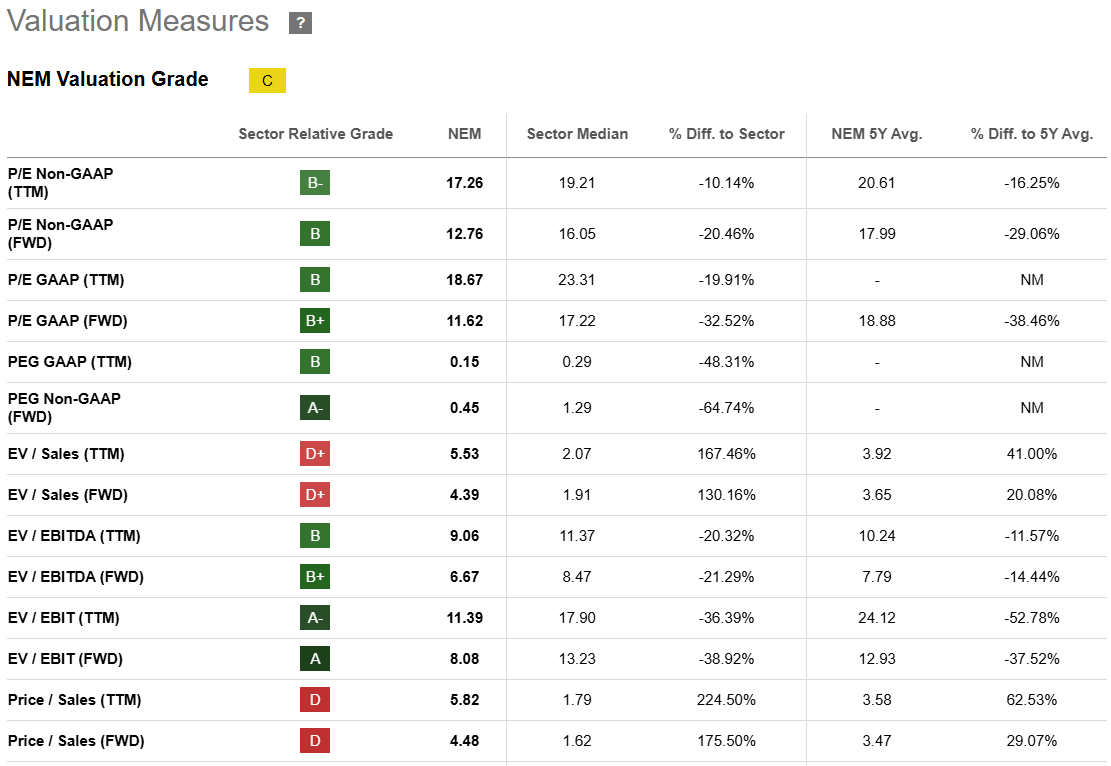

Valuation Context

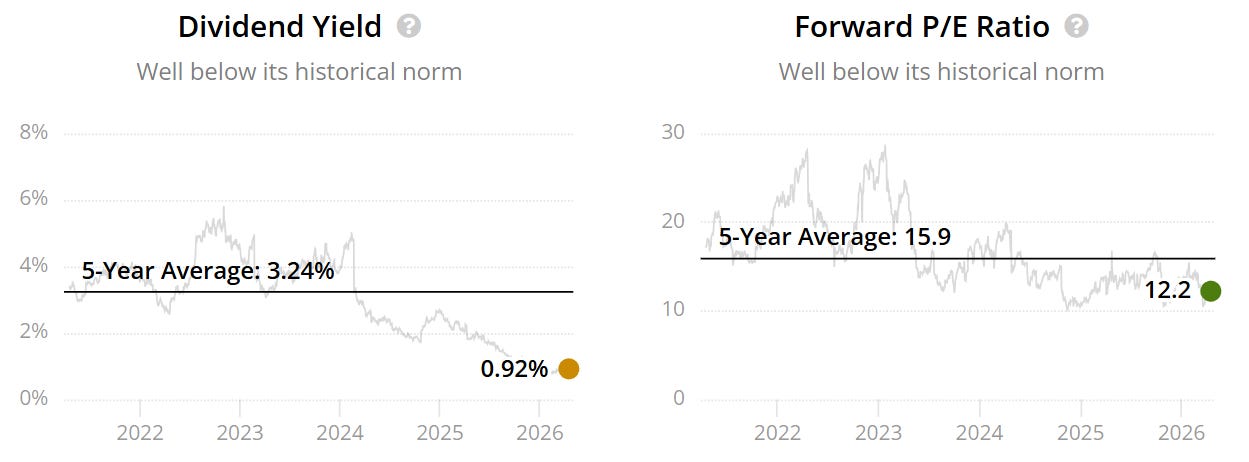

Even after the recent rebound, Newmont still trades at a notable discount to its own historical valuation.

Its forward P/E currently sits around 12.2x, versus a 5-year average closer to 15.9x.

That matters.

Because while the stock has recovered from earlier weakness, the market is still valuing the business below its normal earnings multiple despite a much stronger profitability backdrop than investors typically associate with the sector.

That creates a more attractive setup than the headline dividend yield alone might suggest.

Business Quality

This is where the story gets more interesting.

Newmont’s valuation screen on the surface looks mixed, largely because sales-based multiples remain elevated relative to the sector. But the underlying operating picture is much stronger than that first impression suggests.

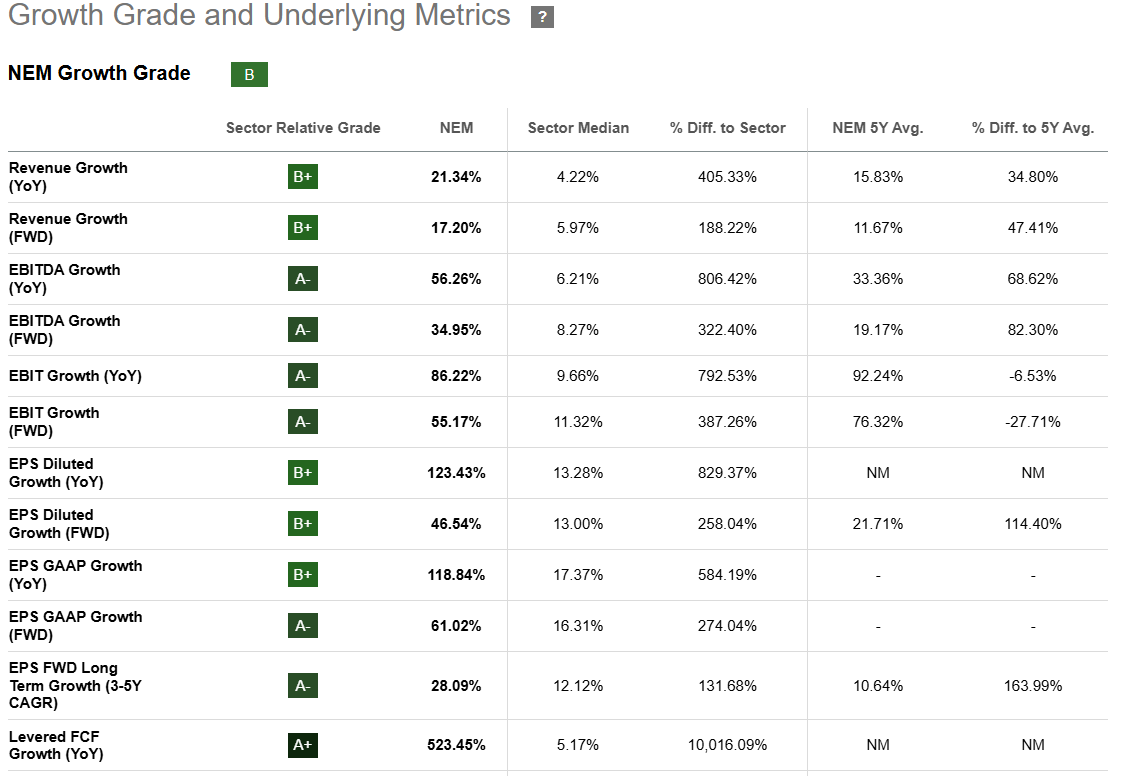

Growth metrics remain robust, including:

21.3% revenue growth

56.3% EBITDA growth

86.2% EBIT growth

123.4% EPS diluted growth

46.5% forward EPS growth

28.1% long-term EPS growth expectation

Those are not weak numbers.

They point to a business benefiting from a much stronger earnings environment than the market may still be fully crediting.

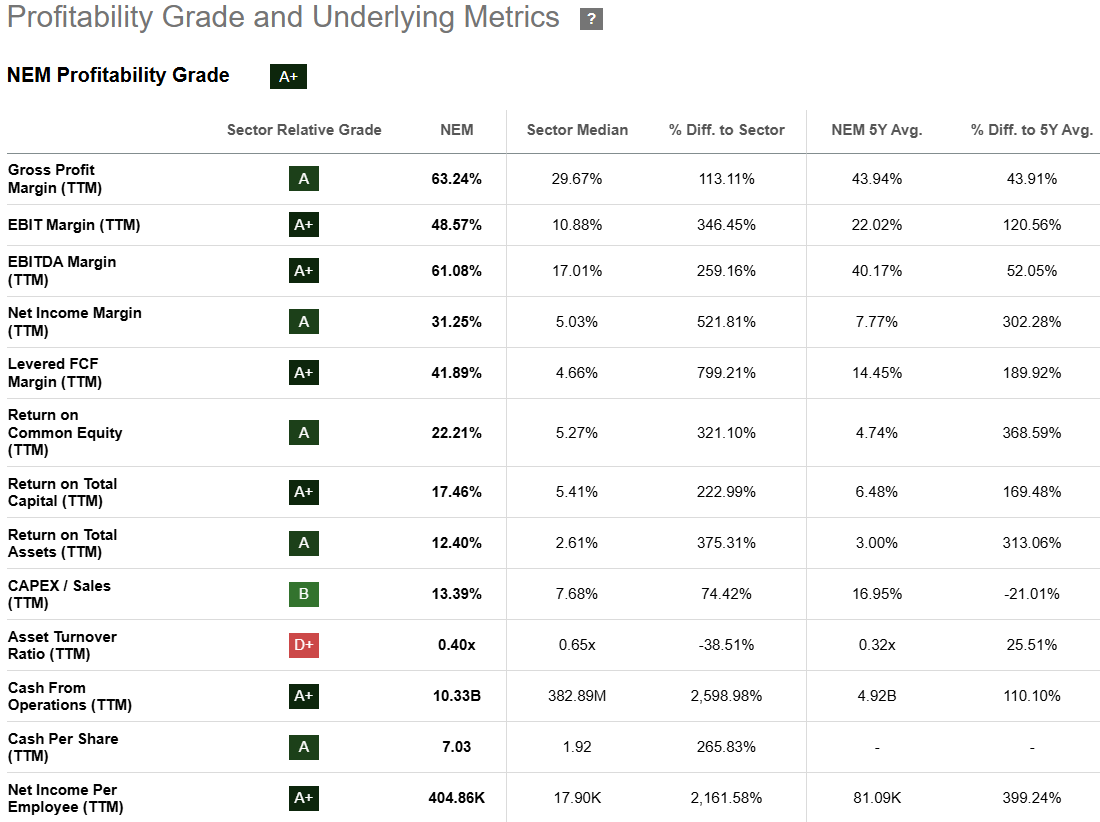

Profitability is also unusually strong for the sector.

Newmont currently carries an A+ profitability grade, supported by:

63.2% gross margin

48.6% EBIT margin

61.1% EBITDA margin

31.3% net income margin

41.9% levered free cash flow margin

17.5% return on total capital

For a mining company, that is a very strong operating profile.

Why It Ranks #5

Newmont ranks #5 this month because it combines three things that rarely show up together cleanly:

large-cap scale

strong profitability

a forward valuation still below its historical norm

The current dividend yield of roughly 0.9% is well below its 5-year average, which may make the stock look less attractive to income-focused investors at first glance.

But that lower yield is really just the mirror image of a stronger share price and improved earnings outlook.

For this screen, the more important point is that the stock still appears reasonably valued relative to its forward earnings power.

Newmont is not the cleanest business model on this list.

It is more cyclical, more commodity-linked, and less predictable than some of the other names ranked above it.

That is why it sits at #5 rather than higher.

But for investors looking for a large-cap name where the valuation still looks supportive and the profitability profile is stronger than the market may appreciate, Newmont remains one of the more compelling remaining opportunities in the screen.

The next four names offer either a larger valuation gap, stronger downside support, or a better overall combination of business quality and upside from current levels.

Two still screen as clear outliers even after the recent rebound.

Paid members unlock:

The remaining Top 4 ranked stocks

Exact buy ranges

Downside scenarios

The full screening dataset

My allocation framework across the list

Which names are actionable now versus watchlist-only