I Can’t Stop Buying These 2 Elite Stocks

Visa and Mastercard are being priced like their moats are breaking. I think the market is making a mistake.

Visa and Mastercard have been two of the best businesses on Earth for decades.

They are not flashy AI stocks.

They do not dominate headlines like Nvidia, Microsoft or Tesla.

And they are rarely the first names people rush to buy during a market rally.

But for long-term investors, they have been almost perfect compounding machines.

Huge margins.

Strong pricing power.

Massive global networks.

Light capital requirements.

High returns on capital.

Consistent buybacks.

And exposure to the long-term shift away from cash.

That is why I have owned these businesses for a long time.

But recently, something has changed.

The market has started to question whether Visa and Mastercard’s best days are behind them.

Europe wants alternatives.

The UK wants alternatives.

Merchants are still angry about swipe fees.

Politicians are once again targeting card economics.

Stablecoins are being called a serious threat.

And reports suggest companies like Amazon and Walmart may be exploring their own payment coins.

So the obvious question is this:

Are Visa and Mastercard finally losing their moat?

Or is this simply another moment where investors panic, the stocks sell off, and two elite businesses keep quietly printing cash?

My view is simple.

The risks are real.

But I do not think the business models are broken.

In fact, I think this could be one of those rare moments where the market gives long-term investors a better price on two of the highest-quality companies in the world.

The Market Is Suddenly Worried

What makes this setup so interesting is that the broader market has been strong.

AI stocks have been running.

The S&P 500 has continued pushing near record highs.

Several mega-cap names still trade close to their peaks.

But Visa and Mastercard have moved in the opposite direction.

Visa is down around 12% from its 52-week high.

Mastercard is down around 18% from its 52-week high.

That is not a collapse. But for businesses of this quality, that kind of move matters.

These are not random struggling companies.

These are elite global payment networks that have historically traded at premium valuations because the market understands how powerful their economics are.

So when the market starts discounting them, I pay attention.

The big concern is that Visa and Mastercard are now being attacked from almost every angle at the same time.

Regulators are questioning card fees.

Merchants want more control.

Governments want domestic payment alternatives.

Stablecoins are being promoted as faster and cheaper rails.

And large retailers may want to reduce their dependence on traditional card networks.

That sounds scary.

But scary headlines and broken fundamentals are not the same thing.

The Bear Case Is Not Stupid

Before making the bullish case, it is worth being honest about the risks.

The bear case against Visa and Mastercard has become more credible than it was a few years ago.

This is no longer just the usual argument of:

“The stocks are expensive.”

That argument has existed for years.

The new argument is more serious.

It says Visa and Mastercard could face structural pressure from four directions:

Regulation

Merchant pushback

Stablecoins

Alternative payment rails

The political risk is especially important.

For years, Visa and Mastercard benefited from being the default global payment networks. But governments are now asking whether countries should rely so heavily on American card networks.

That matters because payments are no longer just about convenience.

They are about control.

They are about sovereignty.

They are about who owns the rails of money movement.

If Europe, the UK or other regions decide they want more domestic alternatives, Visa and Mastercard may face more pressure over time.

Then there is the swipe-fee issue.

Merchants have long complained about the cost of accepting card payments. Every time a consumer taps, swipes or inserts a card, merchants pay fees into the card ecosystem.

Those fees help fund the system.

They support rewards.

They incentivise banks.

They support fraud protection, processing, authorisation and network access.

But from the merchant perspective, they are a cost.

The recent legal settlement around swipe fees could allow merchants to be more selective over which cards they accept. That matters because premium rewards cards tend to carry higher costs.

If merchants can push back against higher-interchange cards, the economics of certain reward-heavy card products could come under pressure.

This does not destroy Visa or Mastercard overnight.

But it is a genuine risk.

And then comes the biggest fear of all.

Stablecoins.

Are Stablecoins the Beginning of the End?

Stablecoins have become the new scary word for Visa and Mastercard investors.

The bearish argument is simple:

If consumers and businesses can move digital dollars instantly, 24/7, across blockchain rails, why would they keep paying traditional card network fees?

And if companies like Amazon or Walmart launch their own payment coins, could they pull transaction volume away from Visa and Mastercard?

On the surface, that sounds dangerous.

But I think investors need to separate two very different use cases.

Stablecoins may be extremely useful for:

cross-border payments

remittances

B2B settlement

treasury movement

crypto-native ecosystems

instant dollar transfer outside traditional banking hours

But that is not the same as replacing mainstream consumer card payments at scale.

Consumer payments are incredibly difficult.

It is not enough to create a faster rail.

You need trust.

You need fraud protection.

You need dispute resolution.

You need identity.

You need compliance.

You need bank partnerships.

You need merchant acceptance.

You need consumer habit.

You need global reliability.

And this is where Visa and Mastercard are still incredibly powerful.

The biggest advantage of Visa and Mastercard is not just that they process transactions.

It is that they are accepted almost everywhere.

Visa has access to roughly 150 million merchant locations. That kind of acceptance network is extremely difficult to replicate.

Stablecoins may be faster money.

But faster money still needs somewhere to go.

And this is where the bull case gets interesting.

Stablecoins may not kill Visa and Mastercard.

They may end up using them.

Visa and Mastercard Are Not Ignoring Stablecoins

This is the part of the story I think the market may be missing.

Visa and Mastercard are not sitting still and pretending stablecoins do not exist.

They are already trying to connect themselves to the new rails.

Mastercard has been expanding into blockchain and stablecoin infrastructure, including the reported BVNK acquisition, which is designed to connect on-chain payments with traditional fiat rails.

Visa has also been building stablecoin settlement capabilities for years and has already talked about real volume moving across blockchain-based settlement infrastructure.

That changes the story.

The simple bearish view is:

Stablecoins replace Visa and Mastercard.

But the more nuanced view is:

Stablecoins still need distribution, acceptance, compliance, security and merchant connectivity — and Visa and Mastercard can provide that infrastructure.

That does not mean there is no risk.

There is risk.

But I do not think this is a clean “old rails die, new rails win” situation.

Payments rarely work that way.

The more likely outcome is that new payment technologies get absorbed into the existing financial ecosystem.

That has happened before.

Investors once worried that PayPal would disrupt Visa and Mastercard.

Then they worried about Apple Pay.

Then they worried about buy now, pay later.

Now they are worried about stablecoins.

But historically, Visa and Mastercard have not been easy to replace.

They have adapted.

And so far, the numbers still suggest these businesses are growing, not breaking.

The Fundamentals Are Still Excellent

This is where the current market narrative starts to look disconnected from reality.

If Visa and Mastercard were truly being disrupted today, I would expect to see weakness in the numbers.

But that is not what we are seeing.

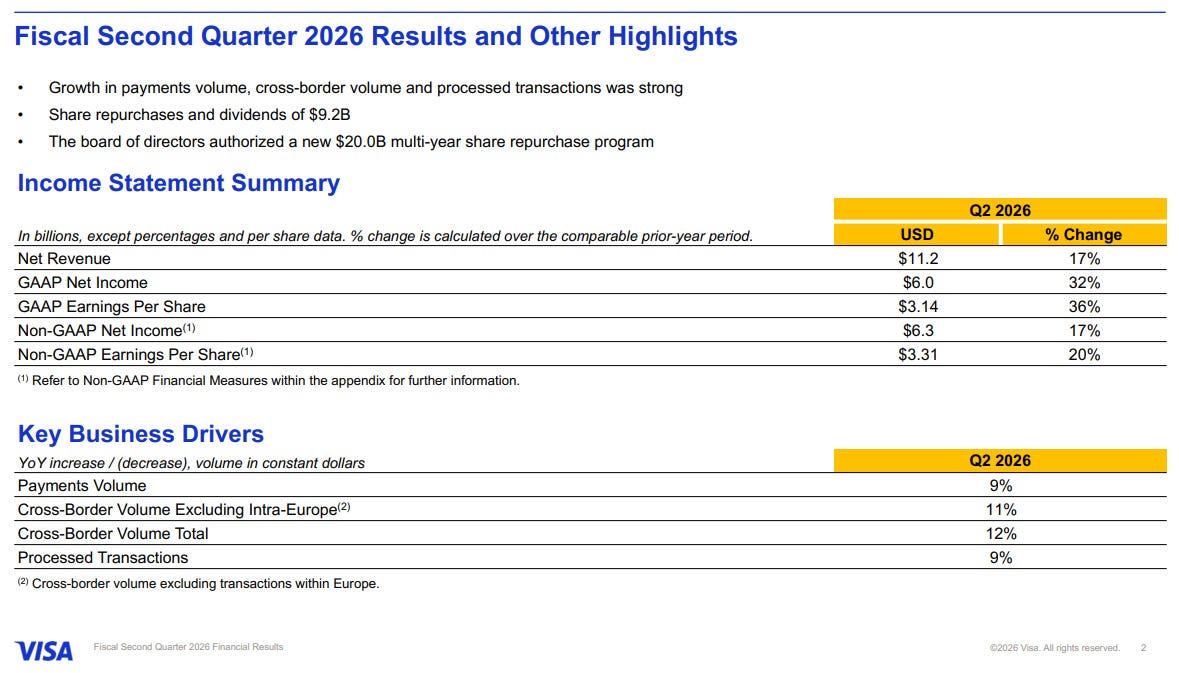

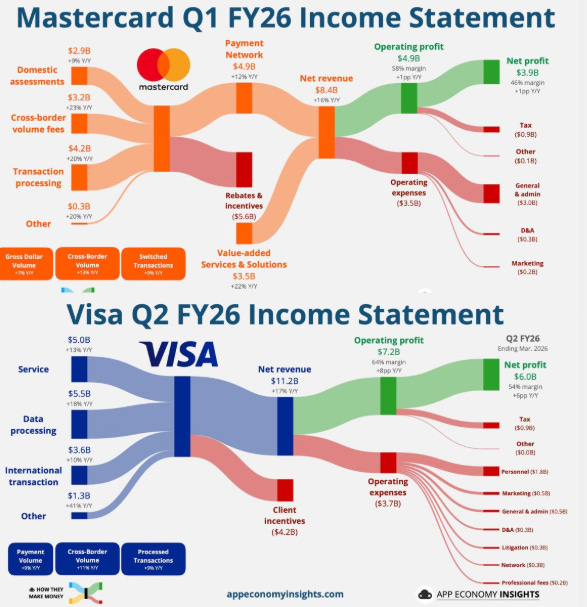

Visa’s latest quarter was strong.

Revenue came in at around $11.2 billion, up 17% year over year.

Non-GAAP EPS came in at $3.31, up 20% year over year.

Payments volume grew 9%.

Cross-border volume, excluding intra-Europe, grew 11%.

Processed transactions grew 9%.

That is not what a broken payment network looks like.

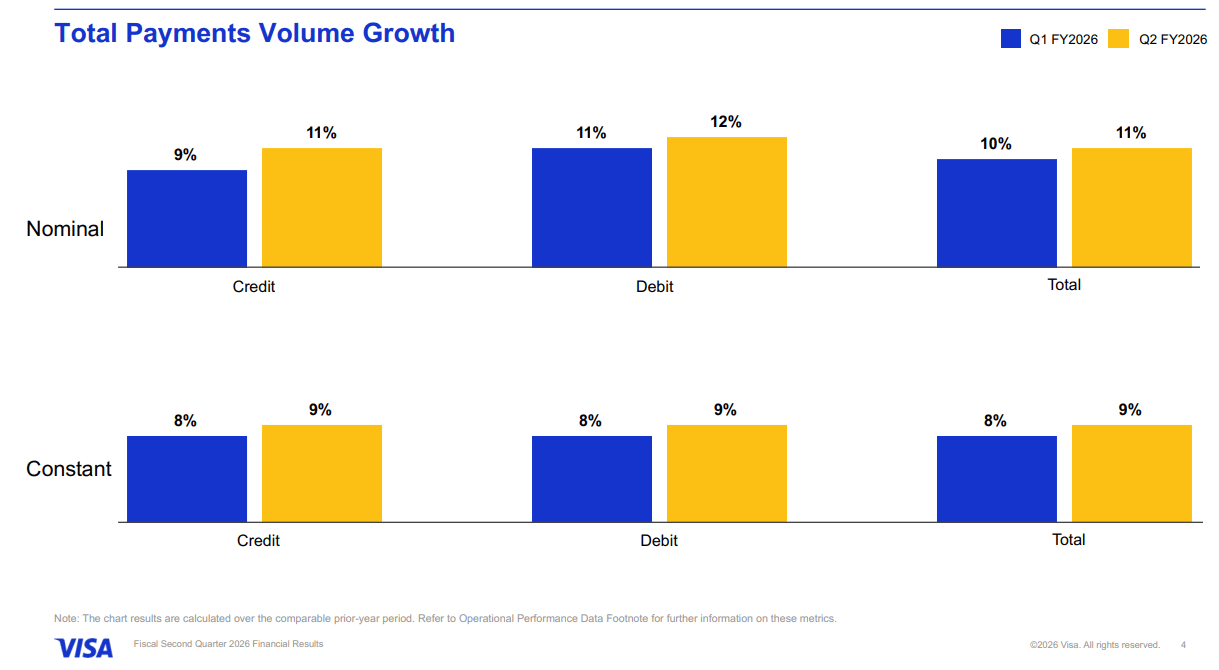

Even more importantly, Visa’s payment volume growth actually accelerated from Q1 to Q2.

US credit improved.

US debit improved.

International payment volume remained strong.

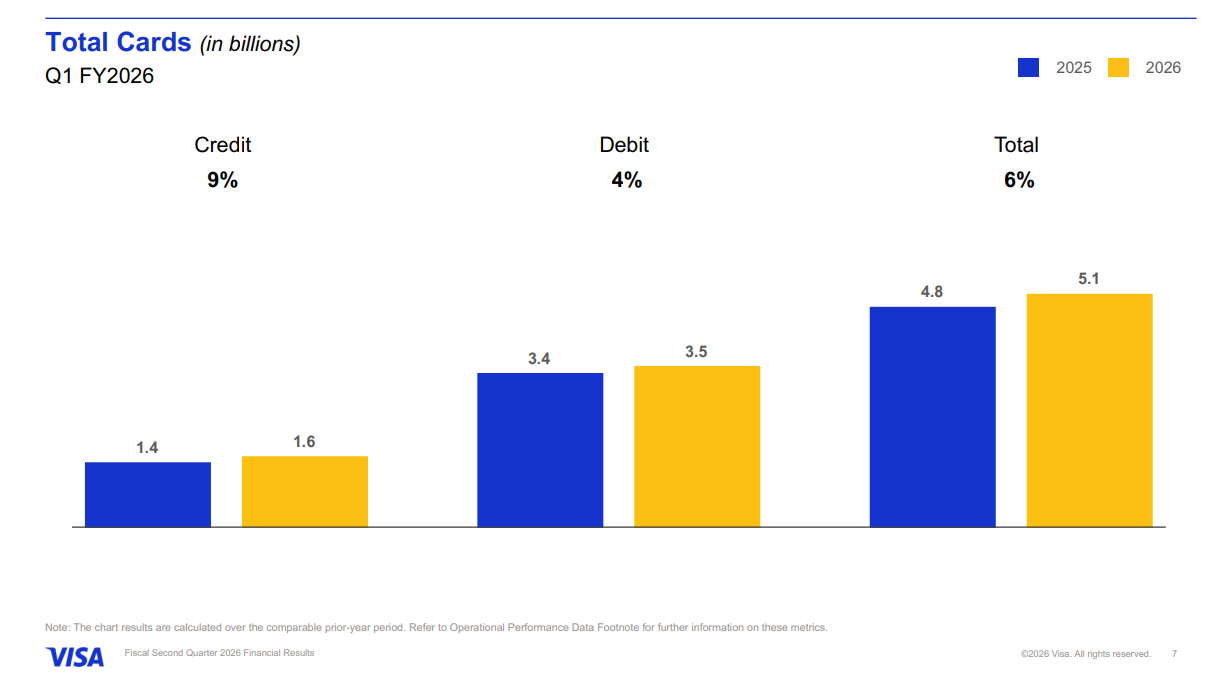

And Visa now has around 5.1 billion cards, up approximately 6% year over year.

So despite all the disruption fears, the network is still expanding.

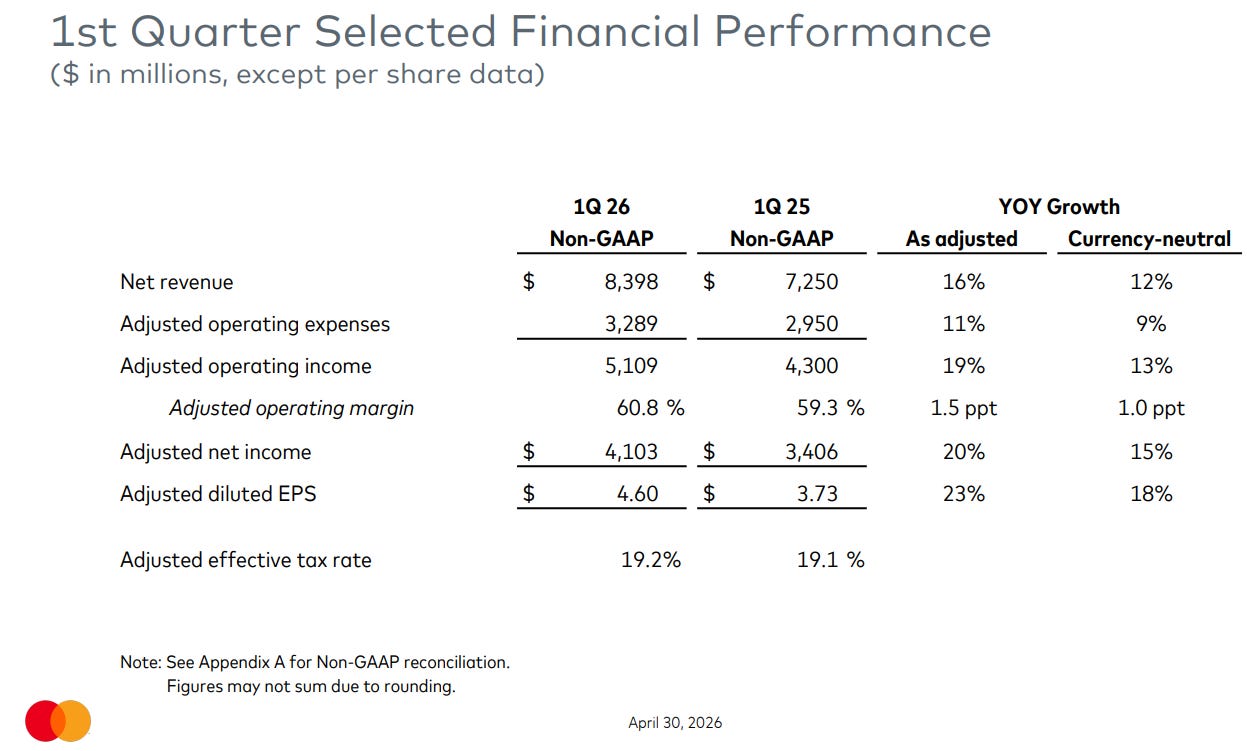

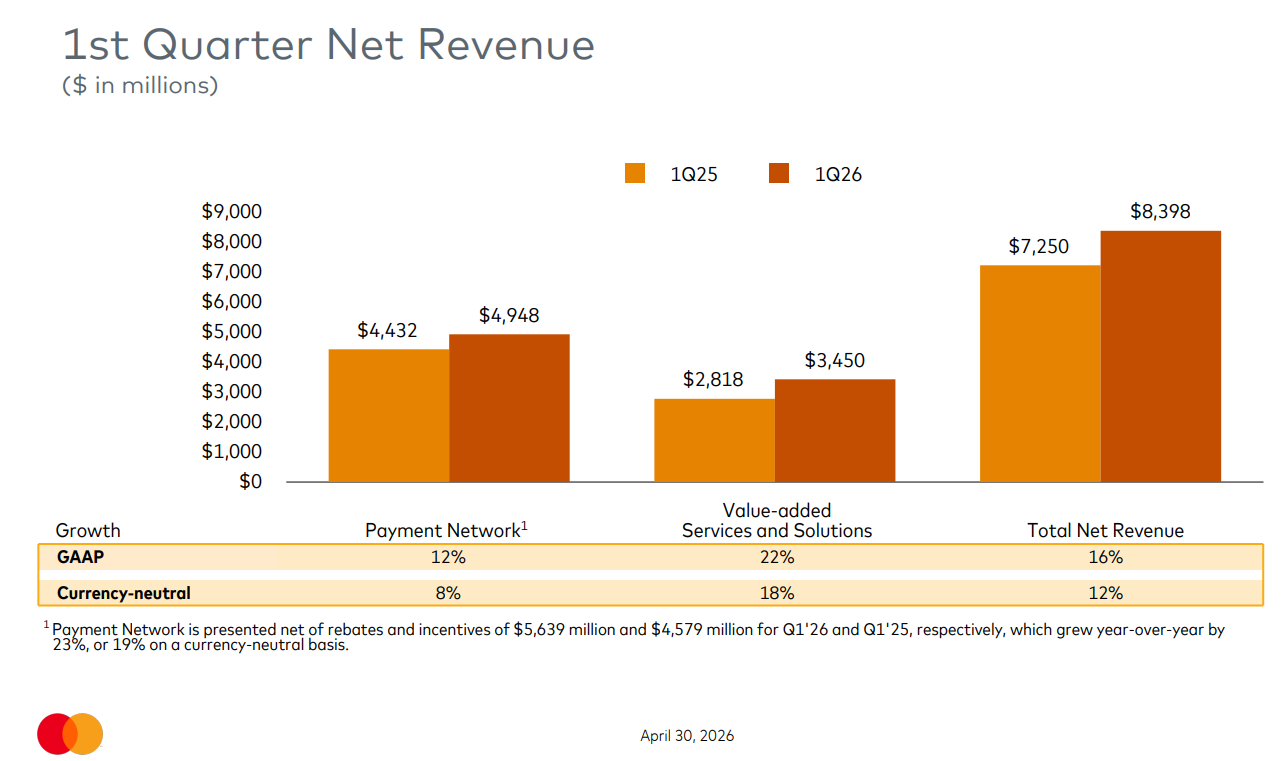

Mastercard was also strong.

Net revenue grew 16%.

Adjusted operating income grew 19%.

Adjusted diluted EPS grew 23%.

Adjusted operating margin was above 60%.

Again, these are not normal numbers.

Most companies would dream of this financial profile.

But the most interesting part of Mastercard’s results was its Value-Added Services and Solutions segment, which grew 22%.

That matters because Mastercard is no longer just a card network.

It is building a wider ecosystem around:

fraud prevention

data analytics

cyber security

identity

open banking

consulting

and now stablecoin infrastructure

That makes the business model more diversified than many investors realise.

These Are Still Global Toll Roads

The reason I have always liked Visa and Mastercard is because they behave like toll roads on global commerce.

They do not lend money to consumers.

They do not take the same credit risk as banks.

They do not need to own huge physical infrastructure.

They simply sit in the middle of a global transaction network and take a small fee as money moves.

That is a beautiful business model.

Mastercard converts around $8.4 billion of revenue into roughly $4.9 billion of operating profit.

Visa converts around $11.2 billion of revenue into roughly $7.2 billion of operating profit.

These are extremely high-margin businesses.

Visa operates around the high-60% operating margin level.

Mastercard operates around the high-50s to 60% range.

That is why the stocks rarely look cheap.

Investors are not just paying for growth.

They are paying for growth with exceptional profitability.

And the long-term transaction data still looks healthy.

From 2012 to 2025, Mastercard’s annual transaction volume increased by around 191%.

Visa’s increased by around 165%.

The bear case requires a meaningful slowdown in the core payment network.

So far, the long-term trend is still up and to the right.

The Real Question

The entire debate comes down to one question:

Can the world build alternative payment rails fast enough to weaken Visa and Mastercard?

Or will Visa and Mastercard simply connect themselves to the new rails and continue taking a fee?

That second outcome is the one I think the market may be underestimating.

Because Visa and Mastercard have a long history of adapting to threats.

They did not get destroyed by PayPal.

They did not get destroyed by Apple Pay.

They did not get destroyed by fintech wallets.

They did not get destroyed by buy now, pay later.

In many cases, these “disruptors” actually increased digital payment volume and strengthened the overall ecosystem.

That is the key point.

New payment methods do not automatically hurt Visa and Mastercard.

Sometimes they expand the market.

The world is still moving away from cash.

More commerce is becoming digital.

More transactions are happening online.

More money is moving across borders.

More businesses need fraud prevention, security, identity and compliance.

That is still a very attractive backdrop.

Institutional Investors Are Not Running Away

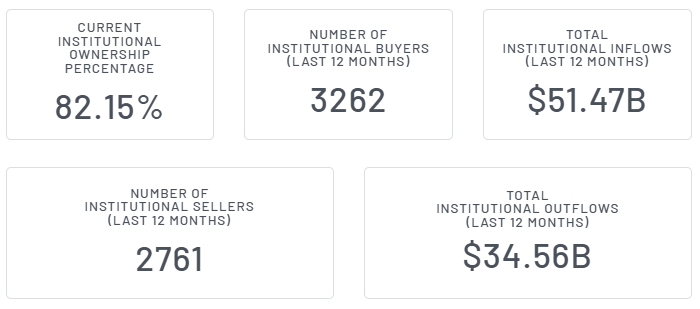

Another interesting part of the current setup is institutional ownership.

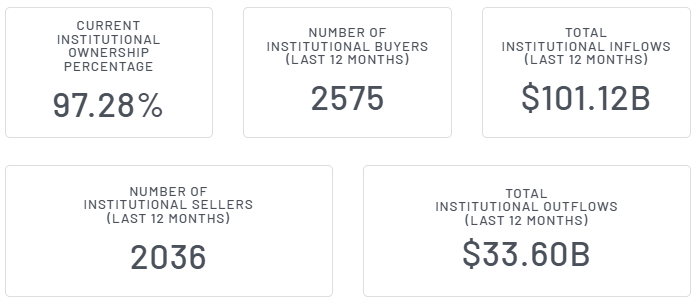

Visa has more than 82% institutional ownership.

Mastercard has around 97% institutional ownership.

That does not mean the stocks cannot fall.

It does not mean institutions are always right.

And it does not mean investors should blindly copy them.

But it does suggest these are not abandoned, dying businesses.

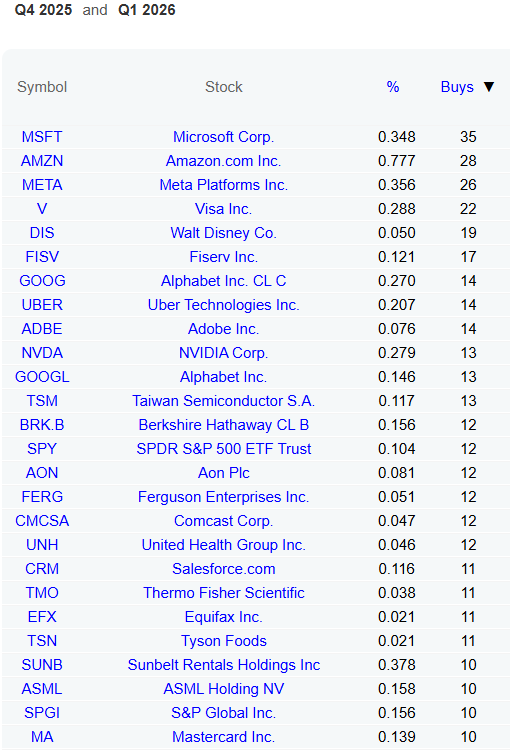

The super-investor data is also interesting.

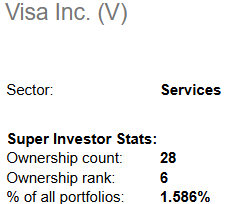

Around 28 super investors hold Visa.

Around 21 super investors hold Mastercard.

Over the last two quarters, 22 super investors added to Visa, while 10 added to Mastercard.

Again, this does not prove Visa is better.

But it does show that sophisticated investors are still interested in these names despite the headlines.

It is also worth noting that Berkshire Hathaway has reportedly sold out of both Visa and Mastercard.

That is worth paying attention to.

But I would not overreact to it either.

Berkshire has been trimming and reshaping parts of its portfolio for a while. A sale by Berkshire does not automatically mean the long-term thesis is broken.

What matters more to me is whether the businesses themselves are weakening.

And right now, I do not see that in the numbers.

The Valuation Is Finally Interesting

Visa and Mastercard are rarely “cheap” in the traditional sense.

These are premium businesses.

Premium businesses usually trade at premium valuations.

So the goal is not necessarily to buy them at deep value multiples.

The goal is to buy them when the market is temporarily worried enough to offer a reasonable entry point.

And today, I think we are closer to that kind of setup.

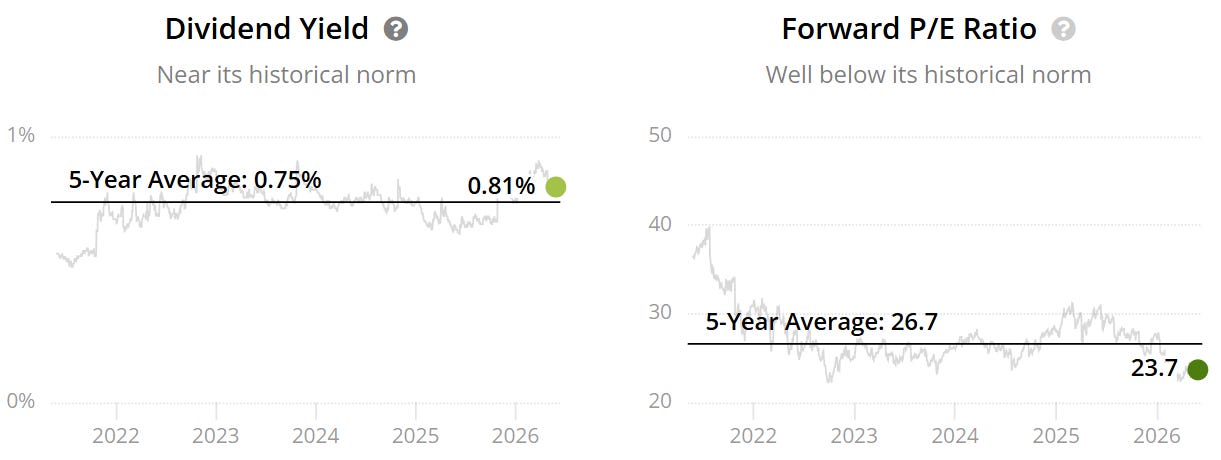

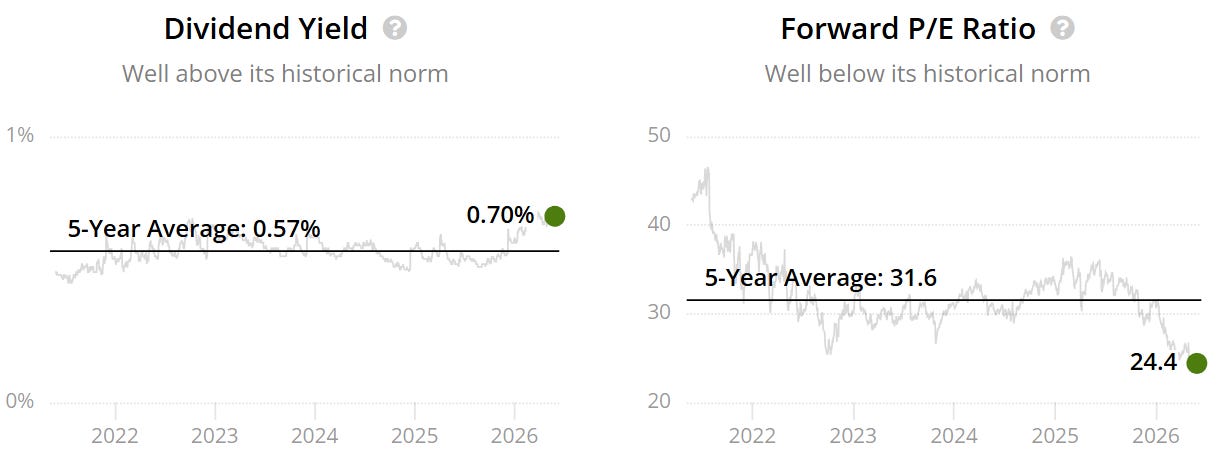

Visa trades at a forward P/E of around 24x, compared to its 5-year average of roughly 27x.

So Visa is not screaming cheap.

But for Visa, this is clearly cheaper than normal.

Mastercard looks even more interesting from a relative valuation perspective.

It trades at a forward P/E of around 24x, compared to its 5-year average of roughly 32x.

That means Mastercard is trading at a much bigger discount to its own history.

This is where the comparison gets interesting.

Visa looks safer.

Mastercard looks more discounted.

Visa has the cleaner balance sheet.

Mastercard has the stronger growth profile.

Visa has slightly better defensive characteristics.

Mastercard may have more upside if sentiment recovers.

That is why I like both.

But if I had to pick one today, the answer becomes more nuanced.

Paid Subscribers: My Fair Value Estimates, Buy Prices and Final Ranking

The rest of this article includes my updated valuation work, including:

my fair value estimate for Visa

my fair value estimate for Mastercard

the implied margin of safety for both stocks

the reverse DCF expectations

which one I would buy first today

and how I would rank them inside a long-term portfolio

Paid members also get access to the full research archive, including last month’s May Best Stocks to Buy edition. The full June edition goes live on Monday morning.

👉 Read last month’s May Best Stocks to Buy edition here:

That spreadsheet will screen the market for the best mix of quality, valuation, risk and income and highlight the stocks that currently look most attractive based on my models.

This Visa and Mastercard setup is exactly the type of situation I like to look for:

elite businesses, scary headlines, strong fundamentals, and a market that may be overreacting.