I Ran a DCF on the Magnificent 7 — Are Any Actually Undervalued?

Stripping away the AI hype to see which mega-caps still justify their price.

Most investors don’t lose money by picking bad companies - they lose it by overpaying for great ones.

I built a valuation system to answer one question every week:

👉 What’s actually worth buying *now* - and what only looks attractive?

Paid members get the same tools I use to size risk, find upside, and avoid value traps.

Each month, members receive:

📊 Undervalued Dividend Dashboard - A live spreadsheet ranking income stocks by valuation, yield safety, and margin of safety (released on the 1st).

🚀 High-Upside S&P 500 Valuations - Market leaders scored by upside, downside risk, and exact buy zones (released on the 15th).

🧠 Weekly Buy / Hold / Avoid analysis - Clear decisions - not just commentary - tied directly to articles like this one.

Free readers get the story.

Paid readers get the numbers, the risk, and the decision.

Over 140,000 investors follow my work across YouTube and Substack, using these models to manage real portfolios - not paper ideas.

Valuation never exists in a vacuum.

The answers a DCF gives you depend just as much on the broader market environment as they do on company-specific assumptions - growth rates, margins, discount rates, and risk appetite all move together.

That’s why before digging into the model outputs on the Magnificent 7, it’s worth stepping back and looking at what actually changed in markets last week.

Because the recent pullback in tech wasn’t random - it reflected shifting narratives around AI, capital spending, interest rates, and investor risk tolerance. And those shifts directly impact how much future cash flow the market is willing to pay for today.

With that context in mind, here’s the market setup going into the DCF analysis.

Market Update

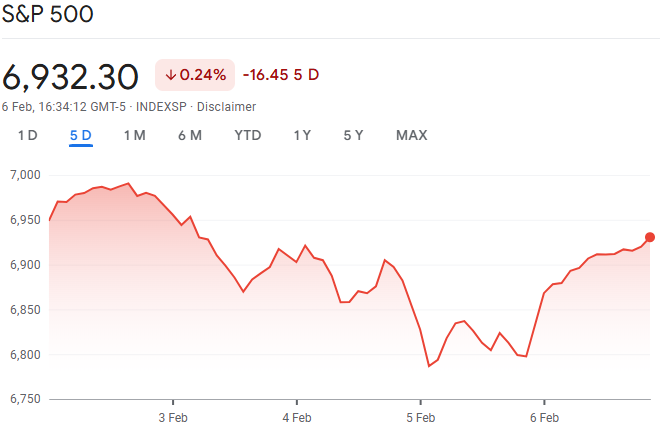

It was a tale of two markets this week.

Big Tech - after months of carrying the market higher - finally stumbled. The Nasdaq had its worst week since November as investors started asking harder questions about AI: How much is too much spending? Are expectations simply too high? That doubt was enough to shake some of the market’s most crowded trades.

But while mega-cap growth stocks struggled, the rest of the market quietly strengthened.

Small caps, mid caps, value stocks - even the Dow - pushed higher. Money didn’t leave equities; it rotated. Investors moved out of expensive, AI-heavy names and into areas tied to the real economy - industrials, cyclicals, and other “old economy” sectors that had lagged for years.

The economic backdrop added to the tension. Labor data came in softer than expected. Private payroll growth slowed. Job openings fell to their lowest level since 2020. Layoff announcements spiked to levels not seen for a January since the financial crisis. The job market isn’t breaking - but it’s clearly cooling.

At the same time, manufacturing showed fresh signs of life. Activity expanded for the first time in a year, and new orders rebounded sharply. Services activity held steady in expansion territory. In short: parts of the economy are slowing, while others are quietly reaccelerating.

Bond markets leaned toward caution, with yields drifting lower as investors processed the softer labor data.

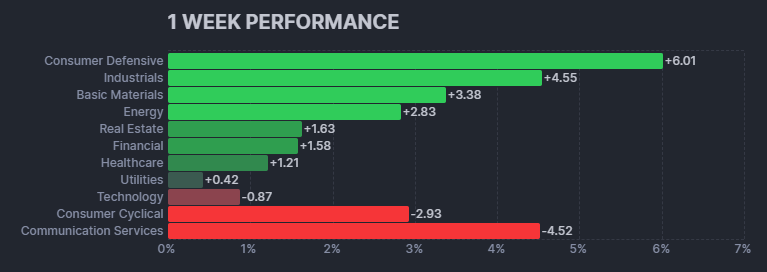

The bigger story isn’t a collapsing market - it’s a changing leadership cycle.

AI disruption fears and surging tech spending have sparked volatility, but the weakness has been concentrated in the mega-cap growth names that dominated returns for years. Meanwhile, improving industrial activity and broader economic resilience are supporting a rotation into under-owned sectors.

For portfolios, this shift matters. Rotation reduces concentration risk, opens the door to diversification, and helps normalize valuations after an extended period of tech-driven dominance.

The market isn’t falling apart. It’s rebalancing.

Last Weeks Winners & Losers

Top performers:

Hershey (+19%)

Bristol-Myers (+13%)

Amgen (+12%)

Merck & Co (+11%)

UPS (+10%)

Walmart (+10%)

Biggest drops:

PayPal (-23%)

Boston Scientific (-18%)

S&P Global (-17%)

ServiceNow (-14%)

Oracle (-13%)

Amazon (-12%)

Notable News

Broadening the Cycle

The spotlight is shifting.

After years of tech dominating nearly every headline and portfolio, capital is moving back toward the so-called “old economy.” Energy. Industrials. Transportation. Consumer staples. Regional banks. The kinds of businesses tied to real assets and real activity - not just digital scale.

These sectors had been left behind during the AI-fueled surge in mega-cap growth. Now, they’re quietly outperforming.

Why the change?

First, valuations matter again. Many of these companies trade at far more reasonable levels than the crowded tech leaders. Second, earnings growth is accelerating outside of technology. And third, investors are looking to reduce concentration risk after years of heavy exposure to a handful of mega-cap names.

The macro backdrop is helping. Higher-income consumers continue to spend. Fiscal support from last year’s tax bill is beginning to flow through the system, boosting refunds and encouraging business investment. And AI-related capital spending - ironically - also benefits industrial suppliers, utilities, and infrastructure plays beyond just the tech platforms themselves.

Put together, the economy looks more balanced than it has in years. Growth doesn’t have to come from just one corner of the market.

Economists are taking note. Expectations for U.S. GDP have been revised higher, with growth now projected around 2.5% in 2026.

This isn’t the end of tech. It’s the broadening of the cycle.

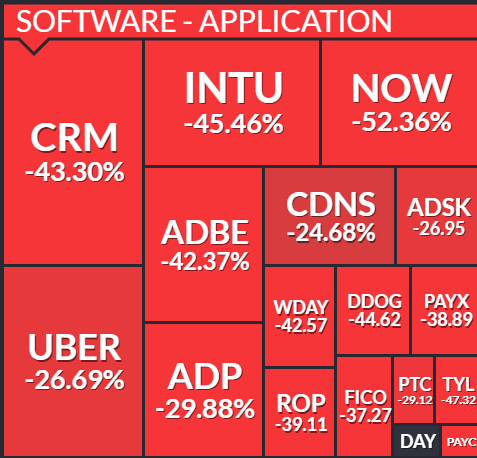

Compression, Not Collapse

Tech isn’t slowing down - but investors are paying less for it.

Earnings across the sector are still growing at one of the fastest clips in the market, up roughly 30% year over year. The weakness we’ve seen hasn’t been about profits collapsing. It’s been about valuations resetting. Forward multiples have compressed sharply as investors rethink how much they’re willing to pay for future growth.

Two forces are driving that reset.

First: AI disruption fears.

The very technology that powered the rally is now raising uncomfortable questions. New AI tools are automating tasks across legal, marketing, finance, and other functions long dominated by established software firms. Investors are wondering whether parts of the software stack could be pressured - or even displaced - faster than incumbents can adapt.

Software Stocks drawdown from 52 week high:

So far, the selling has been broad and largely indiscriminate. In some cases, valuations may already reflect a heavy dose of disruption risk relative to current fundamentals. Industry leaders argue AI will build on existing platforms rather than replace them outright. But the reality is clear: some companies will emerge stronger, others weaker - and it’s still too early to know which is which. That uncertainty is fueling volatility.

Second: the AI spending race.

At the same time, mega-cap tech companies are ramping up capital expenditures at an extraordinary pace. Data centers, chips, infrastructure - the buildout is massive. What used to be capital-light businesses are now investing at industrial scale.

That spending supports parts of the market, especially semiconductors and infrastructure plays. It also feeds into broader economic growth. But it comes with risk. Investors are beginning to ask whether the returns on this AI arms race will justify the scale and speed of investment - particularly as some firms lean more on debt to fund expansion.

In short, this isn’t an earnings problem. It’s a confidence and valuation adjustment.

The AI story isn’t over. But the market is no longer willing to price it as a straight line higher.

When Speculation Cools

Speculation is losing steam.

Some of the market’s most momentum-driven trades have rolled over in recent months. Bitcoin has fallen sharply from its highs, and precious metals - after a powerful run - have also pulled back. While gold and silver remain above year-ago levels, the easy upside appears to have stalled.

This shift adds to the broader risk-off tone we’re seeing across markets. Part of the cooling may reflect the Fed’s recent messaging: rate cuts are unlikely to arrive quickly. When liquidity expectations reset, speculative assets often feel it first.

When speculation cools, discipline matters more than ever.

Earnings Week

Join 120,000+ investors on YouTube! 🎥

We break down earnings, market moves, and exclusive insights you won’t find anywhere else.

Don’t miss out - hit the button below to watch and subscribe now! 👇

YouTube Channel 🔔

Subscribe today and stay ahead of the market!

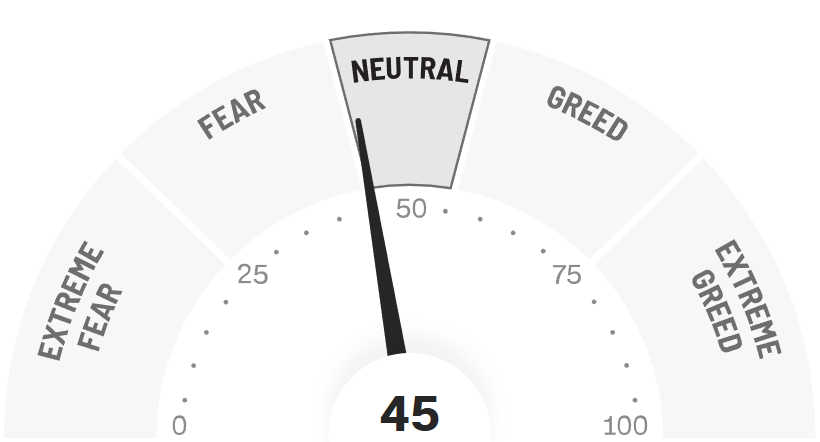

Fear & Greed Index

🔒 This section contains full valuation models, buy zones, and downside scenarios for all Mag7 stocks. Paid members unlock the complete research below.

The Question That Matters

All of this - the rotation, the multiple compression, the AI spending surge, the cooling risk appetite - feeds into one thing:

What are the Magnificent 7 actually worth today?

If leadership is broadening…

If multiples are compressing…

If capital intensity is rising…

Then fair value changes.

So I ran updated discounted cash flow models on each of the Magnificent 7 - using revised growth assumptions, margin scenarios, and a higher-for-longer rate backdrop.

Here’s what the numbers say.

1. Microsoft (MSFT)

Valuation

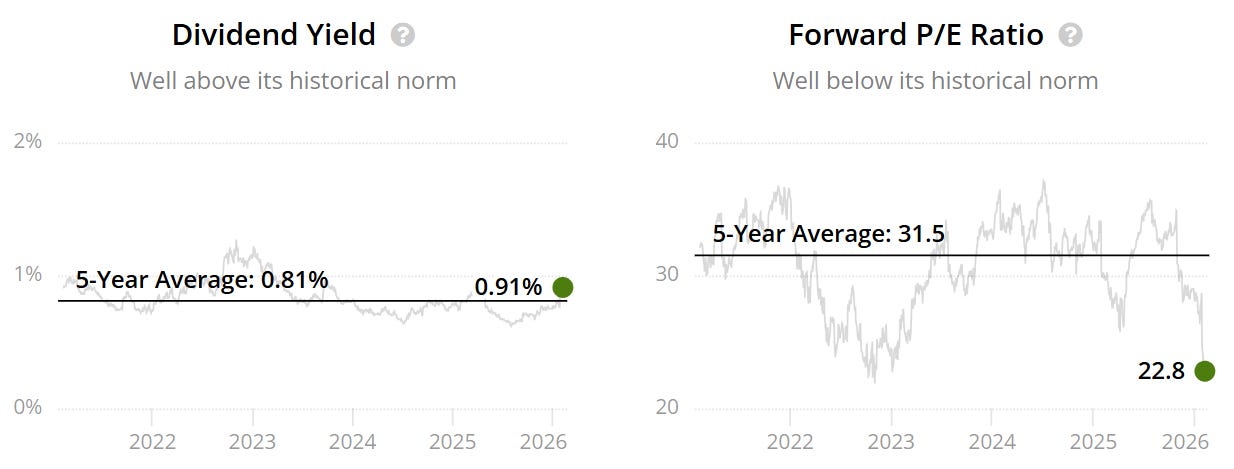

The forward P/E sits below the historical - 22.8x v 31.5x. This could indicate the company is potentially severely undervalued. It is also one of the lowest valuations they have traded for in at least the last 5Y.

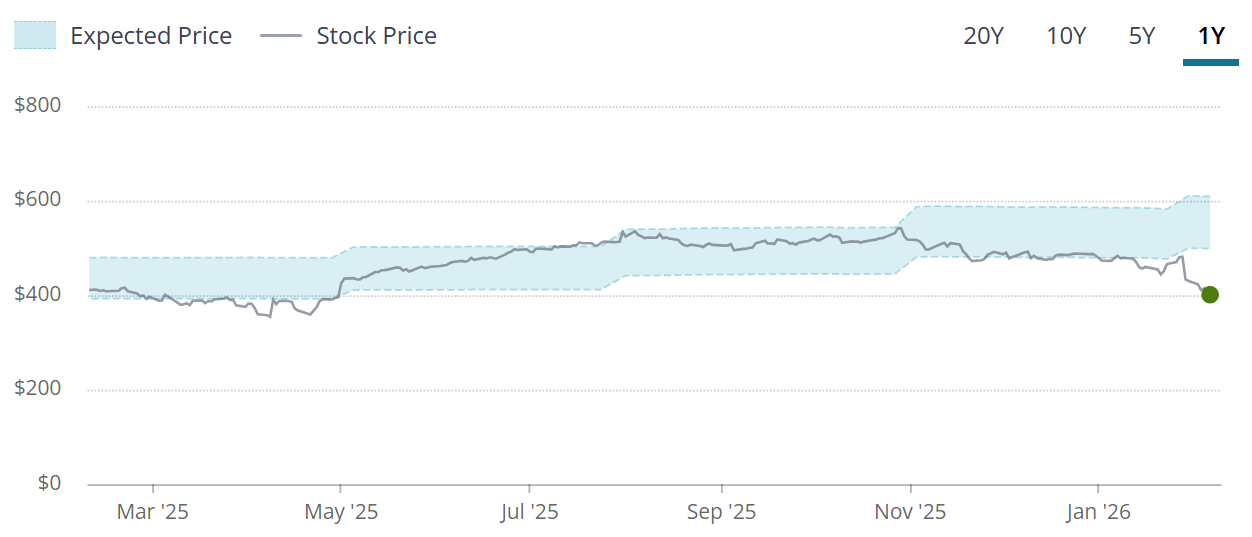

The blue tunnel highlights that Microsoft is now outside of the fair value boundary indicating potential undervaluation.

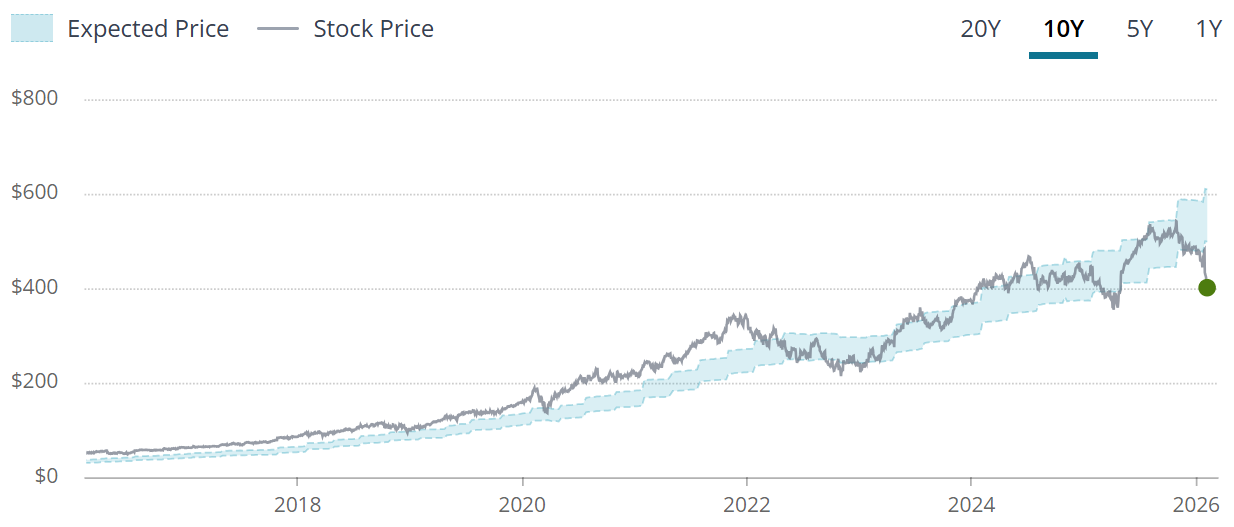

Looking at the last 10Y we note that Microsoft rarely trades at a massive discount.

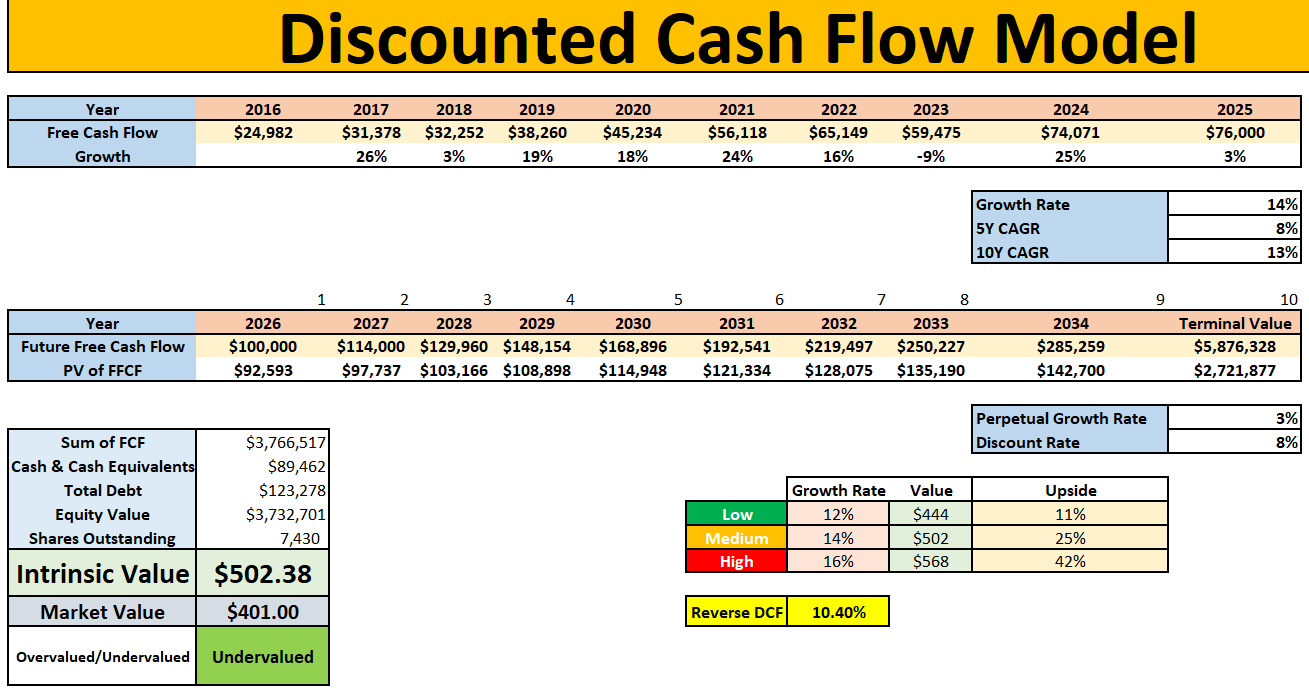

DCF Model

Using our DCF model a few things to note:

10.40% is baked into the FCF growth moving forwards.

5Y FCF CAGR sits at 8%

10Y CAGR sits at 13%

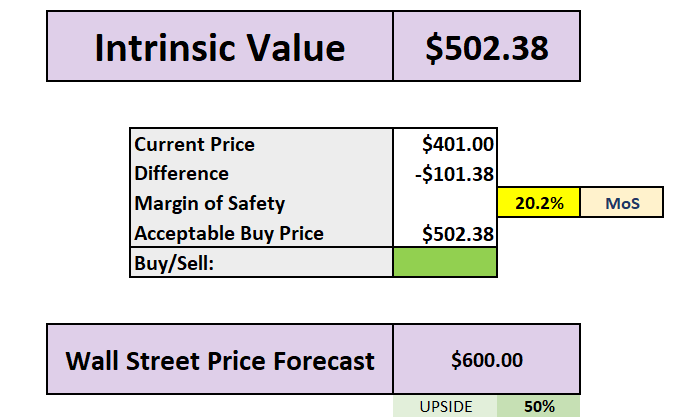

Using 12% (the lower rate) gives an intrinsic value of $444.

Using 14% (the middle rate) gives an intrinsic value of $502.

Using 16% (the higher rate) gives an intrinsic value of $568.

Using the middle growth rate of 14%, we get an intrinsic value of $502 which leads to a 20% margin of safety.

On average wall street see 50% upside by the end of 2026.

What the market is pricing in

The current valuation implies that growth in Azure and enterprise software decelerates meaningfully from recent peaks, despite continued margin expansion and strong free cash flow conversion.

The market appears to be pricing Microsoft as a mature platform rather than a structural AI beneficiary.

If AI-driven productivity gains sustain even mid-teens cash flow growth, today’s multiple leaves room for upside without requiring heroic assumptions.

Verdict: BUY

🔒 The rest of this analysis includes full DCF models, upside/downside scenarios, and exact buy zones for the remaining Magnificent 7.