I Re-Ran a DCF on the Magnificent 7 — Here’s What Changed

Which mega-caps still justify their price?

Most investors do not lose money by buying bad businesses.

They lose money by overpaying for great ones.

That is especially true with the Magnificent 7.

These are some of the best companies in the world. But great businesses do not automatically make great investments. What matters is what is already priced in.

Two months ago, I ran discounted cash flow models across all seven names to see which ones still offered real margin of safety.

Since then, prices have moved. Expectations have shifted. Sentiment around AI, capital spending, and mega-cap tech has changed again.

So I ran the numbers again.

The question is not which businesses are high quality. We already know they are.

The real question is:

Which of these stocks still justify their valuation today - and which ones still require too much optimism?

In this update, I revisited each of the Magnificent 7 using refreshed assumptions around growth, cash flow, and valuation.

Some still look attractive.

Some look closer to fair value.

And a few still look priced for more perfection than I am willing to pay for.

Before getting into each stock, here is the key point:

This is no longer a market where investors can buy mega-cap tech blindly and assume valuation does not matter.

Multiples have already started to compress in parts of the market. Expectations are getting tighter. And as that happens, the gap between great company and great stock matters more.

That is why I wanted to rerun the models now.

Because when leadership narrows, pricing changes fast.

And when pricing changes fast, expected returns can change with it.

What Changed?

Compared with my last review, three things matter most:

1. Prices moved.

Even when the business stays the same, a different starting price changes the return profile.

2. Expectations shifted.

Some of these names are no longer being priced like unstoppable straight-line winners. That creates opportunity in a few cases - but not all.

3. Valuation dispersion is widening.

The Magnificent 7 are often discussed as one group, but the market is not valuing them that way anymore. Some now look far more attractive than others.

That makes this a much better environment for selective buying - and a worse one for lazy buying.

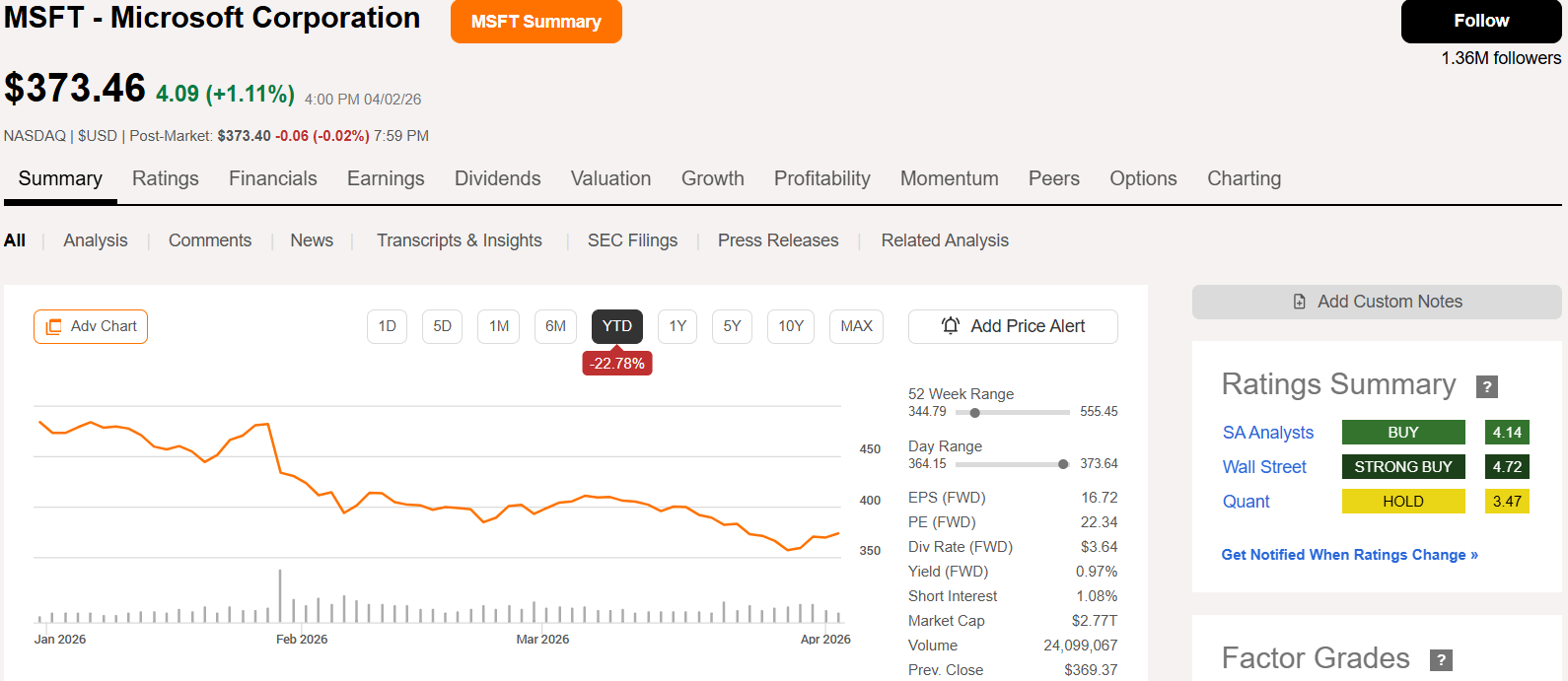

Microsoft (MSFT)

Valuation

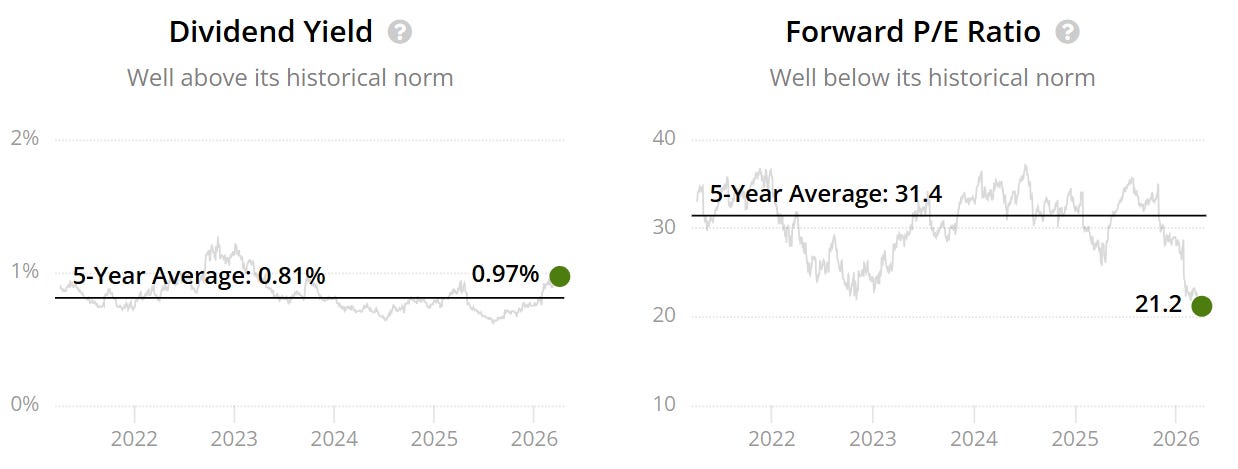

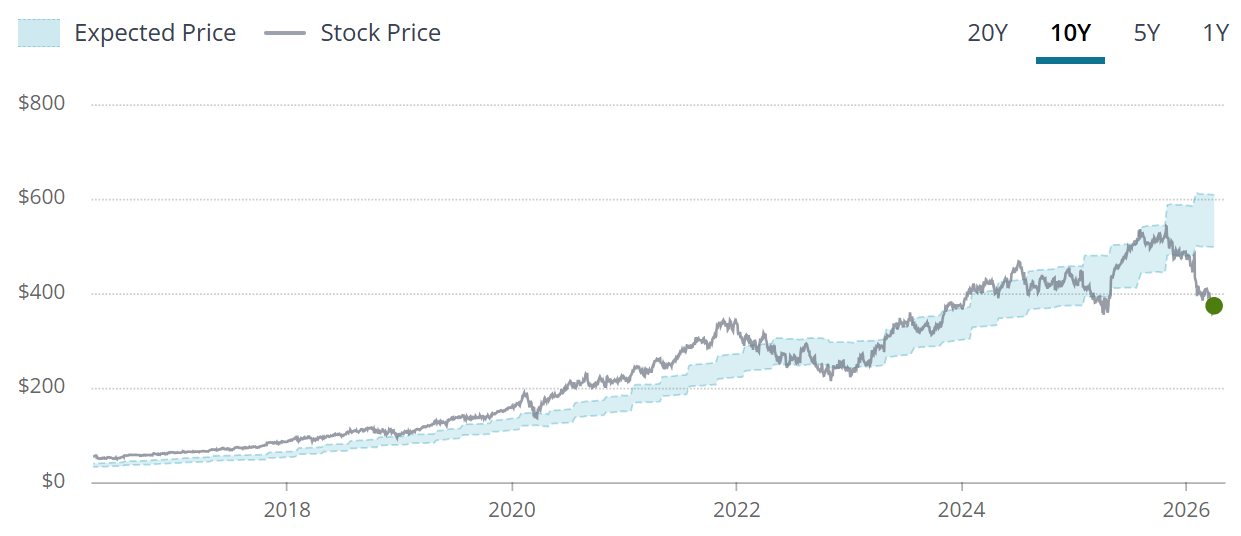

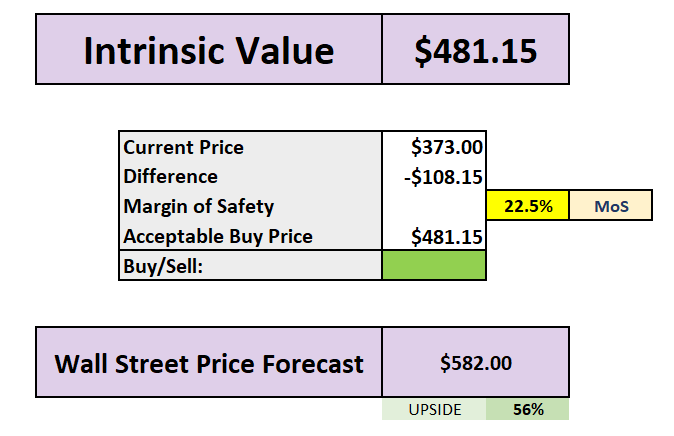

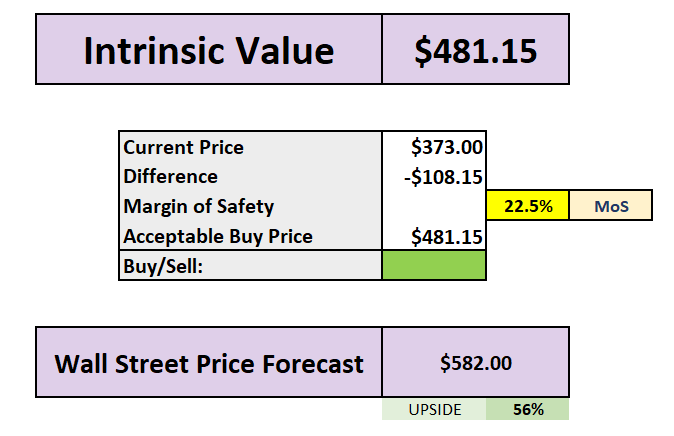

Microsoft now trades at roughly 21x forward earnings, well below its 5-year average of 31x.

That is a meaningful reset for one of the market’s highest-quality businesses and immediately puts the stock back into serious consideration from a valuation perspective.

The setup is simple: this is not a broken business trading cheaply for a reason. It is a premium business that has become materially less expensive.

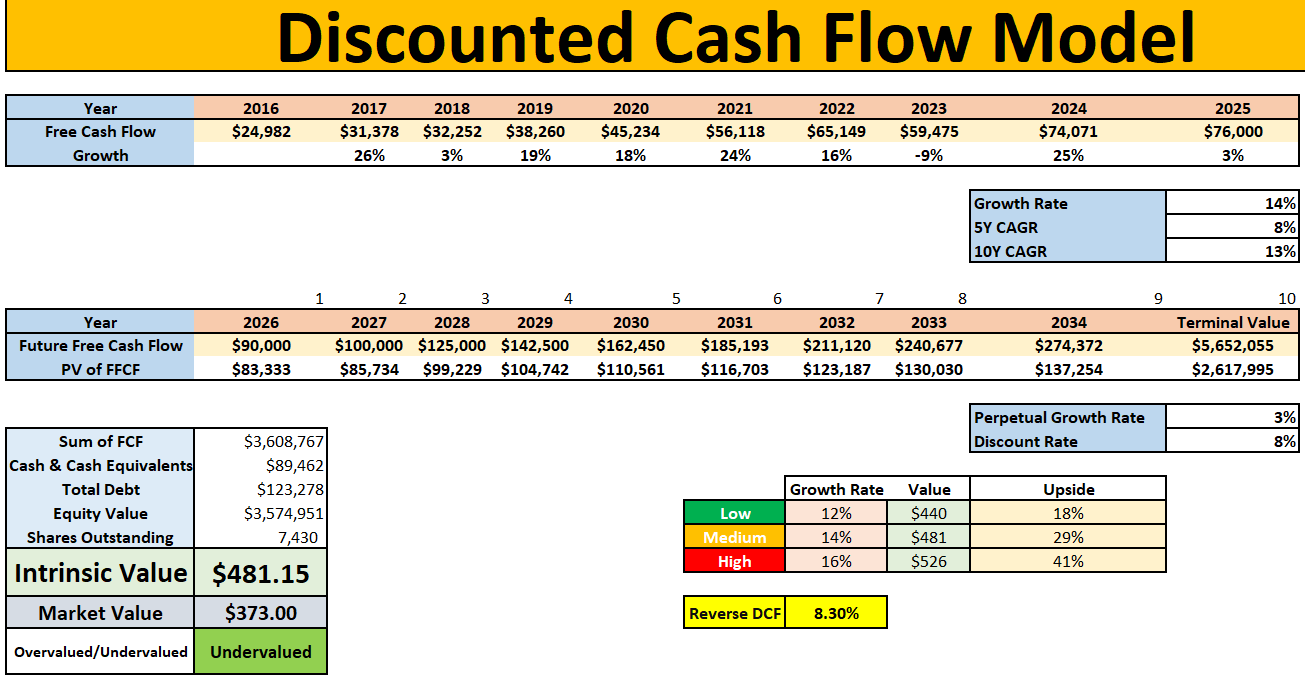

DCF Snapshot

Reverse DCF / implied growth: 8.3%

5Y FCF CAGR: 8%

10Y FCF CAGR: 13%

Low case intrinsic value: $440

Base case intrinsic value: $481

High case intrinsic value: $526

Current price: ~$373

Margin of safety: ~22.5%

What Changed

Since my last review, the main change is straightforward: the stock price fell and the multiple compressed.

That matters because expected returns improve when the entry price drops, even if the business itself remains largely intact. In Microsoft’s case, the reset in valuation has made the stock more interesting without requiring a dramatic change in the underlying thesis.

What the Market Is Pricing In

At today’s price, the market appears to be assuming a much more moderate growth path than Microsoft has historically delivered. The reverse DCF suggests the stock only needs to compound free cash flow at roughly 8.3% to justify the current valuation.

For a business with Microsoft’s scale, recurring enterprise relationships, cloud exposure, and AI optionality, that hurdle does not look especially demanding.

In other words, the market is no longer pricing Microsoft like an untouchable compounder. It is pricing it much closer to a mature platform - and that is where the opportunity starts to improve.

My Take

Microsoft remains one of the highest-quality businesses in public markets, and the valuation is finally starting to reflect more caution than confidence.

That does not mean the stock is risk-free. Expectations around Azure, AI monetisation, and enterprise demand still need to be met. But when a business of this quality trades materially below its historical multiple, while still offering a base-case value comfortably above the current price, the risk/reward becomes far more attractive.

Verdict

BUY

Microsoft is currently my #3-ranked stock in the Magnificent 7.

Microsoft is one of the few names where the recent reset has clearly improved the setup. But across the rest of the Magnificent 7, the picture is far less uniform. Some still offer real upside. Others still look priced for more optimism than I’m willing to pay for.

Below, I break down the remaining six names - including which are still buys, which now look closer to fair value, and which still do not offer enough valuation support at today’s prices.

Paid members unlock the remaining 6 stocks, full fair values, and my complete ranking.