I Re-Ran My DCF Models on 6 AI Chip Stocks — Only 2 Passed

The AI semiconductor trade is starting to split, so I updated my fair value models to find out which stocks still offer real upside.

The AI Chip Trade Is Finally Splitting

The AI trade is no longer moving as one.

For most of the last few years, investors could almost treat the entire AI infrastructure basket as a single trade. Nvidia, Broadcom, Micron, AMD, semiconductor equipment, data centres, power infrastructure, hyperscalers - if it had any connection to AI spending, the market was willing to bid it higher.

But that is starting to change.

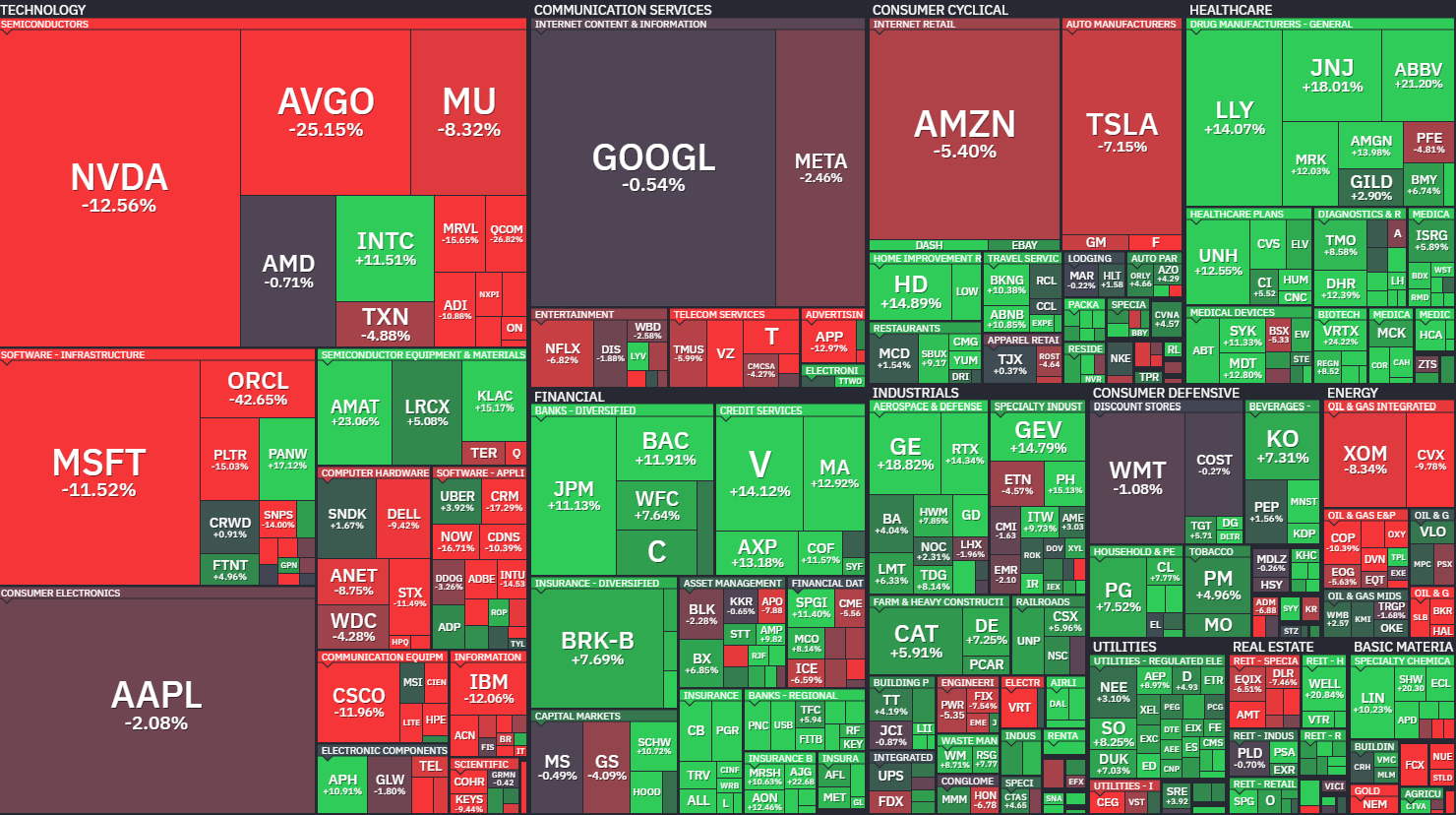

The AI trade is starting to split. Some of the biggest semiconductor winners are selling off, while other parts of the supply chain are still holding up.

Over the past month, some of the biggest AI winners have started to sell off sharply.

Nvidia is down around 13%.

Broadcom is down around 25%.

Micron is down around 8%.

Oracle is down more than 40%.

Microsoft is down more than 11%.

And yet, not everything in the AI supply chain is falling.

Applied Materials is still up strongly.

KLA is still holding up.

Intel has rallied.

Parts of the semiconductor equipment trade are still green.

That is the important point.

This is no longer a market where every AI-related stock is being rewarded equally. The market is starting to separate the companies with durable earnings power from the companies where expectations may have moved too far, too fast.

Before we get into the models, a quick note.

If you enjoy deep-dive valuation work like this, you can subscribe below. I publish regular DCF models, fair value estimates, stock screens, dividend dashboards, and premium stock rankings for investors who want to cut through the noise.

Premium members get access to:

My full DCF assumptions

Bear, base and bull case fair values

Margin of safety estimates

Ranked stock lists

Monthly undervalued stock dashboards

High-upside DCF model updates

The stocks I think offer the best risk/reward today

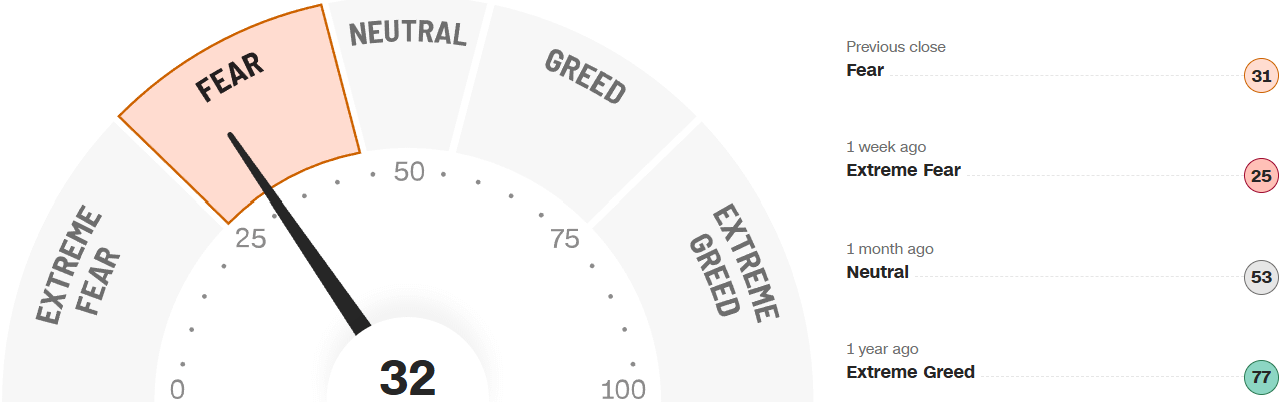

The Market Is Strong — But Fear Is Back

The strange thing is that this sell-off is happening while the broader market still looks strong.

The S&P 500 is up roughly 9.5% year-to-date, almost exactly in line with its long-term average annual path.

Over the past year, the S&P 500 has also delivered a return of around 31%, which is a very strong one-year move by historical standards.

But under the surface, sentiment has weakened.

The Fear & Greed Index is sitting in fear territory, around 32. One month ago, it was neutral. One year ago, it was in extreme greed.

That shift matters.

When sentiment is euphoric, investors often stop asking whether the valuation makes sense. They simply chase the story. But when fear returns, the market starts asking a much harder question:

How much future growth is already priced in?

That question is especially important for AI chip stocks.

Because these are not bad businesses. In many cases, they are some of the highest-quality businesses in the market. The issue is that even a great company can become a poor investment if the expectations are too aggressive.

Market sentiment has cooled sharply, even while the broader index remains up strongly this year.

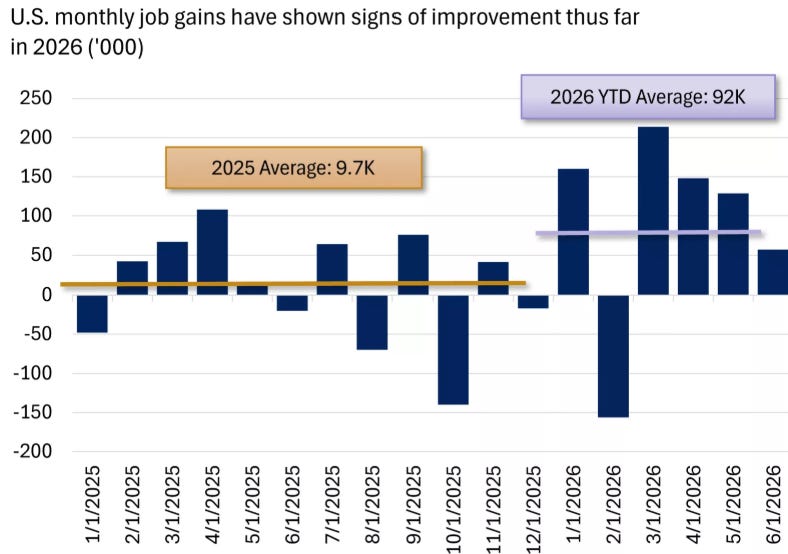

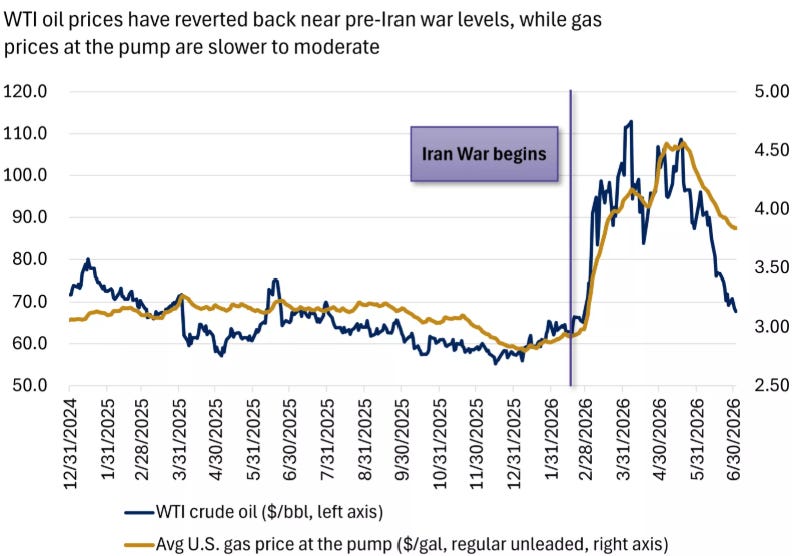

The Economy Is Not Falling Apart

The macro backdrop is still fairly supportive.

The labour market has been bumpy, but it has not collapsed. Monthly job gains in 2026 have averaged around 92,000, compared with roughly 9,700 in 2025. That is not a booming labour market, but it is still enough to support consumer spending and keep the economy moving forward.

Oil has also cooled off. WTI crude has fallen back near pre-Iran war levels, which should help ease some pressure on inflation and consumers if gas prices follow with a lag.

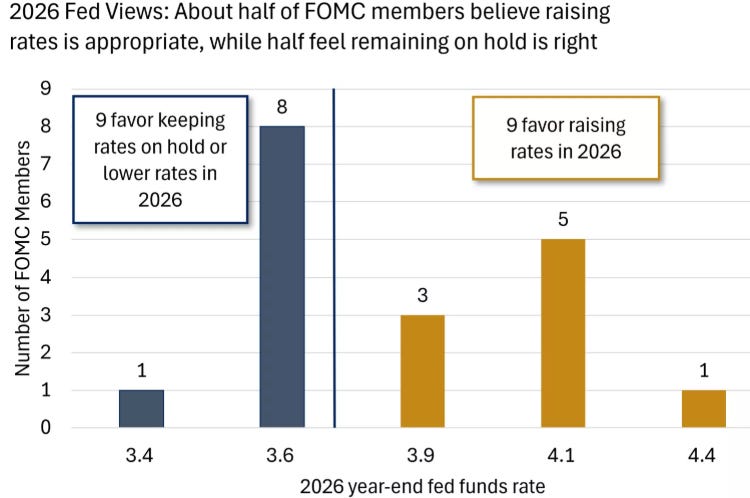

The Fed remains split. Around half of FOMC members appear to think rates should stay on hold or move lower in 2026, while the other half think raising rates may still be appropriate. So this is not a perfect environment, but it is also not an obvious recession setup.

That is why this market is so interesting.

The economy is not broken.

The market is not collapsing.

AI spending is still real.

But valuations are starting to matter again.

And that is exactly the kind of environment where DCF work becomes useful.

The Bull Market Is Broadening Away From the Mag 7

One of the biggest changes this year is that the market is no longer being driven only by the Magnificent 7.

The Russell 2000 is up strongly.

The equal-weight S&P 500 is outperforming the cap-weighted index.

Small caps, mid caps, value stocks, and non-Mag 7 names have all started to participate.

This is important because it tells us the market is not simply saying, “AI is over.”

Instead, the market seems to be saying:

“We still like growth. We still like risk assets. But we are no longer willing to pay any price for the same narrow group of mega-cap winners.”

That is a much healthier market, but it is also a more dangerous one for overvalued AI stocks.

In 2023 and 2024, the market rewarded the AI story almost regardless of valuation. In 2026, that is changing. Investors are still willing to pay for AI exposure, but only where the numbers make sense.

AI Is Still the Centre of the Market

Even with the recent sell-off, AI remains one of the most important forces inside the S&P 500.

One chart I found especially interesting shows that AI-related stocks now make up roughly 45% of the S&P 500’s market cap.

Another shows the broader AI complex rising from 37.5% of the index at the end of 2025 to 42.3% by mid-2026.

Semiconductors and semiconductor capital equipment alone have become a much larger part of the index. According to one chart, semiconductor weight in the S&P 500 has climbed to almost 20%, far above previous cycles.

That is both bullish and risky.

Bullish because it shows how important AI infrastructure has become.

Risky because when one theme becomes this large, small changes in expectations can have a huge impact on the entire market.

This is why I do not want to simply say, “AI stocks are down, therefore they are cheap.”

That is lazy.

The better question is:

Which AI chip stocks still have enough future free cash flow growth to justify their current valuation?

That is what today’s article is trying to answer.

The AI Spending Boom Is Still Real

The strongest argument for the AI trade is that the spending boom has not disappeared.

Data centre construction spending in the U.S. has now eclipsed $50 billion, and private data centre construction has surged over the last few years. This is not just a stock market narrative anymore. Real capital is being deployed into real infrastructure.

That matters for semiconductor demand.

AI chips are not just a software story. They sit at the centre of a much larger physical buildout:

GPUs

custom accelerators

high-bandwidth memory

networking chips

semiconductor equipment

advanced packaging

data centres

cooling

power infrastructure

So yes, the long-term AI infrastructure story is still very much alive.

But here is the problem.

A great long-term story does not automatically equal a great stock today.

If a stock already prices in years of perfect execution, the risk/reward can still be poor. If margins are already near peak levels, revenue growth needs to stay extremely high for a long time. And if the market starts questioning the pace of AI capex, even the best companies can see sharp multiple compression.

That is why valuation matters most when the story sounds most obvious.

The Other Side: Crowding Risk Is Rising

There is also a clear risk building beneath the surface.

Prime brokerage data suggests investors have recently been net sellers of U.S. information technology. The chart from Goldman Sachs showed a very sharp negative reading in weekly net trading flow for U.S. Info Tech.

That does not mean AI stocks have to crash.

But it does show that the trade has become more fragile.

When everyone owns the same theme, the downside can move quickly. And when the most crowded stocks start missing expectations, even slightly, the market can punish them very aggressively.

This is why I think the next phase of the AI trade will be much more selective.

The question is no longer:

“Which companies benefit from AI?”

That list is too broad.

The better question is:

“Which companies benefit from AI and still offer attractive upside after updating the assumptions?”

That is a much smaller list.

So I Re-Ran My DCF Models

That brings us to today’s screen.

I re-ran my DCF models across 6 AI chip stocks to see which names still offer attractive risk/reward after the recent moves.

For each company, I looked at:

updated revenue growth assumptions

free cash flow growth potential

margin durability

terminal multiple assumptions

discount rate sensitivity

bear, base and bull case fair values

current upside or downside to fair value

margin of safety

The goal was not to find the most exciting AI story.

The goal was to find the best investment setup.

Because those are not always the same thing.

Some of these companies are outstanding businesses, but the valuation still looks stretched. Some have sold off, but not enough to create a real margin of safety. And a few now look much more interesting after the recent weakness.

After updating the assumptions, most of the stocks still failed my screen.

But two passed.

And one stood out as the clearest risk/reward opportunity in the group.

ASML: World-Class Business, But Not Enough Margin of Safety

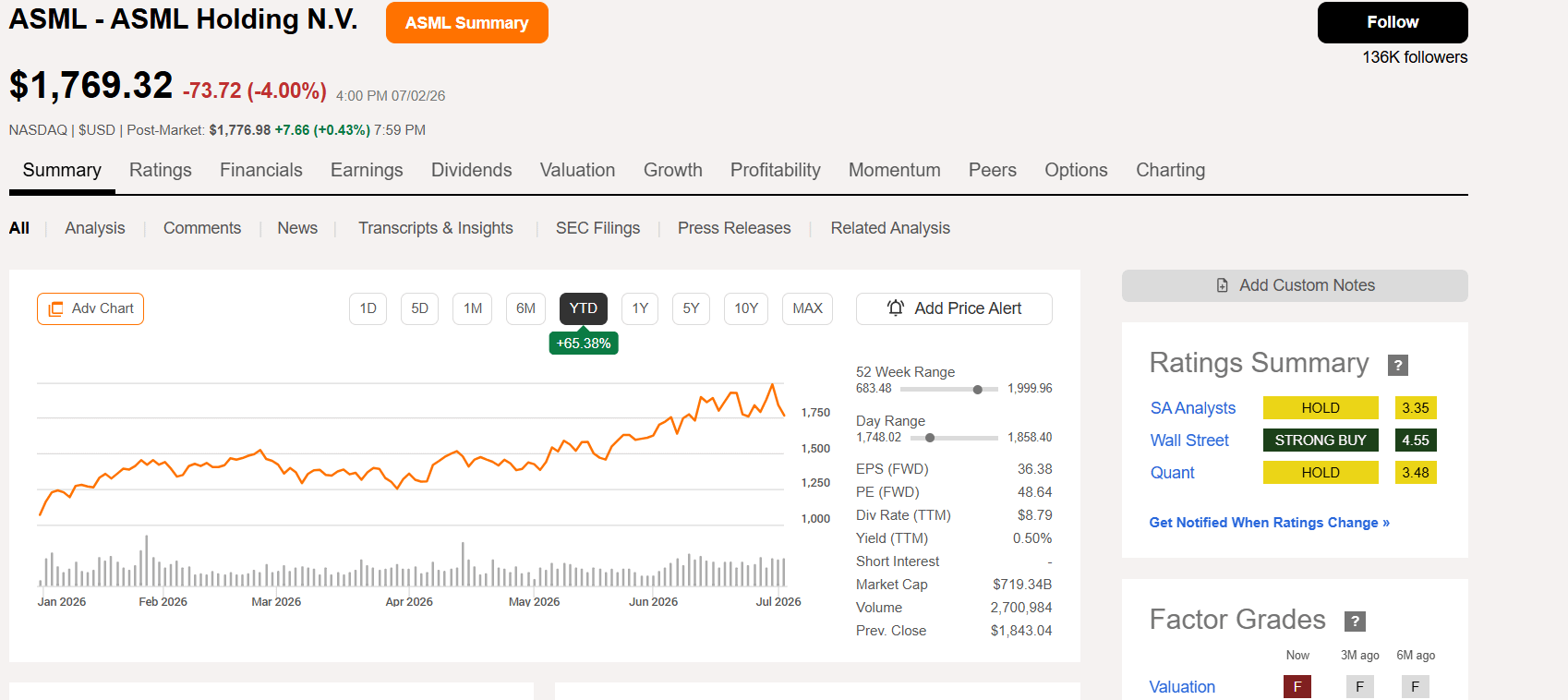

ASML has rallied strongly this year, but the valuation now leaves very little room for error.

Before we get into the full paid screen, I want to show one example of why this article is not simply about buying every AI chip stock that has exposure to the theme.

And I think ASML is the perfect case study.

ASML is one of the most important companies in the entire semiconductor supply chain. The company dominates extreme ultraviolet lithography, which is essential for producing the most advanced chips in the world. If AI demand keeps growing, the world will need more advanced chips. And if the world needs more advanced chips, companies like TSMC, Samsung and Intel will continue relying on ASML’s machines.

So from a business quality perspective, ASML is exceptional.

But the stock has already moved a lot.

ASML is up around 65% year-to-date. That is the key tension. This is not a stock that has collapsed and suddenly become obviously cheap. It is a high-quality AI infrastructure business that has already been rewarded by the market.

And that makes the valuation much harder.

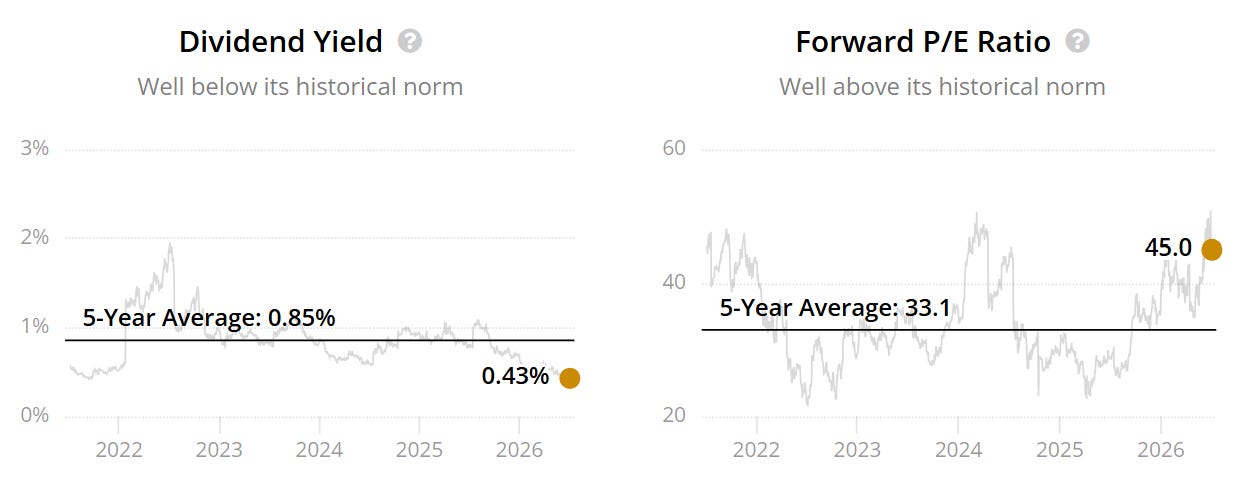

The Market Still Loves ASML

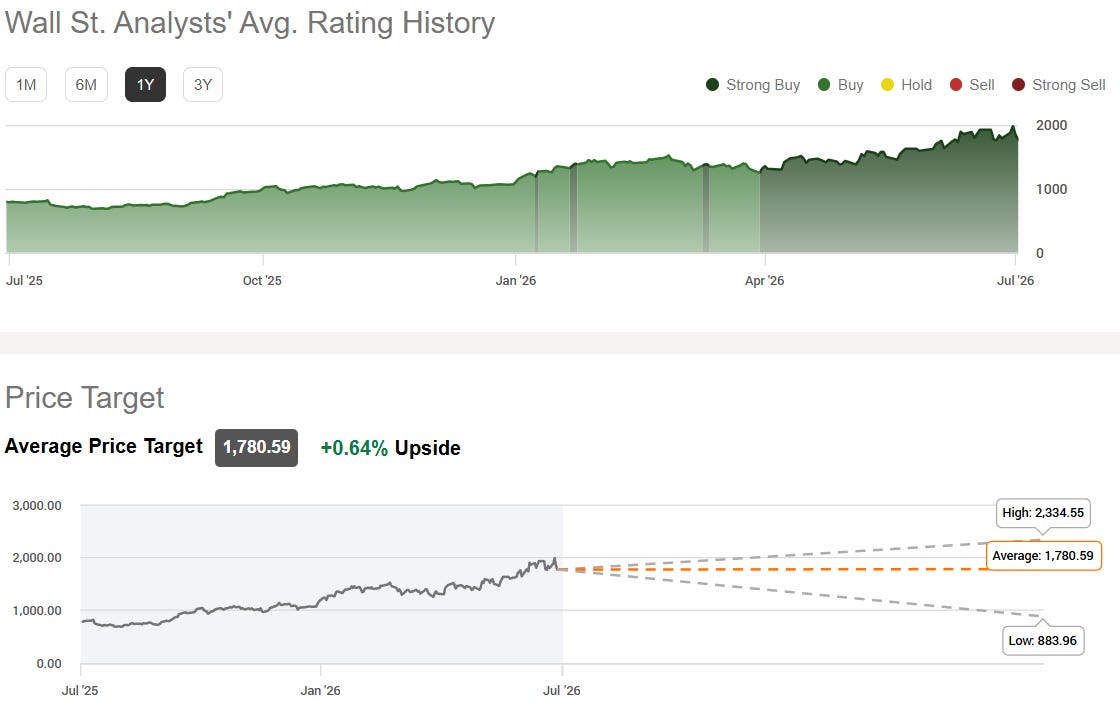

Wall Street remains very positive on the company.

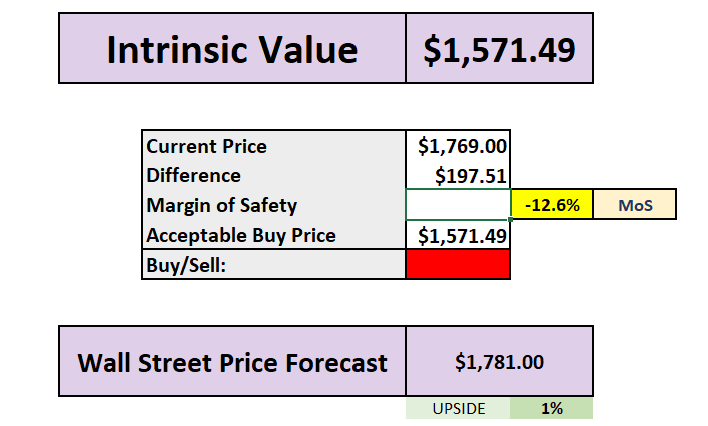

The analyst rating is still sitting at Strong Buy, and the average price target is around $1,781, which is almost exactly where the stock trades today.

That tells us something important.

Analysts clearly still like the business, but the average price target implies almost no upside from the current share price.

So even the bullish Wall Street view is not screaming “bargain” at today’s valuation.

Wall Street still likes ASML, but the average price target implies almost no upside from the current price.

Growth Is Strong — But Expectations Are Already High

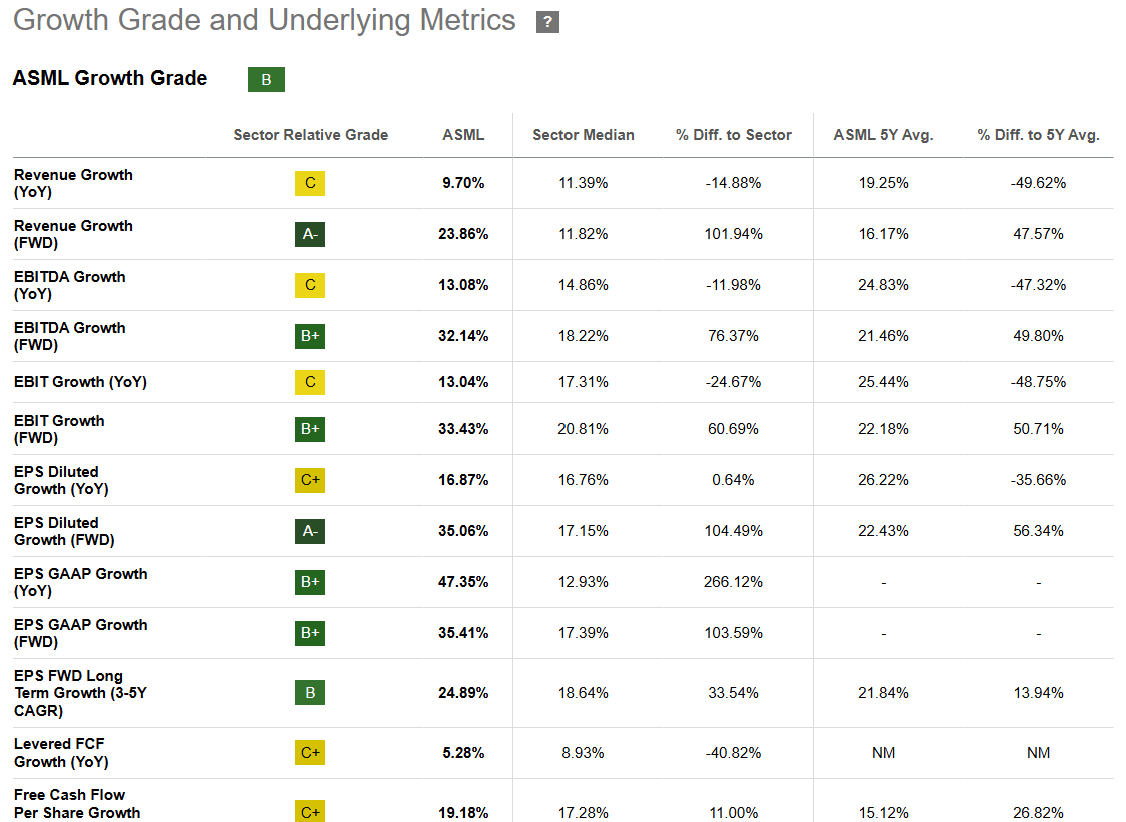

The growth profile is still impressive.

ASML’s forward revenue growth is around 23.9%, forward EBITDA growth is around 32.1%, forward EBIT growth is around 33.4%, and forward diluted EPS growth is around 35.1%.

That is exactly why investors are willing to pay a premium multiple for this business.

But again, the problem is not the company.

The problem is the price.

ASML currently trades at a forward P/E ratio of roughly 45x to 49x, depending on the data source, compared with a 5-year average closer to 33x.

That means investors are not just paying for a great business. They are paying a historically elevated multiple for a great business after a very strong run.

And when a stock already trades well above its historical valuation range, the DCF has to do more work. The future free cash flow growth needs to be strong enough to justify not only the current price, but also the premium multiple already embedded in the stock.

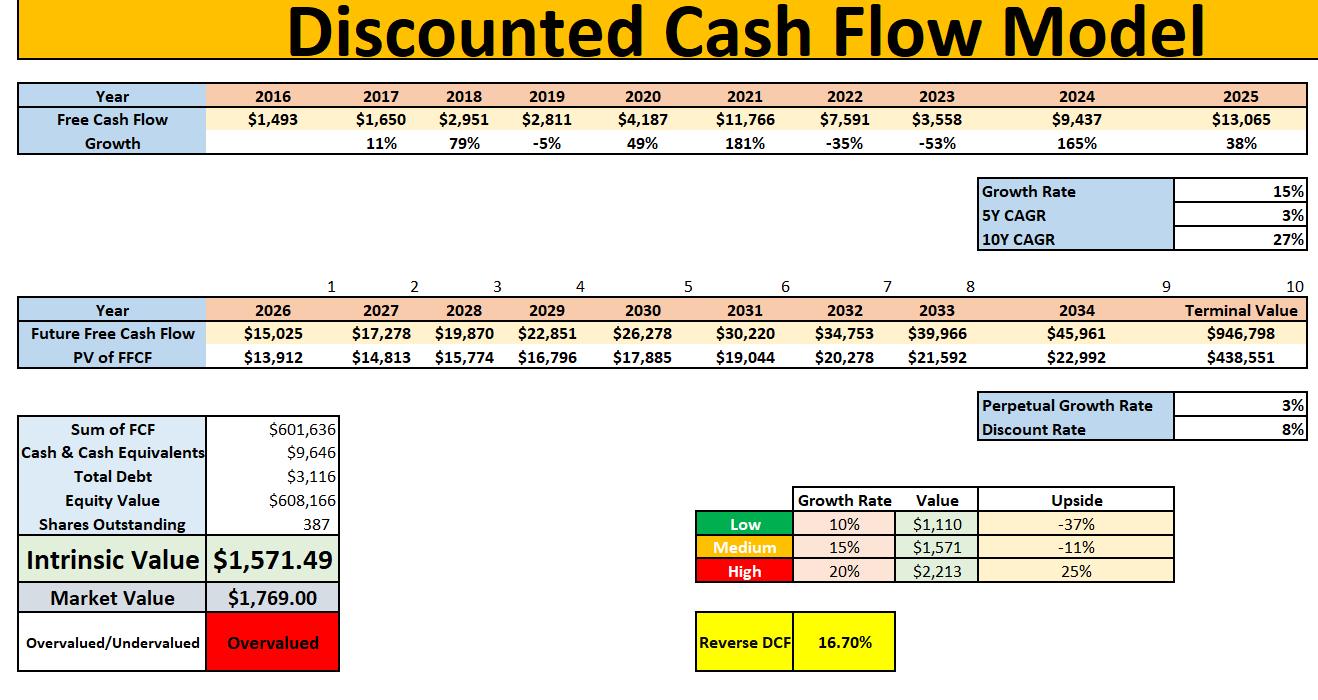

My DCF Result

In my base-case DCF, I assumed ASML can grow free cash flow at 15% annually over the next 10 years, with a 3% perpetual growth rate and an 8% discount rate.

That is not a bearish model.

A 15% free cash flow CAGR for a company of ASML’s size is still a very strong assumption. It reflects the quality of the business, the importance of EUV, and the long-term demand tailwind from AI, advanced chips and semiconductor capacity expansion.

But even with that assumption, my intrinsic value estimate came out at around:

$1,571 per share

Against a current price of roughly $1,769, that implies the stock is trading around 11% above my base-case fair value estimate.

My margin of safety is therefore negative, at around -12.6%.

So based on my model, ASML does not pass.

Reverse DCF: What Is Already Priced In?

The reverse DCF also tells the same story.

At the current price, ASML appears to be pricing in roughly 16.7% annual free cash flow growth over the next decade.

That is possible.

But it is not low-risk.

Especially for a business that is still exposed to semiconductor cycles, customer capex timing, China restrictions, and the broader question of how long AI infrastructure spending can continue at this pace.

This is why ASML failed my screen.

Not because the business is weak.

But because the stock already expects a lot.

My Verdict on ASML

ASML remains one of the highest-quality companies in the semiconductor ecosystem.

It has a dominant competitive position, excellent long-term relevance, strong forward growth expectations, and direct exposure to the most important parts of the AI chip supply chain.

But at today’s valuation, I do not see enough margin of safety.

The stock is already up heavily this year. The forward P/E ratio is above its historical average. Wall Street’s average price target implies almost no upside. And my base-case DCF suggests the stock is trading above fair value.

So for me, ASML is a:

High-Quality Fail

I would happily keep it on the watchlist. But based on my updated assumptions, it was not one of the two AI chip stocks that passed my DCF screen.

Want the full DCF screen?

Premium members get the full breakdown of all six AI chip stocks, including my updated fair value estimates, bear/base/bull cases, margin of safety calculations, and the two stocks that actually passed the model.

And that is the key point of this article.

ASML is a world-class business, and it still failed.

Across the six AI chip stocks I modelled, four failed my updated DCF screen.

Only two passed.

And one stood out as the clearest risk/reward opportunity in the group.