I Screened for Undervalued Dividend Stocks — These 5 Still Look Cheap

Markets are near highs, but my valuation model says a few dividend stocks may still be mispriced.

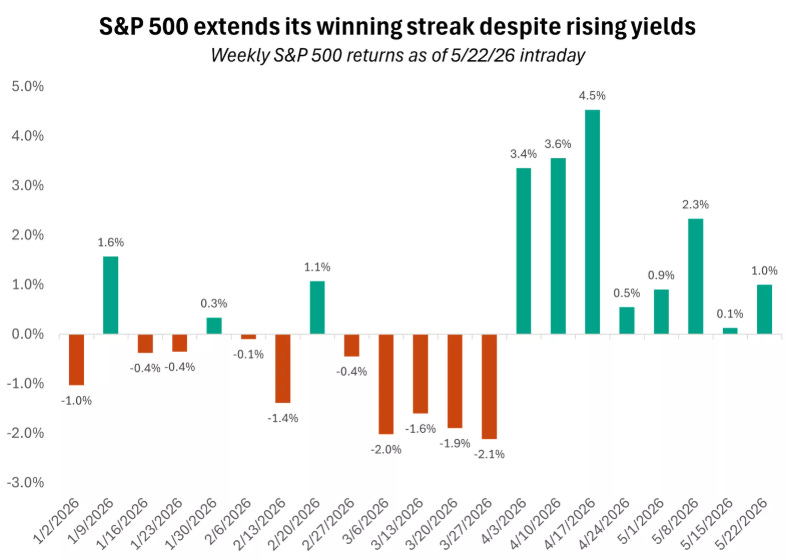

The market has been strong again.

After a difficult stretch earlier in the year, the S&P 500 has continued to recover, and the recent winning streak has been hard to ignore.

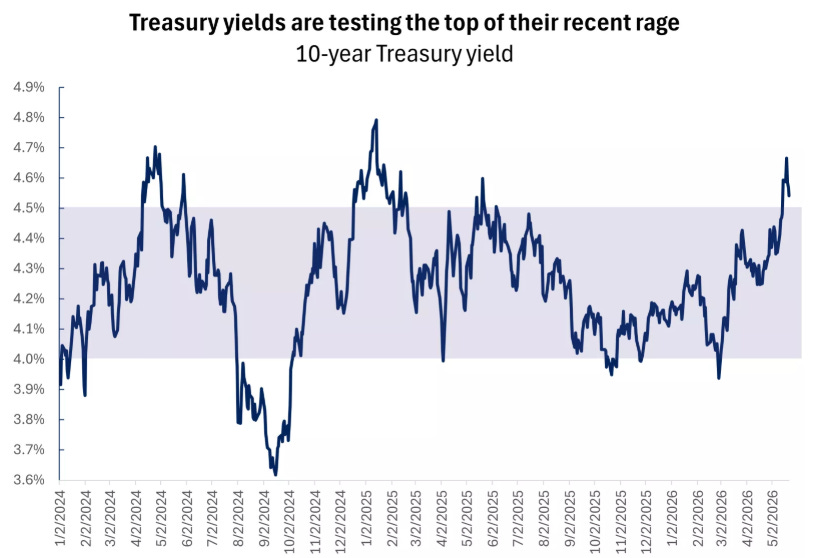

The interesting part is that this rally has happened even while bond yields have moved higher.

That matters.

Higher yields do not automatically kill a bull market, but they do raise the bar for equities. When investors can earn a reasonable return from cash or short-term bonds, they become less willing to pay any price for future earnings.

That is why valuation discipline becomes more important after a rally, not less important.

The 10-year Treasury yield is once again testing the upper end of its recent range. That does not mean stocks have to fall tomorrow, but it does mean investors should be more selective.

This is the environment where I do not want to blindly chase the index.

At the same time, I also do not want to sit completely in cash just because the market has already moved higher.

I prefer a third option:

update the numbers.

Because even when the broad market looks expensive, individual stocks can still be mispriced.

That is especially true when leadership is narrow, sentiment has improved, and investors are paying very different prices for different parts of the market.

The valuation gap is important.

Large-cap indexes are not exactly cheap. But beneath the surface, there are still individual companies trading at more reasonable valuations, especially outside the most crowded parts of the market.

That is what I wanted to test this week.

So I went back through my valuation models and screened for dividend-paying companies where the market price still sits below my estimate of fair value.

I was not just looking for the highest theoretical upside.

A cheap-looking stock is not automatically attractive.

I wanted companies where the valuation, dividend profile, cash flow picture, and business quality still made sense together.

For this article, I focused on companies where my model showed:

a clear discount to fair value

dividend support through either dividend history or dividend modelling

a business that can plausibly recover without needing a perfect macro backdrop

enough upside to justify deeper research

In total, five dividend-paying stocks passed the screen.

Paid subscribers will get the full list, fair value estimates, buy zones, and my ranking below. But first, I want to walk through one example for free readers.

The results were interesting.

One stock had the highest upside in the model, but also the most execution risk.

Two looked like stronger quality/value setups.

One was more of a cyclical turnaround idea.

And one was a lower-upside dividend compounder that I think is a useful free example.

That stock is AbbVie.

I’m choosing AbbVie as the free example because it is not the most explosive name in the screen. It is not the highest-upside stock, and it is not the cheapest.

But it is a good example of how I think about valuation.

The remaining four stocks, including the highest-upside name in the model, are included for paid subscribers below.

AbbVie: A Lower-Upside, Higher-Confidence Dividend Setup

AbbVie is not the cheapest stock in this screen.

It is also not the highest-upside name.

But that is exactly why I think it is useful to discuss before the paywall.

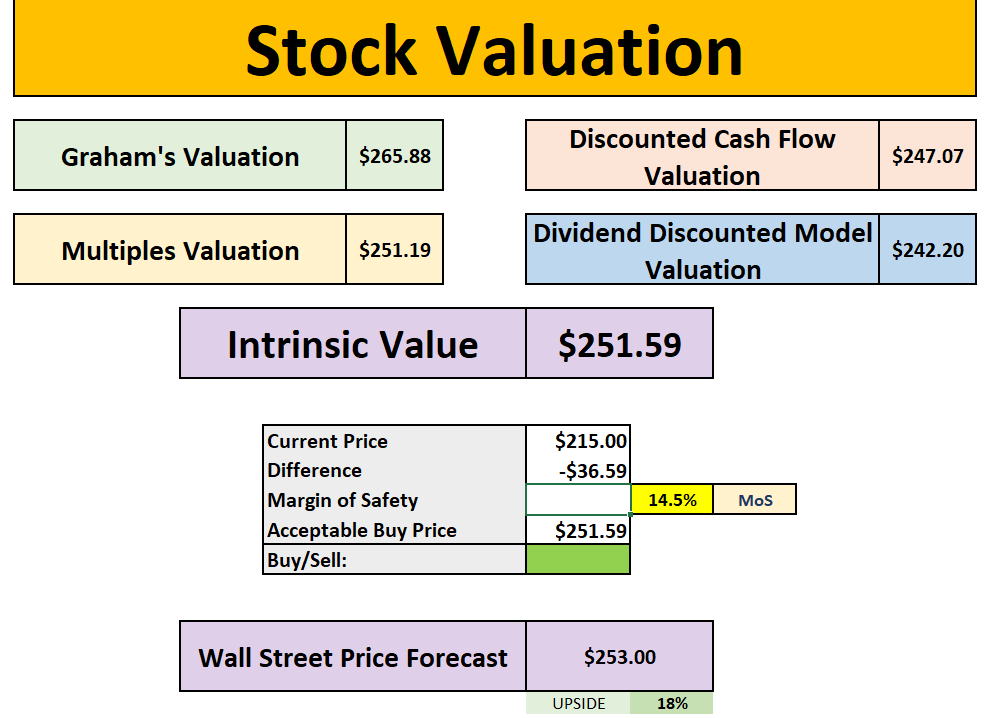

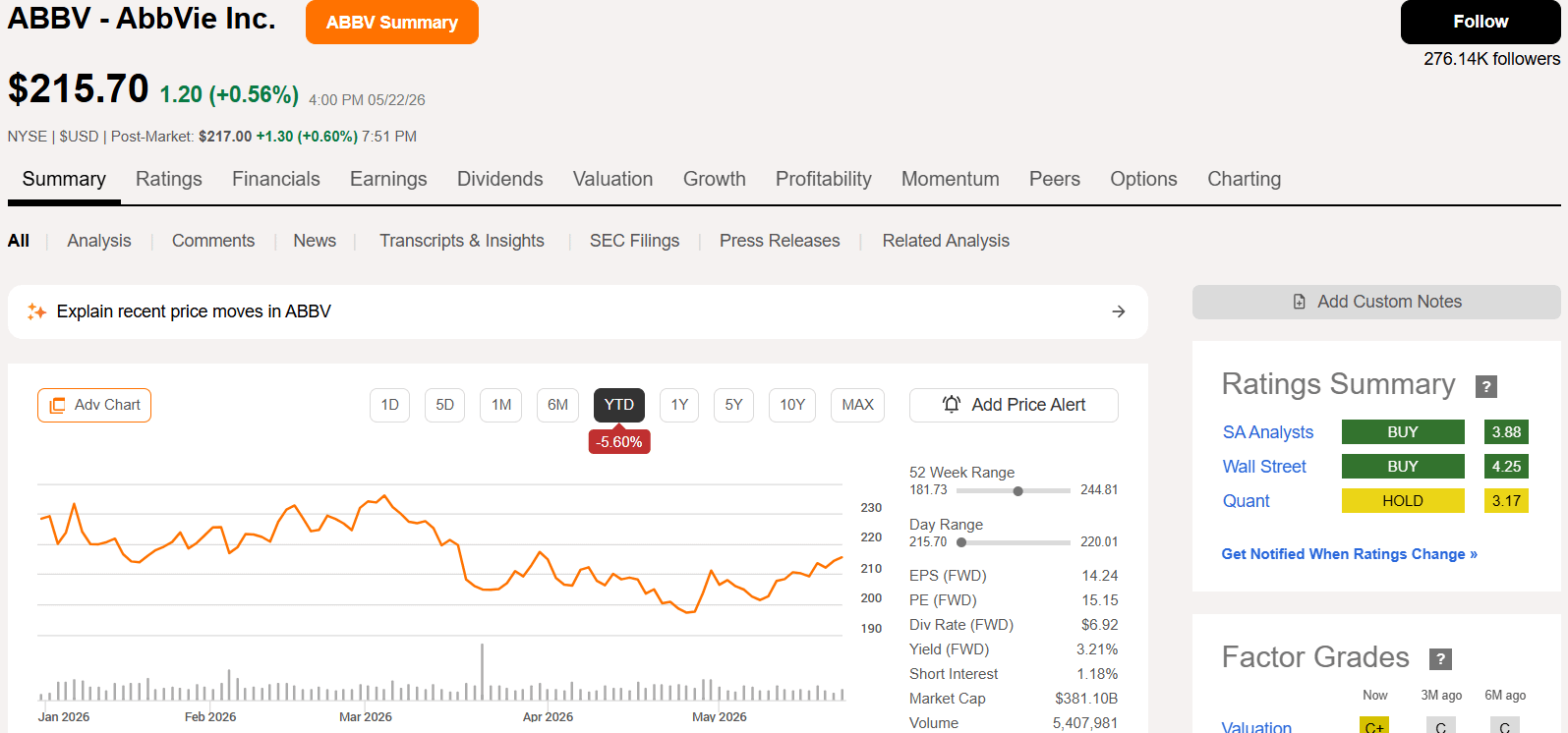

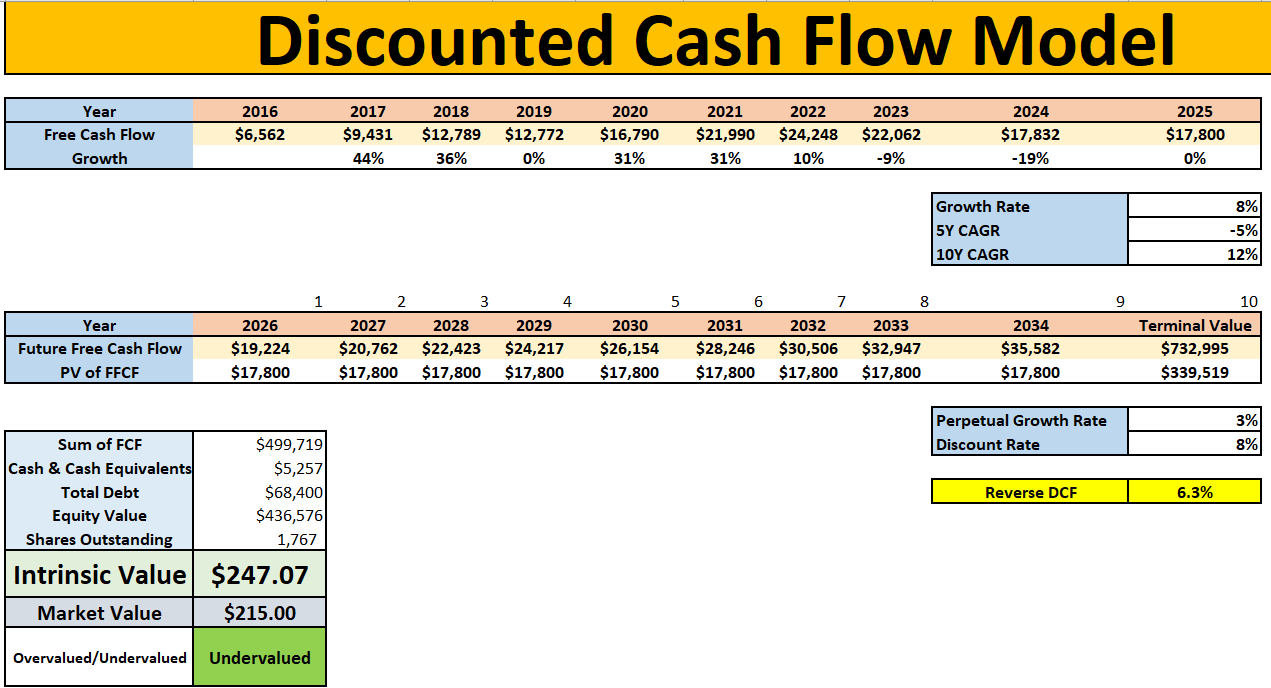

My valuation model estimates AbbVie’s intrinsic value at around $251.59, compared with a recent market price of around $215.

That suggests a margin of safety of roughly 14.5%.

For a deep-value stock, that would not be enough.

But AbbVie is not really a deep-value situation.

This is more of a dividend compounder trading at a reasonable discount to my estimate of fair value.

The valuation is also supported by multiple approaches.

My discounted cash flow model gives a valuation of around $247.07.

The dividend discount model gives a value of around $242.20.

The multiples valuation comes in at around $251.19, while Graham’s valuation is higher at around $265.88.

The exact number is not the point.

The important part is that several valuation methods are pointing in a similar direction.

That does not make AbbVie an automatic buy, but it does make the setup more interesting.

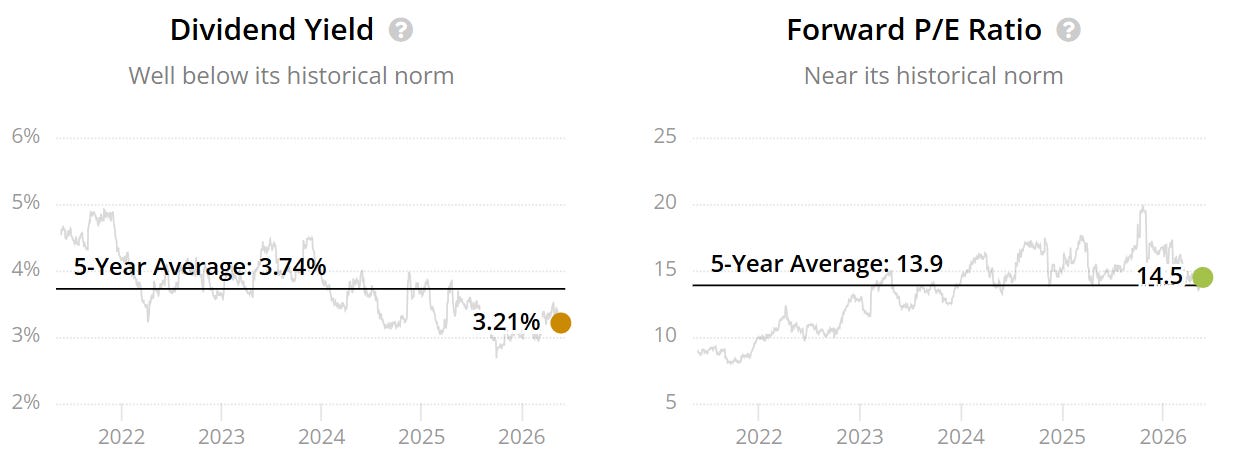

At a recent price of around $215, AbbVie trades on a forward P/E of roughly 15x, with a forward dividend yield of around 3.2%.

That is not screaming bargain territory.

But it also does not look expensive for a profitable, large-cap pharmaceutical company with a meaningful dividend.

The key debate with AbbVie is still the same one investors have been wrestling with for years:

Can the company move beyond Humira?

Humira was a monster drug, and the loss of exclusivity created a real earnings challenge.

That concern was valid.

But the market also knew this was coming. The question today is not whether Humira declines. It already has.

The question is whether AbbVie’s newer portfolio, pipeline, and cash flow can support the next phase of growth.

That is where the setup becomes more interesting.

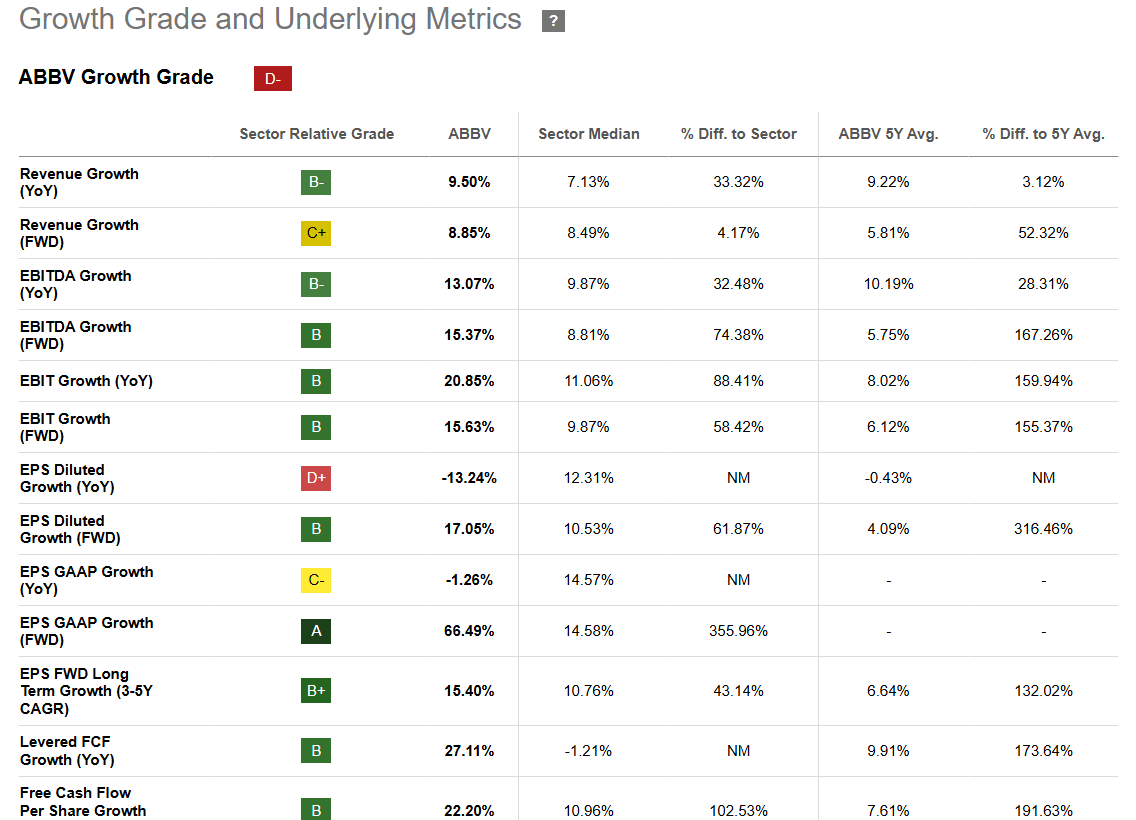

The headline growth grade may look weak, but the underlying metrics are more mixed.

Revenue growth remains positive, forward revenue growth is still respectable, EBITDA growth is strong, and forward EPS growth expectations are not bad.

That tells me the market may still be too focused on the old Humira story, while the actual business is moving through the transition.

Of course, this is not risk-free.

Pharma stocks always come with patent risk, pipeline risk, regulatory risk, and drug pricing pressure.

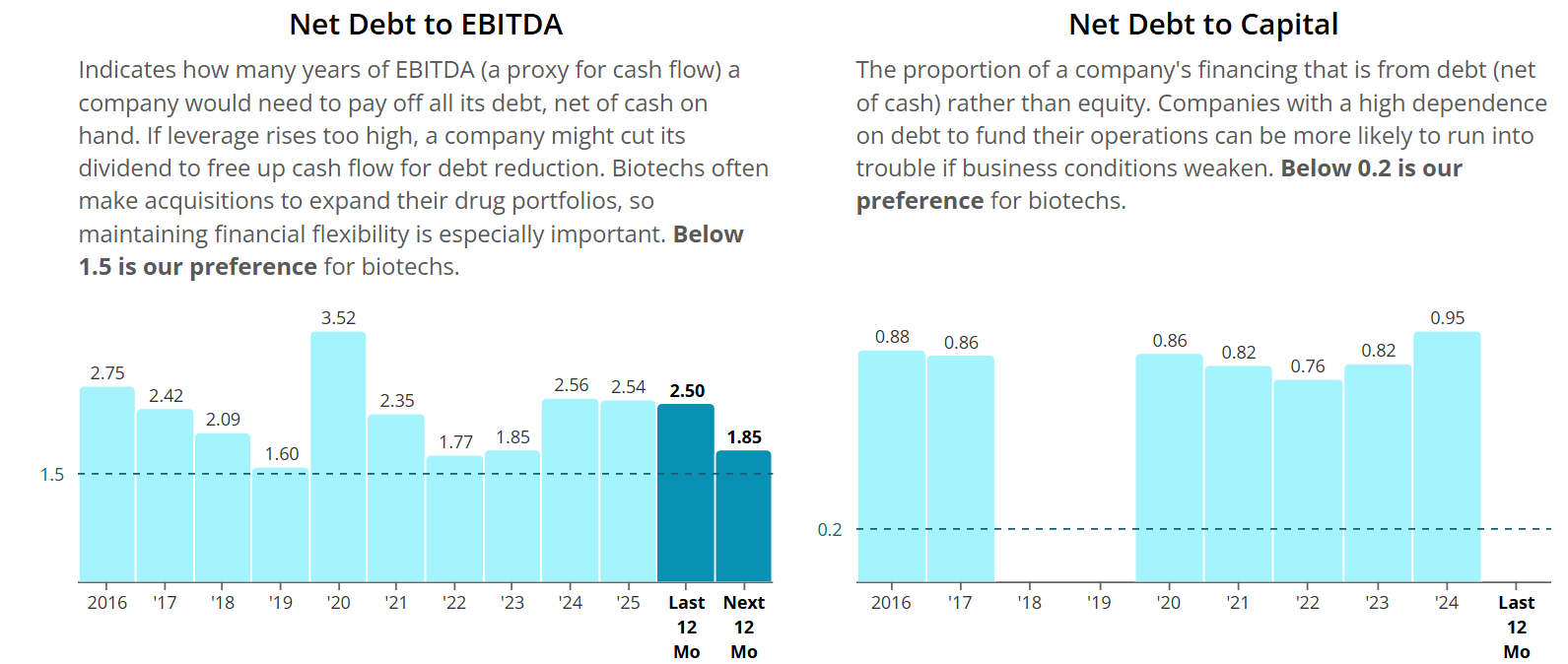

AbbVie also carries leverage, which is something I continue to watch closely.

Net debt to EBITDA has improved versus prior periods, but it is still not as low as I would ideally like.

That does not break the thesis.

But it does mean AbbVie needs to keep generating strong cash flow, supporting the dividend, and managing capital allocation carefully.

For me, the investment case is fairly simple.

AbbVie does not need to be a perfect company to be interesting.

It just needs to keep proving that the post-Humira business can grow, the dividend remains supported, and the valuation remains reasonable.

In my DCF model, I used an 8% discount rate, a 3% perpetual growth rate, and a long-term free cash flow growth assumption of around 8%.

Based on those assumptions, the DCF gives me an intrinsic value estimate of roughly $247 per share.

That is above the current market price, but not by enough for me to call this a screaming buy.

And that is exactly the point.

AbbVie is not the most exciting stock in the screen.

It is the balanced example.

It offers a dividend yield of around 3%, reasonable valuation support, and a business that may still be underestimated if the post-Humira portfolio continues to deliver.

But the margin of safety is not huge.

So I would still be disciplined on price.

For me, AbbVie is the kind of stock that could make sense for dividend investors who want quality and income, but do not want to rely on a full turnaround story.

The bigger question is whether any of the other four stocks offer a better risk/reward today.

And that is where the paid section begins.

For Paid Subscribers

AbbVie is the lower-upside, higher-confidence example from the screen.

But it was not the most mispriced stock my model found.

Below, I’ve included the full five-stock screen, including my fair value estimates, model upside, key risks, buy zones, and final ranking.

One of the remaining names is down more than 50% this year and still shows roughly 64% upside in my model.

Another has a pristine balance sheet, a dividend yield far above its historical average, and what I think may be the most attractive overall risk/reward setup in the screen.

But the raw upside number is not enough.

The real question is which stock has the best blend of valuation, dividend support, business quality, balance sheet strength, and realistic upside.

That is what I’ll break down below.