Markets Drop. Expected Returns Rise.

Why volatility and valuation compression are quietly improving forward returns.

U.S. equity futures are down 2–5% pre-market as geopolitical tensions escalate between the U.S. and Iran.

Oil is rising.

Volatility is spiking.

Risk appetite is shrinking.

And when markets react fast, prices often reset faster than fundamentals.

That’s where opportunity begins.

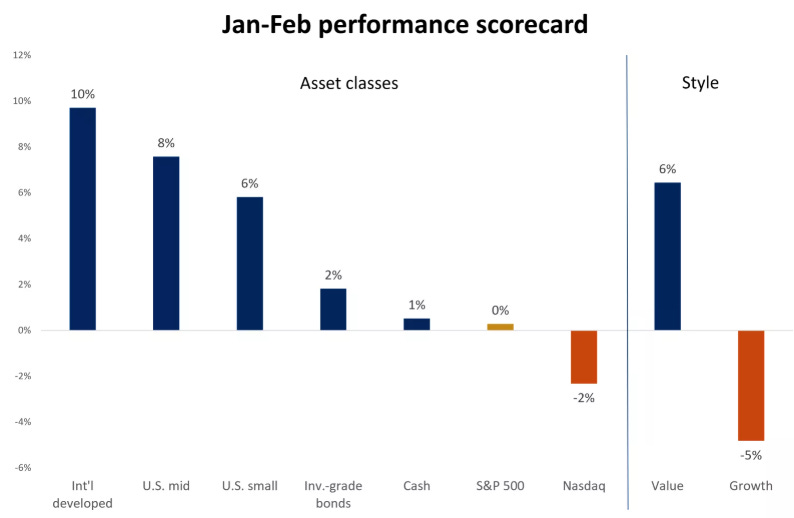

Rotation Is Already Underway

Markets are not falling evenly.

International equities have outperformed.

Value has outperformed growth.

Small caps have diverged from mega caps.

This is dispersion.

Dispersion creates mispricing.

And mispricing creates edge - if you know how to measure it.

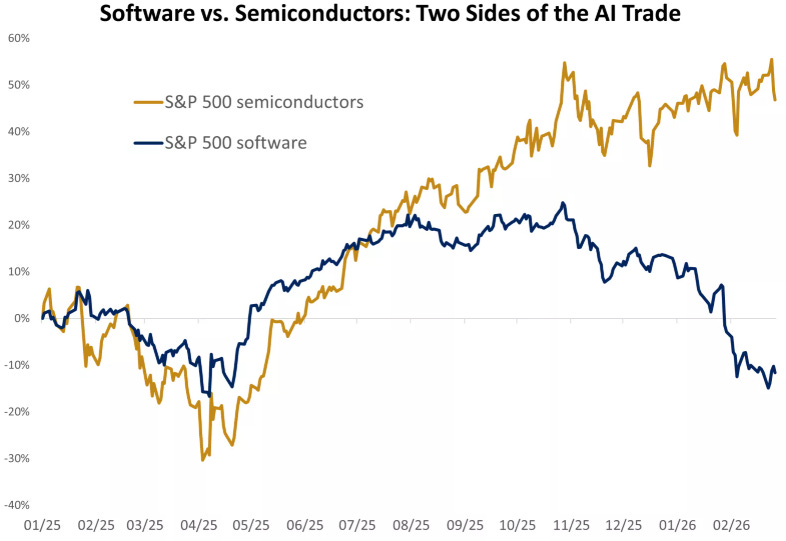

Even the AI Trade Is Splitting

Semiconductors have surged.

Software has lagged.

Same theme. Same macro narrative.

Very different price action.

That’s not collapse.

That’s capital rotating.

When leadership narrows, valuation gaps widen.

And when valuation gaps widen, forward return dispersion increases.

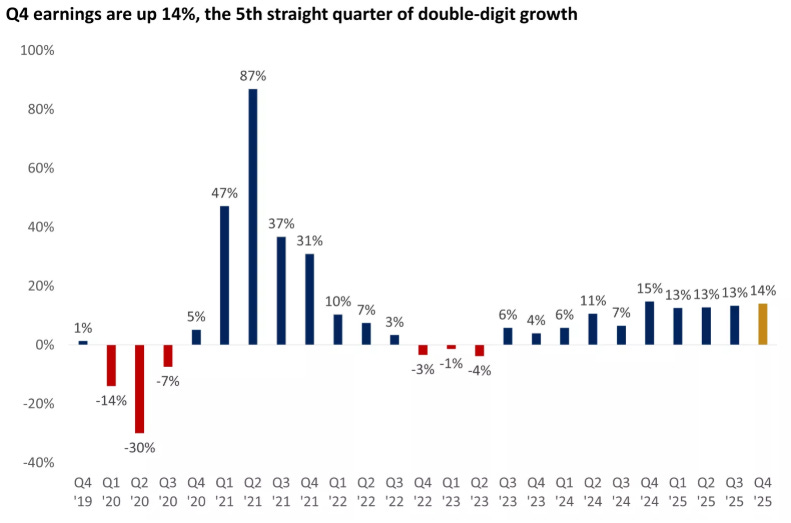

Earnings Are Not Collapsing

S&P 500 earnings are up 14%.

That’s the fifth straight quarter of double-digit growth.

This matters.

Because if earnings continue growing while multiples compress, expected returns rise mechanically.

The business doesn’t need to improve.

The price just needs to overshoot.

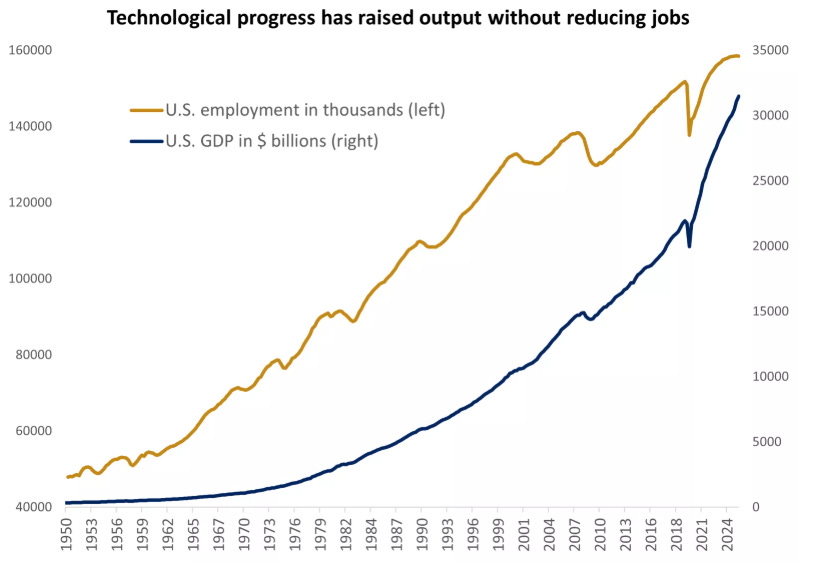

Long-Term Trend vs Short-Term Fear

Technology continues increasing productivity without destroying economic output.

Markets react emotionally in the short term.

But structural growth does not disappear overnight because of geopolitical escalation.

The question is not:

“Is today volatile?”

The question is:

“Has the long-term earning power materially changed?”

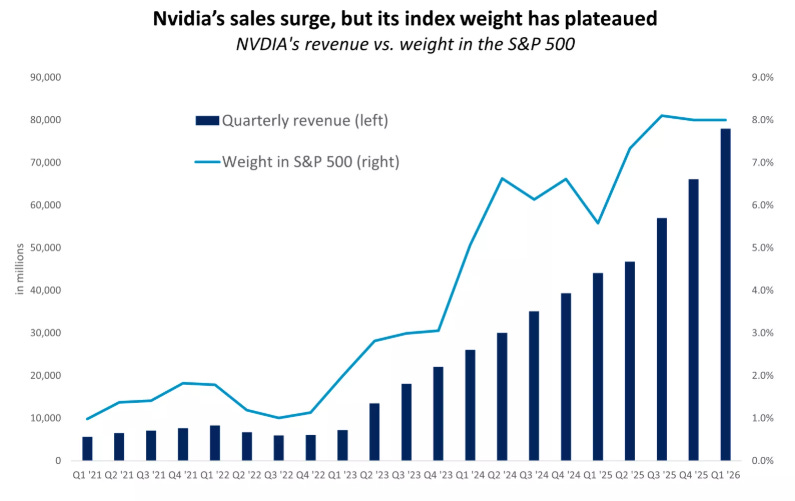

Concentration Risk Is Plateauing

Revenue growth can continue even while index weight stabilises.

Narratives cool.

Multiples compress.

Expectations normalise.

That does not equal collapse.

It equals repricing.

And repricing improves entry points.

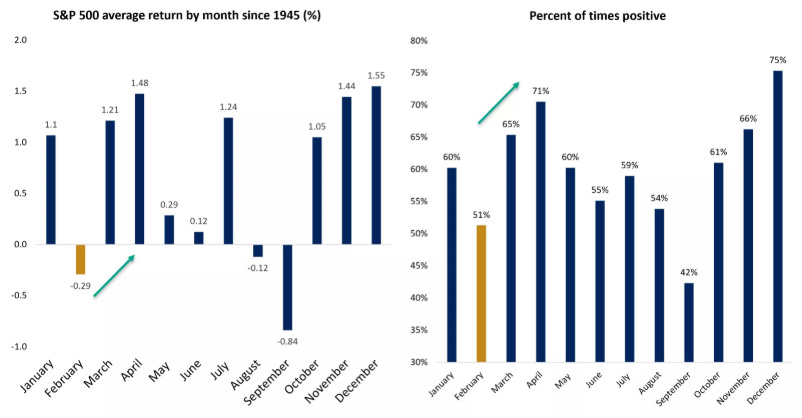

Seasonality & Probability

Short-term volatility is common.

Permanent impairment in high-quality cash-flow-generating businesses is rare.

The distinction matters.

Where This Becomes Actionable

Over the weekend, I ran the March capital allocation framework across 20 elite compounders.

Several now show materially higher 12-month expected returns than they did just weeks ago - not because fundamentals improved, but because valuations compressed.

In multiple cases, fair value gaps now sit in the 30–60% range.

That does not mean immediate upside.

It means the math has shifted.

🔒 Want The Full Ranked Allocation Framework?

Paid members received the March allocation sheet yesterday - including 12-month expected return, bear case modelling, composite allocation ranking, and conviction tiers.

If you want structured exposure instead of reacting to headlines, upgrade below.

The Psychological Edge

When markets are euphoric, buying feels easy - but expected returns are lower.

When markets are uncomfortable, buying feels difficult - but expected returns often improve.

Today feels uncomfortable.

Futures are red.

Oil is volatile.

Headlines are escalating.

But valuation compression in quality businesses rarely persists indefinitely.

Multiples stabilise.

Cash flow compounds.

Sentiment eventually follows price.

Final Thought

The market doesn’t announce when odds improve.

It improves them quietly - during repricing.

Volatility is noise.

Valuation compression is signal.

The difference between reacting emotionally and allocating rationally is structure.

That’s what this month’s ranked allocation framework is built to capture - before sentiment catches up.

- Dividend Talks