Stocks Just Rallied 10%. Now Comes the Hard Part

Earnings are carrying the market, but oil, inflation and a cautious Fed mean investors need to be far more selective after April’s rebound.

The market just delivered one of those rallies that makes investors uncomfortable.

Not because stocks went up.

But because they went up while the macro backdrop still looked messy.

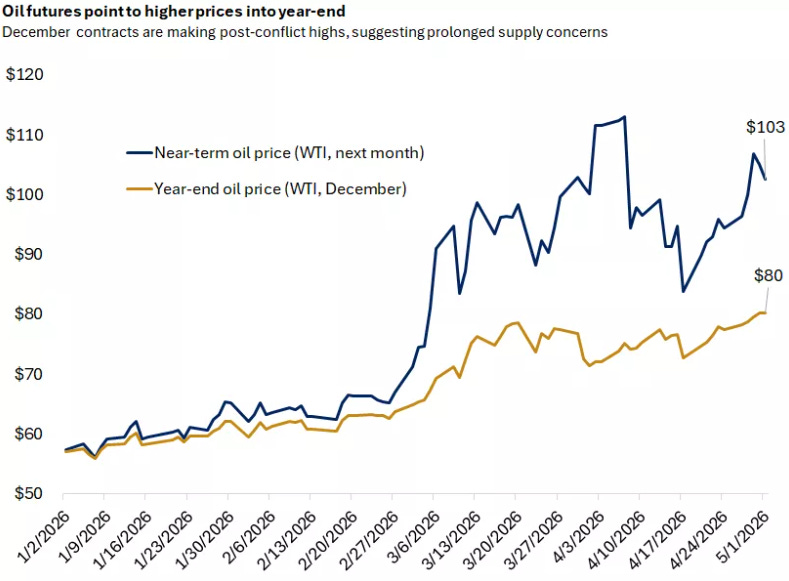

Oil prices moved higher.

The Federal Reserve sounded more cautious.

Treasury yields rose.

War uncertainty remained in the background.

Europe’s economic sentiment weakened.

The UK consumer looked under pressure.

Japan dealt with currency volatility.

And central banks around the world continued to wrestle with the same problem:

Inflation is not fully defeated, but growth is not strong enough to ignore the risks either.

And yet the S&P 500 just staged a sharp V-shaped recovery, rising more than 10% in April.

That was its strongest monthly performance since 2020.

So the obvious question is simple:

Why is the market rallying when the macro backdrop still looks so uncomfortable?

I think the answer is equally simple.

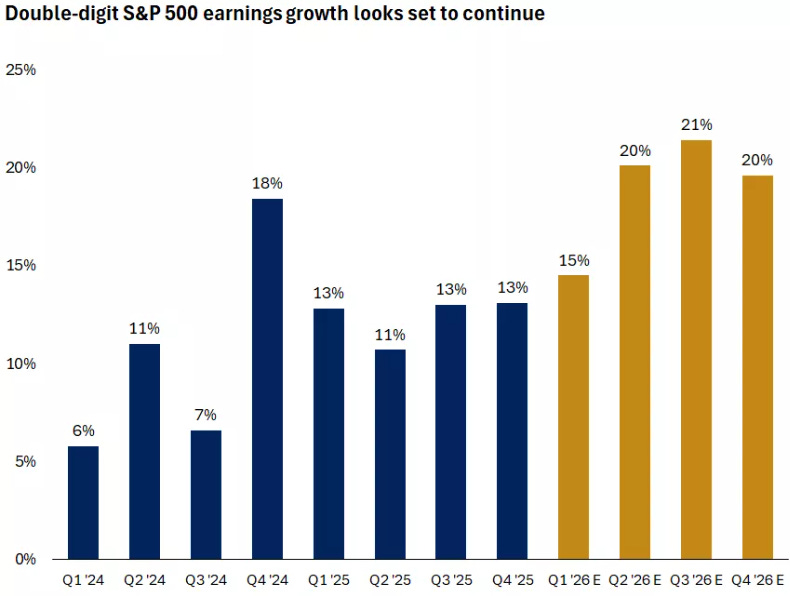

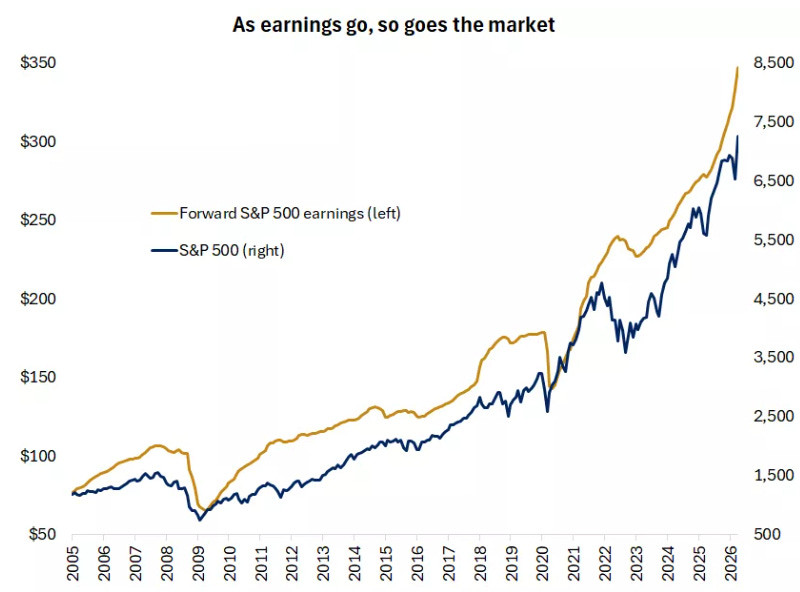

Earnings are doing the heavy lifting.

That does not mean the risks have disappeared.

It does not mean oil, inflation, interest rates, or geopolitics no longer matter.

And it definitely does not mean every stock is attractive again after the rebound.

But it does mean something important.

The market is not necessarily being irrational.

It is responding to the fact that corporate profits are still stronger than many investors expected.

The rally makes sense.

But after a 10% move higher, the next phase becomes much harder.

The Rally Was Not Built on Perfect Macro Conditions

One mistake investors often make is assuming that a rising market means the world has suddenly become safer.

That is not what is happening here.

The macro backdrop is still full of contradictions.

Oil prices are being pulled higher by geopolitical risk and supply concerns.

That matters because higher energy prices can feed into inflation, pressure consumers, raise costs for companies, and make central banks more cautious.

The Fed is also not giving the market a clean green light.

For much of the past year, investors have wanted a simple story:

Inflation falls.

The economy holds up.

The Fed cuts rates.

Earnings rise.

Stocks go higher.

That is the perfect soft-landing script.

But the current environment is not that clean.

Inflation is still sticky.

Energy prices are uncertain.

The labour market has not weakened enough to force aggressive easing.

And policymakers do not sound desperate to cut rates just because equity investors want them to.

That matters because higher rates affect almost everything.

They affect valuation multiples.

They affect borrowing costs.

They affect corporate refinancing.

They affect housing.

They affect consumer credit.

They affect the relative appeal of stocks versus bonds.

So this is not a rally built on perfect macro conditions.

It is a rally happening despite imperfect macro conditions.

That distinction matters.

Because if the macro is not doing the heavy lifting, then something else has to be.

Right now, that something is earnings.

Earnings Are Winning the Tug of War

The market is currently being pulled in two different directions.

On one side, you have macro pressure:

Higher oil.

Sticky inflation.

A cautious Fed.

Geopolitical uncertainty.

Rising yields.

Uneven global growth.

On the other side, you have corporate fundamentals:

Better earnings.

Strong margins.

Resilient consumers.

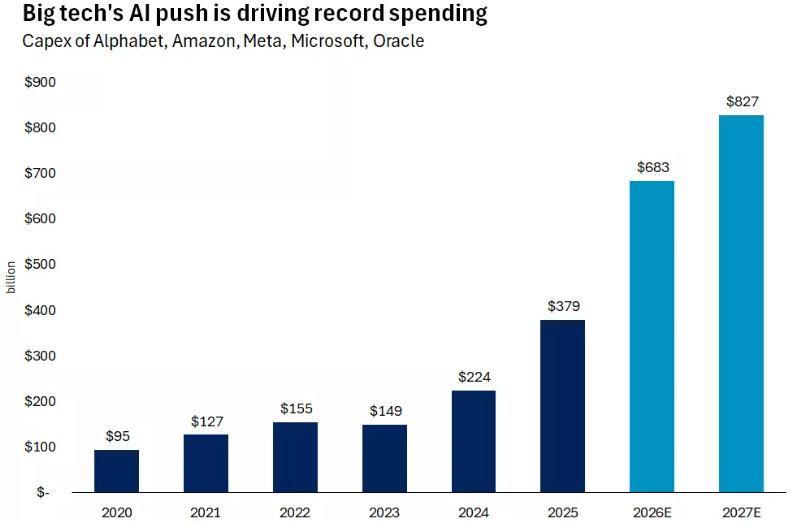

Continued AI investment.

Healthy business spending.

Large companies still clearing expectations.

And for now, earnings are winning.

That is the key.

Investors may worry about oil.

They may worry about the Fed.

They may worry about geopolitics.

But if companies are still growing revenue, protecting margins, generating cash, and guiding reasonably well, the market has something to anchor itself to.

That is what we are seeing right now.

The economy is not perfect.

But it is not cracking either.

The consumer is slowing in places, but has not collapsed.

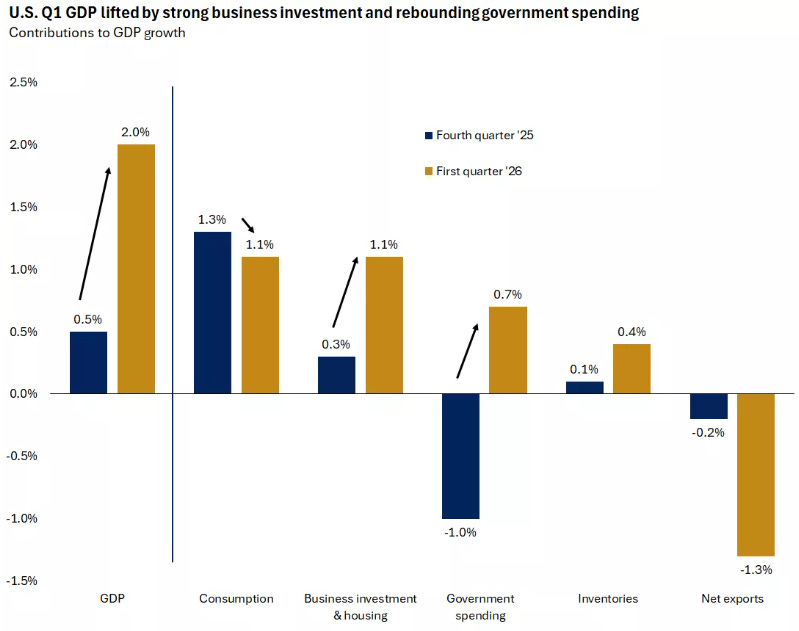

Business investment remains strong, especially in areas tied to artificial intelligence, cloud infrastructure, semiconductors, software, and data centres.

And many companies are still managing through a difficult environment better than feared.

That is why stocks have been able to climb through the noise.

Not because the noise does not matter.

But because earnings matter more.

At least for now.

AI Is Still the Engine — But the Market Is Becoming More Selective

The most important theme from this earnings season is not simply that AI remains powerful.

It is that investors are starting to become more selective about AI spending.

That is a very important shift.

For a while, the market was willing to reward almost anything connected to AI.

If a company mentioned AI, the stock could move.

If management increased AI investment, investors often treated it as a sign of ambition.

If a company built more infrastructure, the market assumed future growth would eventually justify it.

But we are now moving into a different phase.

The market is no longer asking:

“Are you spending on AI?”

It is asking:

“What return are you getting on that spending?”

That is the real change.

This is why the contrast between some of the major technology companies has been so important.

Investors rewarded companies where AI and cloud investment appeared to be translating into stronger demand, better positioning, and clearer business momentum.

But they punished companies where spending increased faster than visibility around monetisation.

That does not mean the punished businesses are suddenly broken.

Some of them remain among the highest-quality companies in the world.

But the market is sending a message:

AI spending is no longer automatically good enough.

Investors want evidence.

They want revenue.

They want margin leverage.

They want cash flow.

They want to know whether the capital being deployed today will create attractive returns tomorrow.

That is healthy.

Because the truth is simple:

AI capex will create enormous value for some companies and destroy value for others.

The winners will be the companies that turn investment into durable revenue growth, productivity advantages, margin expansion, or stronger competitive positions.

The losers will be the companies that spend aggressively because they feel forced to, but never earn enough on that spending to justify the capital deployed.

That distinction is going to matter more and more.

And I think it will be one of the defining investment themes of the next few years.

The Consumer Has Not Broken

Another reason the market has held up is that the consumer still looks more resilient than many expected.

This does not mean everything is perfect.

It does not mean lower-income consumers are not under pressure.

It does not mean higher energy prices will not eventually bite.

It does not mean discretionary spending is immune.

But there is a big difference between a consumer that is slowing and a consumer that is breaking.

Right now, the evidence still looks closer to slowing than breaking.

That distinction matters.

A slowing consumer can create valuation resets.

A broken consumer creates earnings resets.

And earnings resets are much more dangerous.

When the consumer slows, high-quality companies can still manage through the environment.

They can cut costs.

They can protect margins.

They can lean on pricing power.

They can keep investing.

They can continue compounding.

But if demand truly breaks, the entire earnings outlook changes.

So far, that is not what the market is seeing.

This is why investors have been willing to look through some of the macro noise.

The consumer is not perfect.

But the consumer is still alive.

And as long as that remains true, earnings have support.

The Fed Is Still the Main Risk

The bullish argument becomes more complicated when you look at interest rates.

Because while earnings are strong, the Fed is not providing the market with an easy path.

Markets love falling rates.

Lower rates usually support valuation multiples.

They reduce borrowing costs.

They make future cash flows more valuable.

They reduce pressure on consumers.

They make stocks look more attractive relative to bonds.

But the Fed is still dealing with inflation that is not fully back to target.

And higher oil prices make that job harder.

This is why the current setup is more fragile than it looks.

The market can handle higher rates when earnings are accelerating.

But it cannot easily handle the combination of:

Higher rates.

Higher oil.

Sticky inflation.

And earnings disappointment.

That is the risk.

Right now, earnings are strong enough to carry the market.

But if that changes, the macro risks investors are currently ignoring could suddenly become much harder to ignore.

That is why I do not think this is a market for blind optimism.

But I also do not think it is a market for blind pessimism.

The right approach is more balanced.

Constructive, but selective.

Optimistic, but valuation-aware.

Willing to buy quality, but not willing to chase everything.

The Global Picture Is Uneven

The US remains the centre of the earnings story, but the global picture is far less clean.

Europe is not collapsing, but sentiment has clearly weakened.

The region is still dealing with the pressure of higher energy prices, sluggish confidence, and central banks that cannot ignore inflation risk.

The UK has its own problems.

Rates remain restrictive.

Inflation is still above target.

And consumer-facing data continues to look weak.

That does not mean every UK stock is unattractive.

In fact, weaker sentiment can sometimes create opportunity.

But it does mean investors need to be careful about assuming the global recovery is broad and smooth.

Japan is facing a different problem.

The yen has been volatile, inflation expectations have moved higher, and the Bank of Japan is under pressure to continue normalising policy.

That creates a difficult environment because a weaker currency can support exporters, but sudden currency moves and higher rates can create volatility quickly.

China looks more mixed.

There are signs of strength in manufacturing, industrial profits, high-tech sectors, and areas tied to advanced production.

But the recovery is still uneven.

Domestic demand remains a question.

Policy support remains targeted.

And investors remain cautious.

So globally, the picture is not terrible.

But it is not clean either.

That is important.

Because when the global macro picture is uneven, the strongest opportunities tend to become more stock-specific.

This is not the type of environment where everything rises equally forever.

It is the type of environment where quality, valuation, balance sheet strength, and earnings durability matter more.

This Is No Longer a Simple Buy-the-Dip Market

A few weeks ago, the opportunity was clearer.

Sentiment was weaker.

Prices were lower.

Fear was higher.

Valuations had reset in several areas.

And investors were being paid more obviously to take risk.

But after a 10% rebound, the setup has changed.

The index has recovered a lot of ground.

Many obvious dips have already been bought.

Some stocks have moved quickly.

And expectations are no longer as low as they were.

That does not mean there are no opportunities.

There are always opportunities somewhere.

But the opportunity is no longer as simple as:

“Stocks fell, therefore buy.”

Now the questions need to be more precise.

Which companies still have earnings power the market is underestimating?

Which companies have durable cash flows that are not fully reflected in the valuation?

Which companies sold off because of temporary fear, not permanent damage?

Which companies are spending heavily but can actually generate strong returns on that spending?

Which companies can protect margins if inflation remains sticky?

Which companies can keep compounding even if rates stay higher for longer?

Those are the questions that matter now.

Because after a sharp rebound, valuation discipline matters more, not less.

The Biggest Mistake Investors Could Make Now

I think there are two obvious mistakes investors could make here.

The first mistake is becoming too bearish simply because the macro backdrop looks messy.

That sounds logical.

But it ignores the fact that earnings are still strong.

Markets do not need perfect conditions to rise.

They need conditions to be better than expected.

And right now, corporate profits are giving investors enough reason to stay constructive.

The second mistake is becoming too bullish simply because the market has rallied.

That is just as dangerous.

A rising market can make every stock look attractive.

It can make investors forget about valuation.

It can make weak companies look strong.

It can make temporary rebounds feel like permanent recoveries.

It can make people chase stocks after the risk/reward has already become less attractive.

That is why I think the correct stance today is not extreme bearishness or blind bullishness.

It is selective optimism.

Stay constructive where earnings support the valuation.

Stay disciplined where the market has already priced in too much good news.

And avoid companies where the narrative is running ahead of the numbers.

What This Market Is Really Telling Us

The message from the market is not:

“Everything is fine.”

And it is not:

“Everything is broken.”

The message is more nuanced than that.

Earnings are still strong enough to support equities.

AI investment remains a major growth engine.

The consumer has not collapsed.

Large companies are still clearing expectations.

And business investment is still supporting parts of the economy.

But the macro is getting messier.

Oil is higher.

Rates are not falling quickly.

Inflation is sticky.

Global growth is uneven.

Central banks are cautious.

And after a 10% rally, the market has less room for disappointment.

That is the real setup.

The rally makes sense.

But the easy money may already have been made.

From here, selectivity matters.

The Bottom Line

I do not think this is a market to be blindly bearish on.

The earnings backdrop is too strong for that.

But I also do not think this is a market where everything deserves to be chased.

The best opportunities are likely to be in companies where the market is still underestimating earnings durability, cash flow strength, balance sheet quality, or long-term return potential.

Not every stock that fell is attractive.

Not every valuation reset is an opportunity.

And not every company spending on AI will create value.

But this is exactly why the current market is interesting.

The index has bounced.

The headlines are noisy.

The macro is messy.

And underneath the surface, individual stocks are being repriced very differently.

That is where the work begins.

The market is no longer handing investors easy answers.

It is handing them contradictions.

Strong businesses with weak charts.

Good companies with compressed multiples.

Quality names with uncomfortable narratives.

Real risks mixed with emotional overreactions.

That is where stock picking becomes valuable.

And that is why, even after this rally, I still think there are opportunities for investors willing to be disciplined.

Not by chasing the broad market.

But by finding the companies where the fundamentals still look stronger than the sentiment.

Want the Stock List Behind This?

On Friday, I published my full May paid screen:

The Market Is Punishing the Wrong Stocks — I Found 10 That Stand Out

The market has a habit of doing this.

For that article, I screened 182 companies.

95 qualified under the valuation and quality framework.

And from there, I ranked the 10 highest-conviction opportunities based on:

Valuation

Business quality

Balance sheet strength

Downside risk

Dividend strength

Expected return

Capital allocation potential

The key question was simple:

Where has the market confused short-term fear with long-term damage?

That paid article includes the full ranked list, fair value estimates, expected upside, quality scores, risk scores, income scores, allocation rankings, conviction tiers, and the downloadable May spreadsheet.

If You Found This Useful

If this helped you make sense of the market this week, the best way to support the work is to share or restack this article.

It helps more investors find the newsletter, and it tells me these market breakdowns are useful alongside the paid stock research.

The current market is noisy.

But noise also creates opportunity.

The goal is to stay calm, stay selective, and keep separating temporary fear from long-term damage.