The Balance Sheet Matters More Than Valuation (Most Investors Learn This Too Late)

Why leverage, liquidity, and earnings durability matter more than valuation — and how to assess a company’s risk in under 60 seconds.

Markets reward discipline.

But most investors spend their time in the wrong place.

They focus on:

valuation multiples

growth rates

analyst price targets

All useful.

None sufficient.

Because none of them answer the one question that ultimately matters:

Can this business withstand pressure?

That answer doesn’t sit in the income statement.

It sits on the balance sheet.

And most investors only realise that when it’s too late.

By then, the damage is already done.

Why This Only Shows Up When It’s Too Late

In strong markets, balance sheets are largely ignored.

credit is cheap

liquidity is abundant

refinancing is easy

Weakness doesn’t disappear.

It just gets delayed.

But when conditions tighten, the difference between companies becomes obvious very quickly.

Not gradually.

All at once.

Two businesses can look identical on the surface:

similar growth

similar margins

similar valuation

But produce completely different outcomes.

The difference is rarely the business model.

It’s this:

One has flexibility. The other has constraints.

The 10-Second Balance Sheet Test

If I only had a few seconds to assess a company’s financial strength, I would start with one metric:

Net Debt relative to earnings power

In simple terms:

After accounting for cash, how many years of earnings would it take to repay the debt?

This is typically measured as:

Net Debt / EBITDA

How to Use It

Start with:

Total Debt – Cash = Net Debt

Then compare it to earnings.

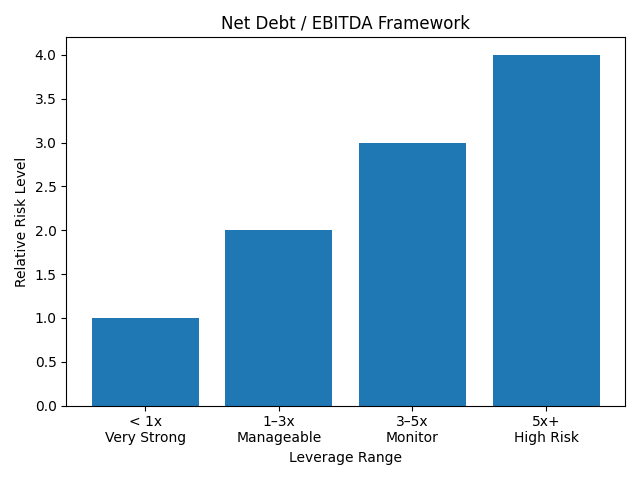

As a rough framework:

< 1x → structurally strong

1–3x → manageable

3–5x → increasingly dependent on stable execution

5x+ → vulnerable to disruption

What This Looks Like in Practice

At the lower end of the spectrum (<1x Net Debt / EBITDA), you’ll typically find businesses with:

strong free cash flow generation

high margins

and minimal reliance on external financing

Examples often include:

large-cap technology companies with net cash positions

asset-light software platforms

and certain high-quality compounders

These businesses don’t just survive downturns.

They operate from a position of strength.

They don’t need capital markets.

That’s the key difference.

But This Is Only the Starting Point

One of the biggest mistakes investors make is reducing balance sheet analysis to a single ratio.

Net Debt / EBITDA is useful.

But it doesn’t tell the full story.

A proper assessment looks at three things:

1. Liquidity (Short-Term Survival)

Before anything else, ask:

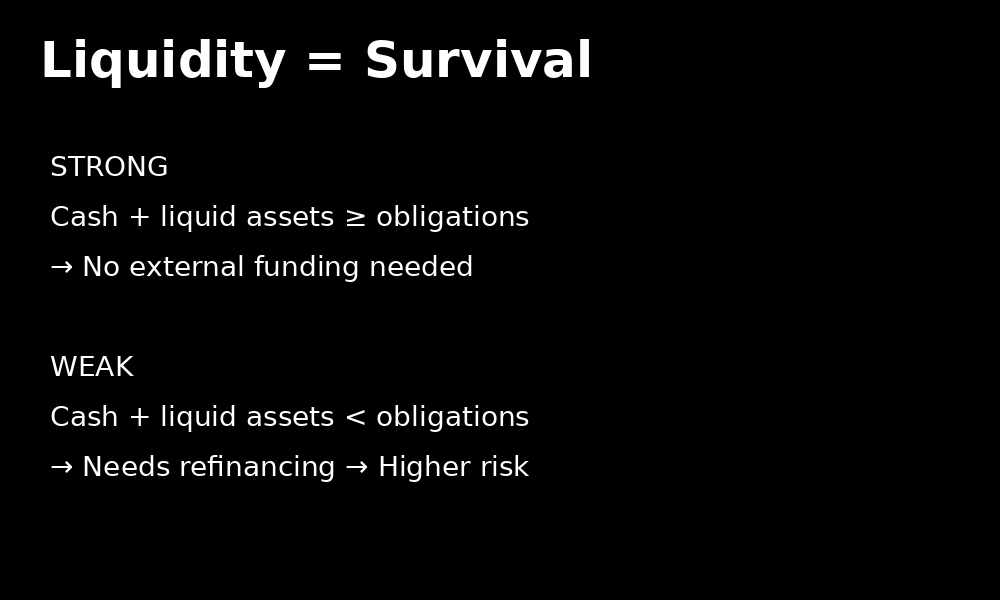

Can this business meet its obligations over the next 12–24 months?

Simple framework: liquidity determines whether a company can survive short-term stress.

This is where most problems start.

Look at:

cash

short-term assets

vs short-term liabilities

A company can be “cheap” and still run into trouble if liquidity is weak.

Because:

refinancing may be required

capital may need to be raised

or assets may need to be sold

Simple signal:

Strong liquidity → flexibility

Weak liquidity → dependence

And dependence is risk.

2. Debt Structure (When does the risk actually show up?)

Not all debt is equal.

What matters is:

When it needs to be repaid.

Two companies with identical leverage can have very different risk profiles.

One might have:

long-dated debt

fixed rates

minimal near-term refinancing

The other might have:

near-term maturities

floating-rate exposure

refinancing risk

💡 Key insight:

Most investors don’t get into trouble because a company has debt.

They get into trouble because that debt becomes relevant at the wrong time.

3. Cash Flow vs Earnings (Can the company actually handle it?)

EBITDA is useful.

But it isn’t cash.

What matters is:

How much real cash the business generates after everything else.

Look at:

free cash flow

capital intensity

consistency of cash generation

Because:

A company can look profitable on paper…

…but still struggle to manage its obligations in reality.

Bringing It Together

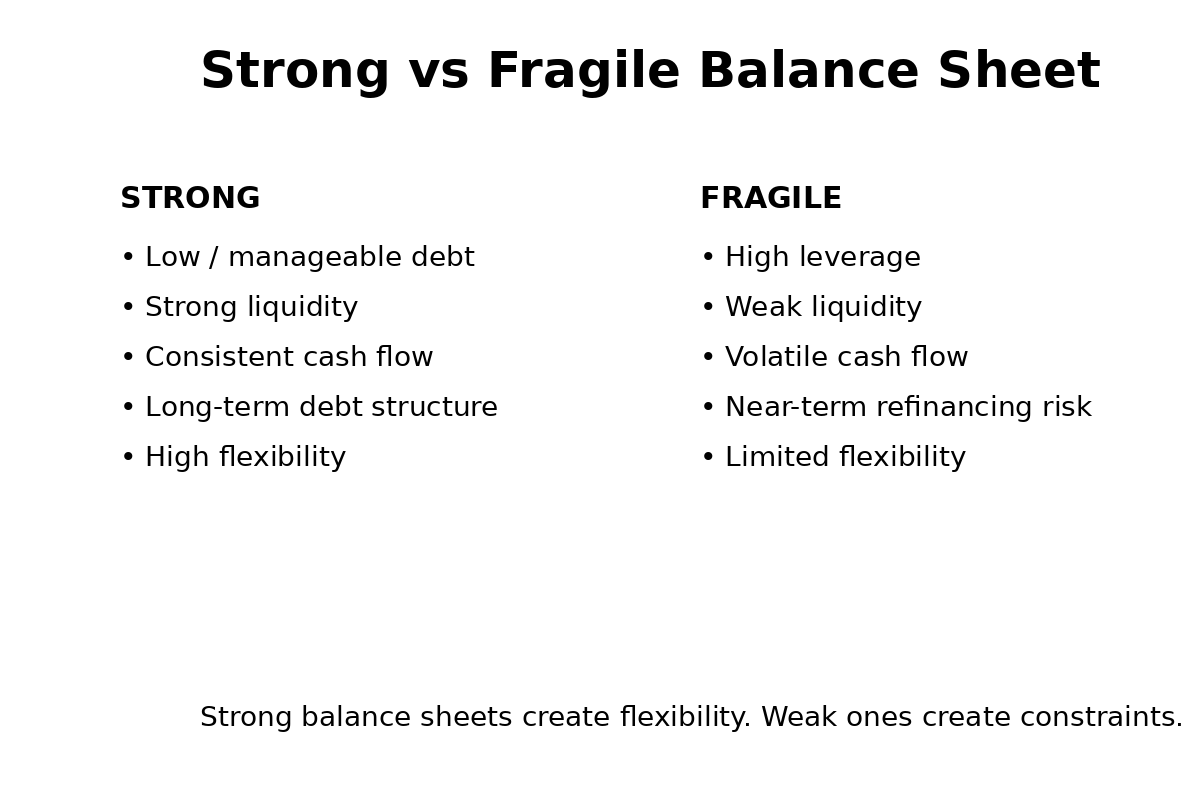

A strong balance sheet isn’t defined by one number.

It’s defined by alignment.

A strong balance sheet creates flexibility.

A weak one creates constraints.

It’s defined by alignment:

manageable leverage

strong liquidity

predictable cash flow

sensible debt structure

When all four are present:

The business has flexibility

When they aren’t:

The business becomes fragile

The Real Risk Isn’t Debt — It’s Fragility

Debt doesn’t kill businesses.

Fragility does.

Leverage simply exposes it.

When flexibility disappears:

small problems become big problems

refinancing becomes expensive

optionality disappears

That’s when you see:

dilution

dividend cuts

forced decisions

permanent repricing

A Better Way to Think About Risk

Most investors ask:

“Is this stock cheap?”

A better question — and the one that actually matters — is:

“What happens if things go slightly wrong?”

Because if the balance sheet is strong:

time is on your side

the company can adapt

valuation tends to recover

If it isn’t:

time works against you

and downside compounds

Why This Matters Right Now

Over the past few weeks, markets have repriced risk quickly.

Across multiple sectors, large-cap companies have seen meaningful pullbacks.

That creates opportunity.

But also risk.

Because:

Not all drawdowns are mispricings.

Some are opportunities.

Others are early warnings.

The balance sheet is often what separates the two.

How I Apply This in Practice

This is exactly why, in my monthly screens, I don’t just look for upside.

Every company in my screen passes this balance sheet framework before valuation is even considered.

I filter for companies where:

valuation is attractive

earnings are durable

and the balance sheet provides flexibility

Because:

Upside without durability isn’t opportunity. It’s leverage disguised as value.

What This Looks Like in the Current Market

In my latest report:

119 companies were screened

30 qualified based on strict criteria

A smaller group met my execution threshold

From those, five stand out most clearly.

Not just because of upside.

But because:

downside is defined

balance sheets are resilient

and risk/reward is asymmetric

Unlock the Full Breakdown

🔒 Paid members get access to:

The Top 5 ranked stocks this month

Exact buy ranges

Downside modelling

The full 30-stock screening dataset

Allocation framework

If you’re allocating real capital:

Entry price and downside matter just as much as upside.

Final Thought

Most investors focus on what can go right.

The balance sheet tells you what can go wrong.

And over time:

Avoiding permanent losses matters more than capturing every opportunity.

Markets reward discipline.

Not optimism. Not narratives. Not hope.

👉 If you found this valuable, consider sharing or upgrading to access the full monthly reports.

The distinction between debt as a number and debt structure as a risk factor is the part that often gets missed. Two companies with the same leverage can have very different outcomes depending on when it matures and how it's priced.