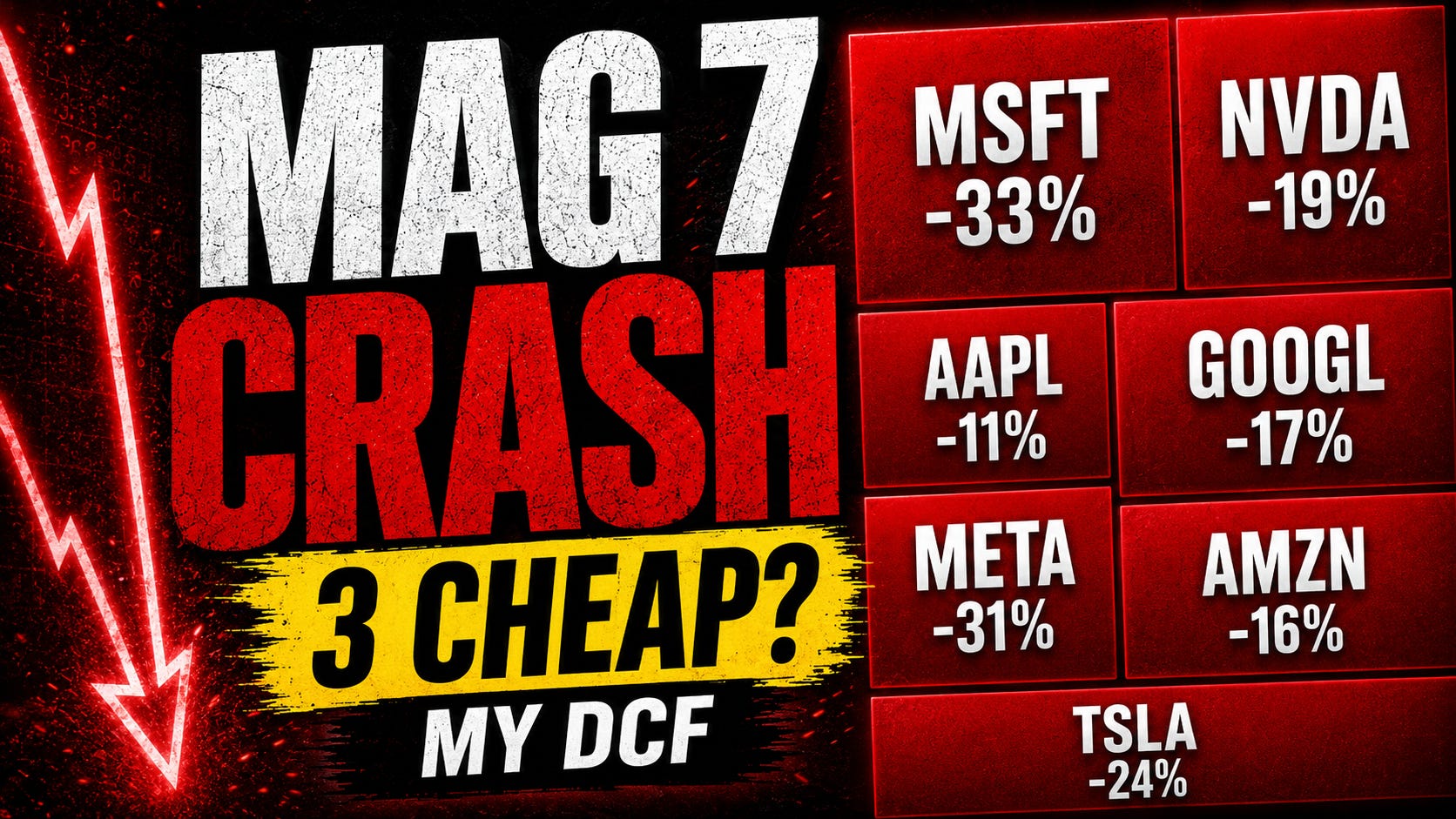

The Magnificent 7 Are Crashing — 3 Now Look Dirt Cheap in My DCF

Some Magnificent 7 stocks are now down nearly 40%, so I rebuilt every DCF model from scratch. Three look deeply undervalued, one is attractive but riskier, and three still lack enough margin of safety

Most investors don’t lose money by picking bad companies, they lose it by overpaying for great ones.

That is why I built a valuation system to answer one question every week:

👉 What’s actually worth buying now, and what only looks attractive?

Paid members get the same tools I use to size risk, find upside, and avoid value traps.

Each month, members receive:

📊 Undervalued Dividend Dashboard - A live spreadsheet ranking income stocks by valuation, yield safety, and margin of safety.

🚀 High-Upside S&P 500 Valuations - Market leaders scored by upside, downside risk, and exact buy zones.

🧠 Weekly Buy / Hold / Avoid analysis - Clear decisions, not just commentary, tied directly to articles like this one.

Free readers get the story.

Paid readers get the numbers, the risk, and the decision.

Over 150,000 investors follow my work across YouTube and Substack, using these models to manage real portfolios, not paper ideas.

Introduction

The Magnificent 7 setup is finally getting interesting.

Apple, Microsoft, Nvidia, Amazon, Alphabet, Meta and Tesla are some of the most powerful businesses on earth, but at the wrong price, even a world-class company can become a poor investment.

And after the latest sell-off, the question has changed.

It is no longer: are these great companies?

Most of them clearly are.

The real question is: are any of them finally cheap enough to buy?

Some Magnificent 7 stocks are now down heavily from their highs.

Microsoft has been hit hard. Meta has pulled back sharply. Tesla has rolled over again. Nvidia, Amazon, Alphabet and Apple have all weakened too.

The headline looks scary.

But the important point is this:

This is not a broad market collapse.

It looks much more like a leadership reset.

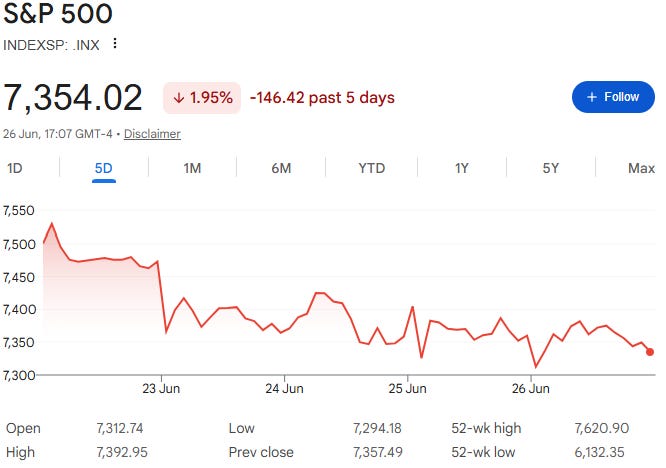

Market Update

The S&P 500 fell around 2% over the past five days, but the real pain has been concentrated in the same group of stocks that carried the market for most of the last two years: mega-cap technology.

The broader market is wobbling, but it is not falling apart.

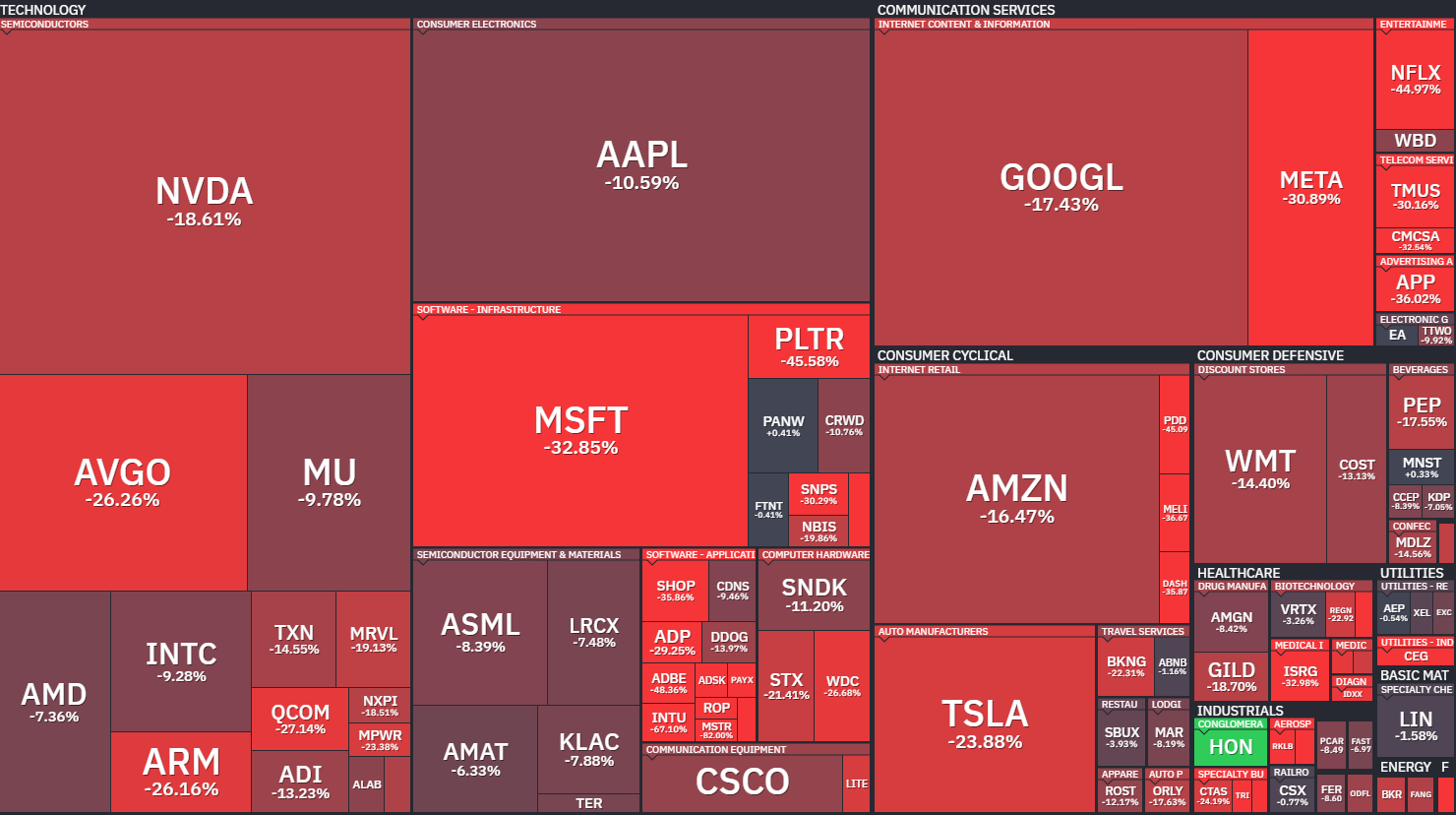

Last week’s heatmap tells the story clearly.

Last Week’s Winners & Losers

Before getting into the Mag 7 specifically, here is what leadership looked like last week.

Top performers:

AbbVie (+17%)

Merck & Co (+13%)

Johnson & Johnson (+12%)

Danaher (+11%)

Thermo Fisher (+10%)

Biggest drops:

Western Digital (-21%)

Oracle (-19%)

Seagate (-16%)

Qualcomm (-16%)

Broadcom (-11%)

Technology and semiconductors were under pressure, with Nvidia, Apple, Alphabet, Amazon, Microsoft and Tesla all red.

But beneath the surface, large parts of the market held up far better.

Healthcare was strong. Financials were resilient. Industrials were mixed, but far from broken. Consumer defensives were not collapsing either.

In other words, money is not simply leaving the stock market.

It is rotating.

That distinction matters.

When everything sells off together, fear usually creates broad opportunity. But when only the most crowded part of the market starts breaking down, the question becomes more specific:

Are investors finally being offered value in the Magnificent 7, or are these stocks just correcting from overvalued levels?

Macro News

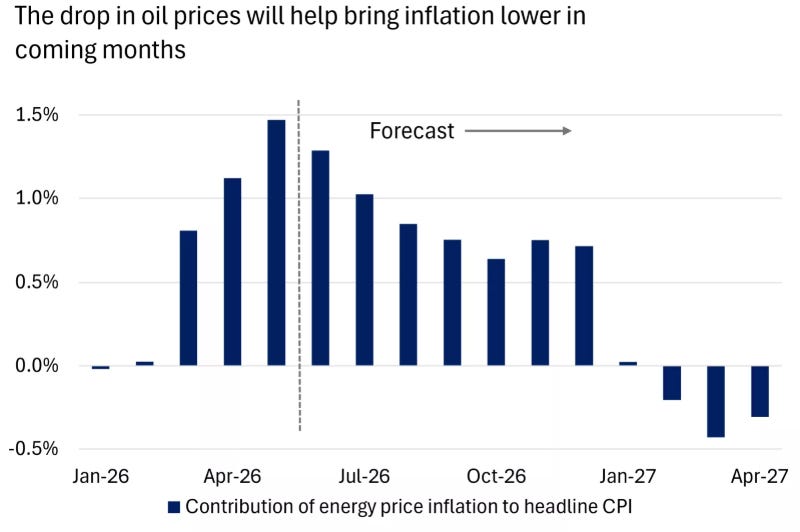

There are reasons for the rotation.

Oil prices have fallen sharply after the recent geopolitical spike began to unwind, inflation pressure from energy should ease in the coming months, and markets are already pricing in less pressure on central banks to keep hiking rates.

That matters because if inflation pressure cools, the market no longer needs to hide exclusively in the same handful of AI-linked mega-cap winners.

The broader economy also still looks more resilient than the tech sell-off suggests.

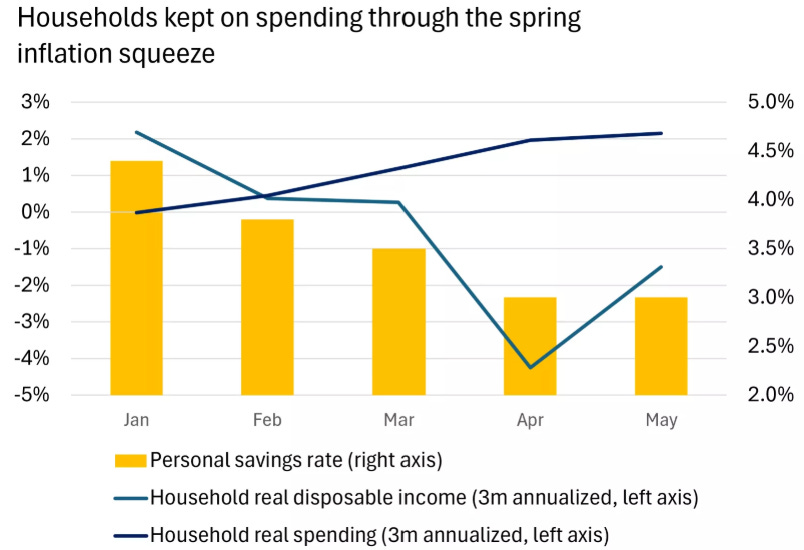

Households have continued spending, even after the spring inflation squeeze. Lower oil prices could give consumers some breathing room, help rebuild savings, and support a broader market where leadership is not dominated by the same seven stocks.

At the same time, the AI trade itself is being questioned.

Investors are starting to ask harder questions about capital expenditure, margins, competition, buybacks, and whether every dollar being poured into AI infrastructure will generate the returns currently implied by valuations.

Magnificent 7 Sell-Off

So the Mag 7 sell-off is not random.

It reflects three things happening at once:

Crowded positioning is unwinding.

The market is rotating into broader leadership.

Investors are demanding more valuation discipline from AI and mega-cap growth stocks.

And that brings us to the real question.

Lower prices alone do not automatically create value.

A stock can fall 20% and still be expensive.

A stock can fall 30% and still lack margin of safety.

And sometimes, a great business falling with the crowd can create one of the best buying opportunities in the market.

That is why I rebuilt every Magnificent 7 DCF model from scratch.

The goal was simple:

Which of these stocks are actually worth buying after the sell-off?

After updating the numbers, the answer was not “buy all seven.”

Three now look deeply undervalued in my DCF.

One looks attractive, but is more execution-dependent.

And three still lack enough margin of safety at today’s price.

Paid members get the full valuation models, fair values, buy zones, downside scenarios and final Buy / Hold / Avoid decisions behind articles like this.

Free readers get the story.

Paid readers get the numbers, the risk, and the decision.

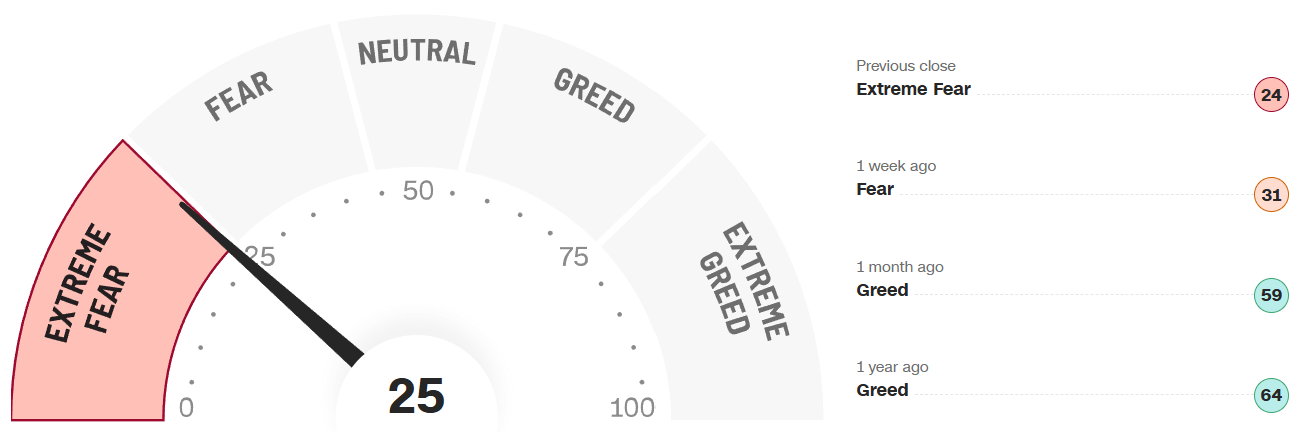

Fear & Greed Index

Sentiment has also weakened.

The Fear & Greed Index is back in fear territory, which is exactly when valuation discipline matters most.

Fear creates opportunity, but it also creates traps.

The job is not to buy everything that has fallen.

The job is to separate the real bargains from the names that still have too much optimism priced in.

This is why the current setup is so interesting.

The Mag 7 trade is cracking, but the market itself is not broken.

That creates a very different opportunity set.

If the entire market were collapsing, the answer might be simple: raise cash, manage risk, and wait for panic.

But if the weakness is concentrated in the most crowded mega-cap growth stocks, then the better question is:

Which of these companies are being unfairly punished?

That is what the DCF models are designed to answer.

Earnings Week

It is a quieter earnings week, but there are still a few names worth watching: Nike, Constellation Brands, FactSet, General Mills, MSC Industrial, Concentrix and AeroVironment.

None of these are likely to define the entire market narrative on their own, but they can still give us useful signals around consumer demand, enterprise spending, industrial activity and whether the broader economy remains as resilient as the rotation suggests.

Join 130,000+ investors on YouTube! 🎥

I also break down these market moves every week on YouTube.

If you prefer watching the analysis rather than reading it, you can subscribe to the Dividend Talks YouTube channel below 👇

Magnificent 7 DCF Models

Now the main event for this article is the Magnificent 7.

So let’s get into the models.

I ranked all seven from weakest to strongest based on valuation, margin of safety, quality, risk, and what the market appears to be pricing in today.

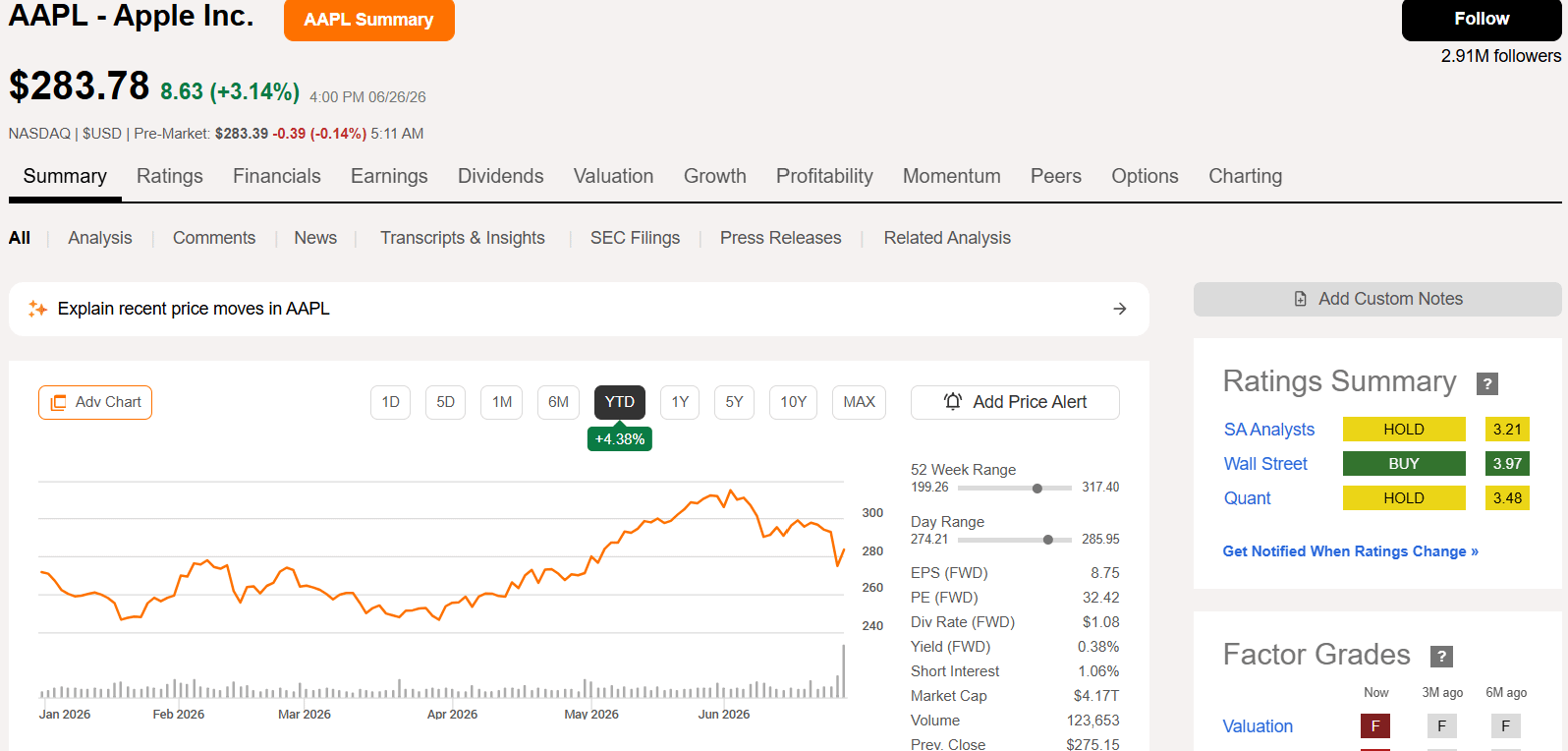

Free Model — Apple (AAPL): Great Business, Weak Margin of Safety

Valuation

Apple is still trading at a premium valuation despite the recent pullback.

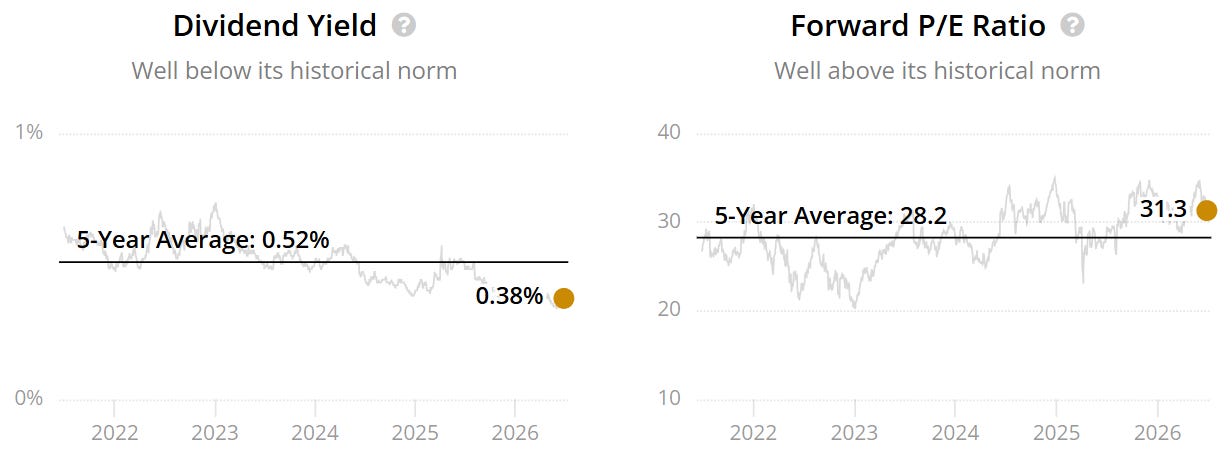

The forward P/E sits well above its historical norm at 31x vs a 5-year average of 28x.

This suggests the stock is still being priced as a premium compounder, even though recent free cash flow growth has been relatively modest.

The dividend yield also remains well below its historical norm at 0.4% vs a 5-year average of 0.5%, which supports the same conclusion: Apple is not obviously cheap on traditional valuation metrics.

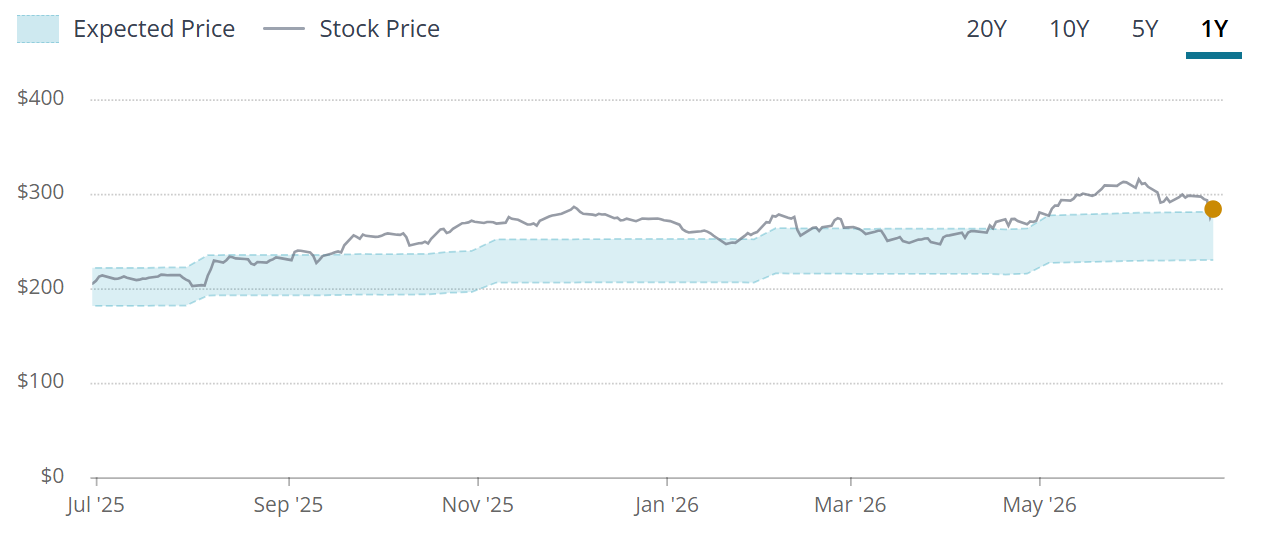

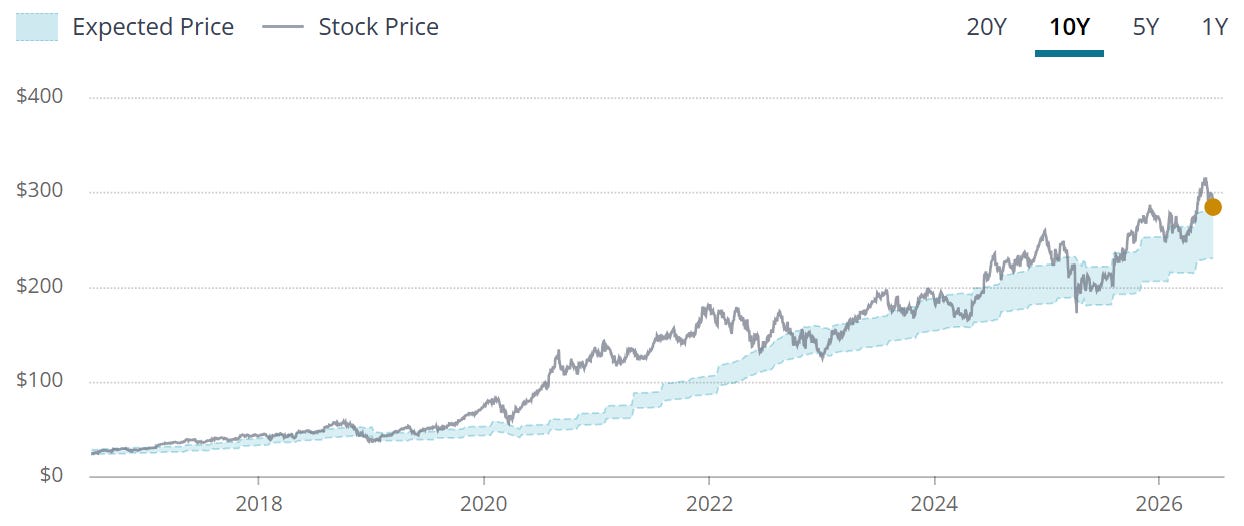

The blue tunnel also shows Apple trading around the upper end of its expected valuation range. While the stock has pulled back from recent highs, it has not fallen far enough to create a clear margin of safety in my model.

Looking at the last 10 years, Apple has rarely traded at a huge discount for long. The market consistently awards the business a premium because of its ecosystem, brand strength, services revenue and enormous buyback program.

But that premium only makes sense if future cash flow growth can justify it.

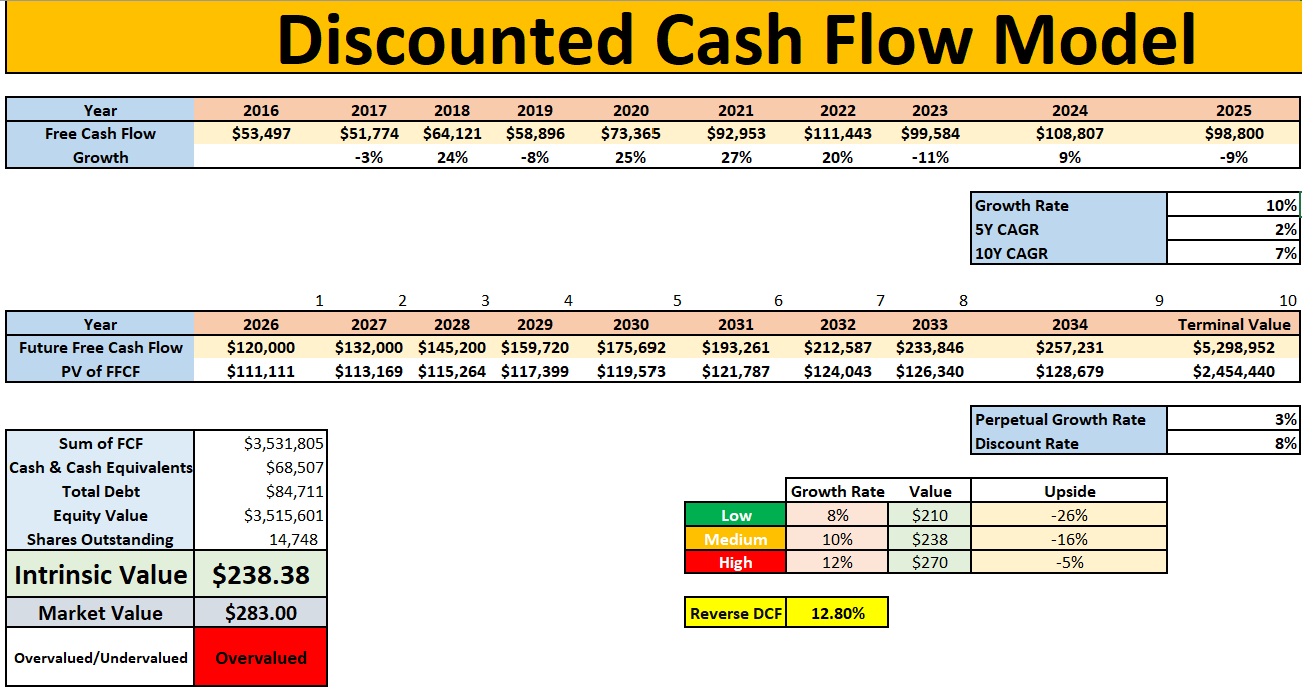

DCF Model

Using my DCF model, a few things stand out:

12.8% is currently baked into the reverse DCF for future free cash flow growth.

Apple’s 5-year free cash flow CAGR sits at 2%.

Apple’s 10-year free cash flow CAGR sits at 7%.

Using 8% as the lower growth rate gives an intrinsic value of $210.

Using 10% as the middle growth rate gives an intrinsic value of $238.

Using 12% as the higher growth rate gives an intrinsic value of $270.

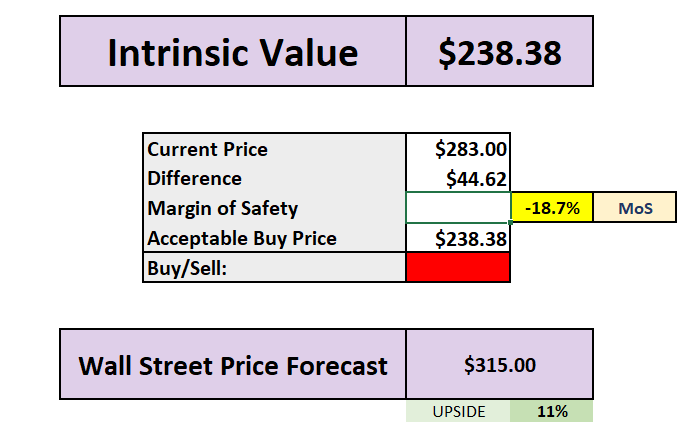

Using the middle growth rate of 10%, I get an intrinsic value of $238.

With Apple trading around $283, that means the stock still trades at roughly an 18.7% premium to my fair value estimate.

In other words, even after the pullback, Apple still does not offer enough margin of safety in my model.

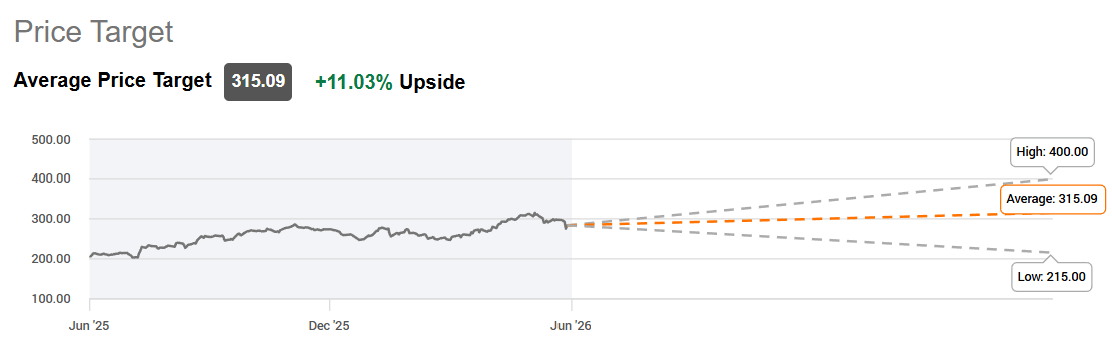

Wall Street’s average price forecast is around $315, implying roughly 11% upside, but my own DCF remains more cautious.

What the market is pricing in

The market is still pricing Apple like a premium growth compounder.

That makes sense to a point. Apple remains one of the highest-quality businesses in the world. The ecosystem is sticky, the balance sheet is strong, services revenue is valuable, and the company continues to return huge amounts of cash to shareholders through buybacks.

But the issue is not quality.

The issue is valuation.

At today’s price, Apple needs a meaningful reacceleration in free cash flow growth to justify the current multiple. That is difficult when the company’s recent free cash flow growth has been far lower than what the market appears to be pricing in.

The current setup seems to assume that services growth, buybacks and ecosystem monetisation can offset slower hardware growth for a long time.

That might happen.

But I do not think today’s price gives investors enough margin of safety if it does not.

Verdict: HOLD

Apple is a wonderful business, but it is not one of the Magnificent 7 stocks that looks deeply undervalued in my DCF.

The stock has pulled back, but not enough.

For me, Apple is a perfect example of why falling prices alone do not automatically create value.

A great company can still be a mediocre investment if the valuation already prices in too much future success.

Apple shows why a lower price alone is not enough.

Even after the pullback, my model still does not show enough margin of safety. The business is excellent, but the valuation still assumes a lot of future success.

But Apple is not where the ranking gets most interesting.

After updating all seven DCF models, three Magnificent 7 stocks now look deeply undervalued, one looks attractive but more execution-dependent, and three still fail my margin-of-safety test.

Below, paid members get the full valuation breakdown for the remaining six stocks, including my updated fair values, downside scenarios, buy zones, final Buy / Hold / Avoid decisions, and the exact order I would buy them in today.