The Market Just Triggered 3 Buy Signals in My Valuation Model

Oil shocks, weak payrolls, and rising fear rattled markets this week. I screened for mispriced companies - here are 3 stocks my model says are buys and 2 to avoid.

Markets faced something of a perfect storm this week.

Oil prices surged following escalating tensions in Iran, raising concerns about a renewed inflation shock. At the same time, a weaker-than-expected payroll report added to fears that economic growth may be starting to slow.

The combination triggered a broad risk-off move across global markets.

Equities pulled back, bond yields jumped, and investors rapidly reduced risk exposure as they attempted to assess the implications for both inflation and monetary policy.

Despite this volatility, the S&P 500 remains only a few percent below all-time highs and is still up roughly 17% over the past year.

In other words, sentiment has deteriorated quickly, but the broader market structure remains relatively resilient.

Periods like this are important for investors.

When fear rises and volatility spikes, markets often begin to create temporary valuation dislocations.

And that’s exactly what my valuation framework attempts to identify.

When volatility rises, my focus is simple: find high-quality businesses trading below intrinsic value.

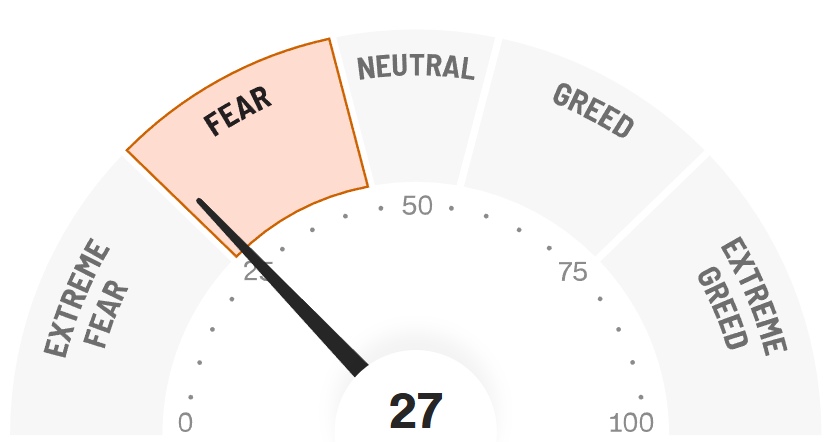

Market Sentiment Has Shifted Rapidly

Investor sentiment deteriorated sharply during the past week.

The Fear & Greed Index dropped to 27, firmly within “Fear” territory.

When sentiment indicators move into fear territory, it often signals that investors are becoming excessively cautious in the short term.

Historically, these environments have often created attractive entry points for long-term investors, particularly when strong companies are sold alongside weaker businesses during broad market pullbacks.

What Happened In Markets Last Week

The S&P 500 heatmap highlights the uneven nature of the recent selloff.

Large technology companies such as Microsoft and Broadcom held up relatively well, while weakness across healthcare, consumer staples and financials weighed on the broader market.

Several mega-cap companies - including Apple and Alphabet - also declined as investors rotated capital amid rising macro uncertainty.

This type of dispersion is important.

It suggests that investors are not indiscriminately selling everything, but instead are reallocating capital as they reassess risks tied to inflation, interest rates and geopolitical tensions.

Weak Payroll Data Added To Market Concerns

The latest payroll report surprised markets to the downside.

February payrolls declined by 92,000 jobs, significantly below expectations for a modest gain.

Revisions to previous months also revealed weaker hiring momentum than initially reported.

While one month of data should not be overinterpreted, the report raised concerns that the labour market may be cooling more quickly than previously expected.

However, the unemployment rate remains relatively low at 4.4%, suggesting the labour market is slowing but not collapsing.

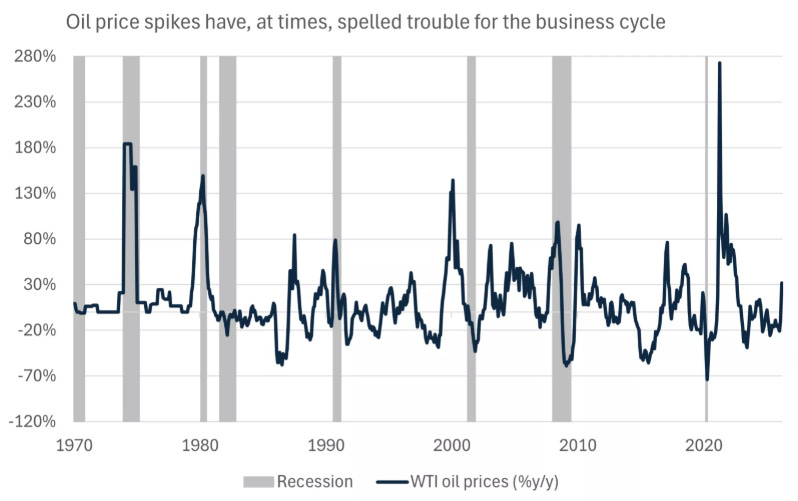

Oil Prices Are Creating A New Inflation Risk

At the same time, energy markets delivered a major shock.

Oil prices surged more than 30% following the escalation of tensions in Iran.

Historically, large energy price shocks have sometimes coincided with economic downturns.

However, the relationship between oil prices and the U.S. economy has changed significantly over the past several decades.

The United States now produces far more energy domestically and is far less dependent on imported oil than it was during the energy crises of the 1970s.

As a result, the economy today is far more resilient to energy price shocks.

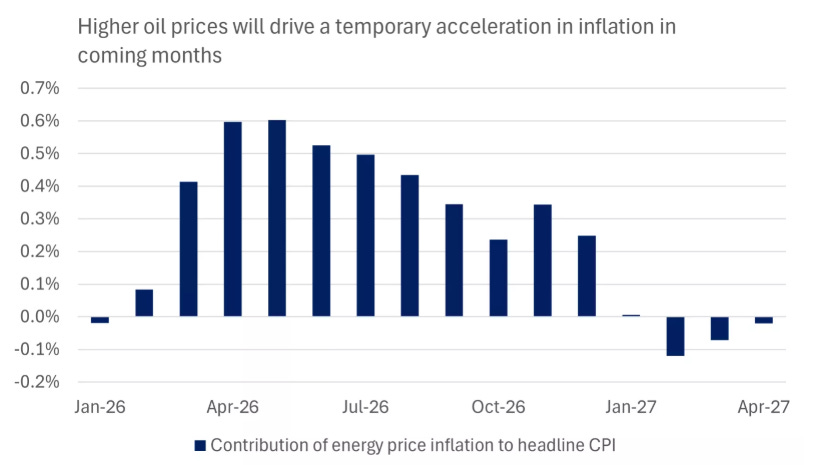

Inflation Could Temporarily Rise Again

Even so, higher oil prices are likely to feed into inflation data in the coming months.

Energy accounts for roughly 6% of the CPI basket, meaning increases in oil prices can push headline inflation higher even if underlying economic conditions remain stable.

Based on current futures pricing, the energy shock could push inflation modestly higher during 2026 before gradually fading.

This dynamic creates a dilemma for policymakers.

Normally, weak labour data would increase expectations for interest rate cuts.

However, rising energy prices may force the Federal Reserve to delay easing policy, which is one reason markets reacted negatively this week.

Upcoming Earnings This Week

Investors will also be closely watching several earnings reports in the coming days.

Companies such as Oracle and Adobe could provide additional insight into enterprise software demand and broader technology spending trends.

While this week’s earnings calendar does not include many mega-cap names, the results may still provide signals about corporate spending trends across the economy.

Why This Matters For Investors

Periods of macro uncertainty often create short-term pricing inefficiencies.

When investors reduce risk broadly, even strong businesses can sell off alongside weaker companies.

This is where disciplined valuation frameworks become valuable.

Each week I screen the market for companies that meet several key criteria:

• Durable competitive advantages

• Strong free cash flow generation

• Long-term growth drivers

• Attractive valuations relative to historical ranges

This week, three companies triggered buy signals in my valuation model.

At the same time, two widely owned stocks currently appear less attractive based on their growth outlook and valuation.

I publish research like this every week - breaking down markets and identifying stocks trading below intrinsic value.

Subscribe to access the full analysis.