This Is a Huge Week for the Stock Market

Inflation, rates, AI stocks and the SpaceX IPO are all being tested at once.

Good morning everyone,

This could be a huge week for the stock market.

Not because one single event will decide everything.

But because several major market forces are now colliding at the same time.

Inflation data is coming.

Interest rate expectations are shifting.

AI stocks just took a hit.

Fear has moved higher.

And the SpaceX IPO could become one of the biggest market events investors have ever seen.

That last point matters more than people realise.

Because SpaceX is not just another IPO.

It is a test of how much investors are still willing to pay for future growth, AI infrastructure, private-market hype, Elon Musk premium, and the idea that retail investors are finally getting access to something they were locked out of for years.

And the timing is fascinating.

Just as the market is starting to question stretched valuations, just as technology stocks are showing signs of stress, and just as interest rate expectations are moving higher, one of the most anticipated IPOs in history is being discussed at a valuation that could leave almost no room for error.

That combination matters.

Because Friday was not just another red day.

It was a warning shot.

Friday Was a Warning Shot

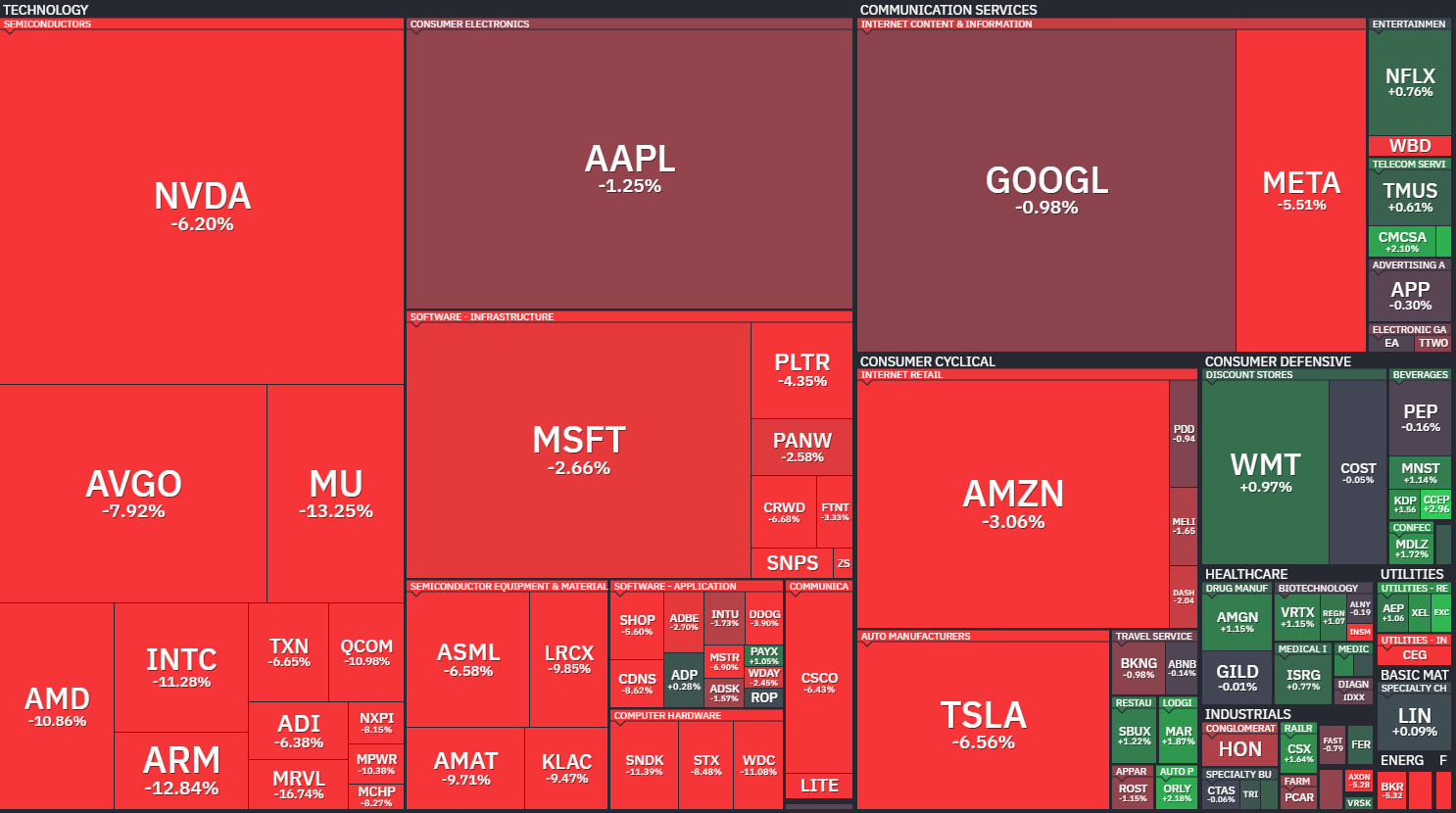

On Friday, the market looked ugly on the surface.

But the real story was even more interesting underneath.

Technology was hit hard.

Semiconductors were crushed.

Nvidia fell sharply.

Broadcom dropped even more.

AMD, Micron, Intel and several other chip-related names were deep in the red.

The Nasdaq was under real pressure.

But this was not a normal “everything is down” type of sell-off.

One of the most interesting charts from Friday showed that more than half of S&P 500 stocks were actually advancing, even though the index itself was down more than 2%.

That is unusual.

And it tells us something important.

This was not necessarily a broad market collapse.

It looked more like a concentrated unwind in the stocks that had been carrying the market higher.

In other words, the market was not selling everything.

It was selling the crowded winners.

That is a very different message.

The Market Is Starting to Question the AI Trade

For most of the past few years, the easiest trade in the market has been simple:

Buy the AI winners.

That trade has worked incredibly well.

AI-related companies have added trillions of dollars in market value since the launch of ChatGPT.

The market has rewarded companies connected to chips, cloud infrastructure, data centres, large language models, and anything tied to the next phase of artificial intelligence.

And to be clear, I am not dismissing AI.

The opportunity is real.

The investment cycle is real.

The demand for compute is real.

But the stock market does not just care whether a theme is real.

It cares how much investors are paying for that theme.

And that is where things become more complicated.

If a small group of AI-related companies has driven most of the market’s gains, then the market becomes much more sensitive to any change in expectations.

If interest rates rise, valuations matter more.

If earnings disappoint, expectations matter more.

If investors start rotating away from crowded trades, positioning matters more.

That is why Friday was important.

It showed that investors may be starting to question whether some parts of the AI trade have become too crowded, too expensive, or too dependent on perfect execution.

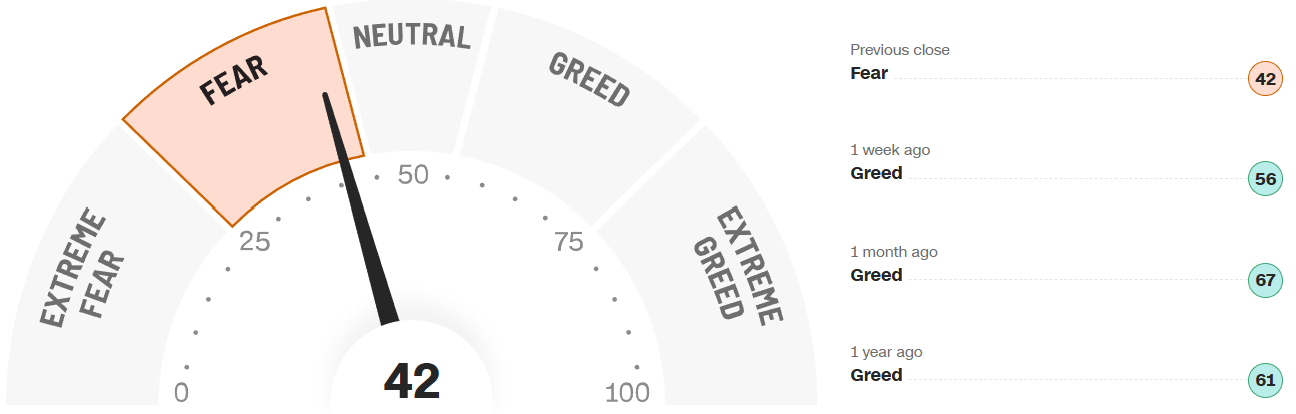

Fear Is Rising Again

The Fear & Greed Index has moved back into fear.

That does not mean the market has to crash.

It does not mean investors should panic.

But it does show that sentiment has changed quickly.

One week ago, the market was still in greed.

One month ago, it was deeper in greed.

Now, after one sharp move lower, investors are suddenly more cautious.

That is how quickly sentiment can shift when valuations are high.

And this is why I always come back to valuation discipline.

When investors are greedy, they focus on upside.

When investors are fearful, they suddenly remember risk.

The business may not have changed in 24 hours.

But the price investors are willing to pay for that business can change very quickly.

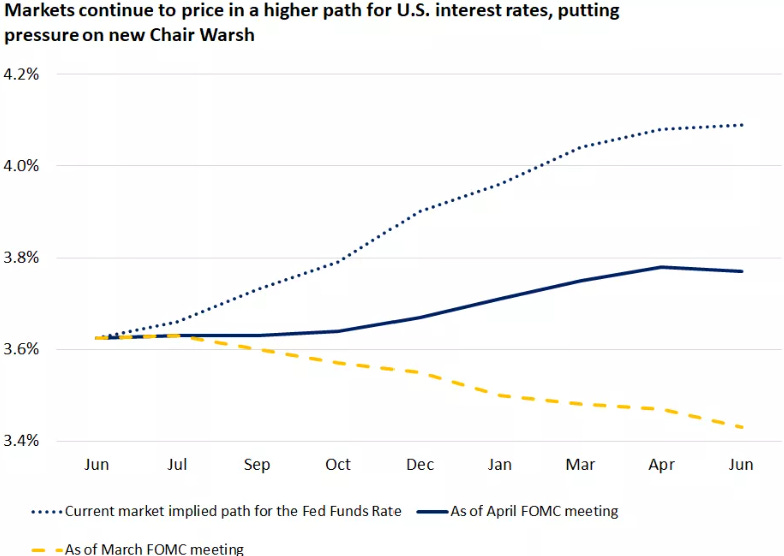

Good News Is Becoming Bad News Again

The other major issue is interest rates.

The market has spent much of the year hoping for lower rates.

But the latest economic data has made that story more difficult.

The labour market has been stronger than expected.

Hiring has improved.

The economy looks more resilient.

Normally, that should be good news.

And for the real economy, it probably is.

A stronger labour market supports consumer spending, corporate earnings, and overall growth.

But for the stock market, there is a catch.

If the economy is stronger than expected, the Federal Reserve has less pressure to cut interest rates.

And if inflation remains sticky at the same time, the market may start worrying about the opposite problem.

What if rates stay higher for longer?

What if the next move is not a cut?

What if the market has been too optimistic?

That is why this week matters so much.

Inflation data is coming.

And if inflation comes in hotter than expected, the market may have to reprice again.

Higher Rates Change the Valuation Conversation

This is the part investors cannot ignore.

Higher interest rates do not affect all stocks equally.

When rates are low, investors are usually more willing to pay higher prices for future growth.

That helps technology stocks.

It helps companies where a lot of the expected value sits far into the future.

It helps long-duration growth stories.

But when rates rise, or when markets price in higher-for-longer rates, those same valuations become harder to justify.

That does not mean great companies suddenly become bad companies.

It means the price matters more.

A great company can still be a bad investment if the starting valuation is too high.

And that brings us to one of the biggest stories in the market right now.

The SpaceX IPO Is Arriving at a Fascinating Time

SpaceX may be one of the most impressive private companies in the world.

The company has transformed the launch industry.

Starlink has built a global satellite internet business.

The long-term potential is enormous.

And if SpaceX does come public, it will likely become one of the most talked-about listings in market history.

But here is the problem.

It may be arriving at exactly the moment investors are starting to care about valuation again.

SpaceX is reportedly targeting a valuation around $1.75 trillion.

That is an extraordinary number.

At that level, investors are not just paying for a great rocket business.

They are not just paying for Starlink.

They are paying for a future where almost everything goes right.

Reusable rockets.

Satellite broadband.

Space-based infrastructure.

Potential AI compute.

Massive future cash flows.

And entirely new markets that do not yet exist at scale.

Could some of this happen?

Absolutely.

But the question investors need to ask is not whether SpaceX is an incredible company.

The better question is:

How much of that incredible future is already priced in?

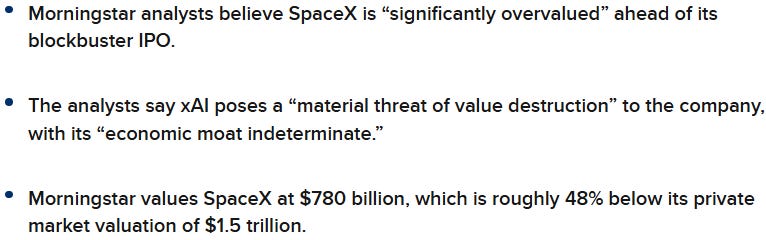

The Valuation Gap Is the Real Story

Morningstar has reportedly valued SpaceX at around $780 billion.

That is still a huge valuation.

But it is far below the valuation being discussed for the IPO.

This creates the central issue for investors.

SpaceX may be an amazing business.

But if the IPO valuation is more than double what a fundamental analyst believes the business is worth today, then the margin of safety may be very thin.

And that matters.

Because public market investors are not buying the company in its early days.

They are not buying when the valuation was $10 billion.

They are not buying when the valuation was $100 billion.

They are potentially being invited in after the story has already become enormous.

That does not automatically make it a bad investment.

But it does mean investors need to be honest about where they are entering the story.

Are retail investors getting early access to a once-in-a-generation business?

Or are they providing liquidity at a very high valuation?

That is the question.

Retail Investors Are Being Invited In

One of the most interesting parts of the SpaceX IPO is the potential retail allocation.

Usually, high-profile IPOs are dominated by institutions.

Retail investors often get access later, after the big money has already had the better entry point.

But in this case, retail investors may receive a much larger allocation than normal.

On the surface, that sounds exciting.

It sounds like access.

It sounds like democratisation.

And maybe that is part of it.

But investors should also be careful.

When retail investors are invited into a huge IPO at a very high valuation, the question is not just:

Can I get shares?

The better question is:

Should I want shares at this price?

Because IPOs are often emotional.

They are marketed with excitement.

They are surrounded by hype.

They create fear of missing out.

But long-term returns are usually not driven by hype.

They are driven by earnings, cash flow, growth, and the price paid.

Being early is not always the same as being right.

Especially if the valuation already assumes an extraordinary future.

Index Buying Could Create Forced Demand

There is also another important issue.

Index inclusion.

If SpaceX becomes a public company and is eventually added to major indexes, passive funds may be required to buy it.

That can create automatic demand.

But automatic demand is not the same as valuation-sensitive demand.

A passive fund does not buy because a stock is cheap.

It buys because the index tells it to.

That is why investors should be careful when people point to future index demand as a reason to buy.

Yes, it can support the stock in the short term.

Yes, it can create powerful flows.

Yes, it can make the IPO even more exciting.

But forced buying does not make a stock undervalued.

It just means more money may be required to buy the stock, regardless of price.

And in a market where passive capital is so large, that matters.

This Is the Bigger Lesson for Investors

The SpaceX IPO is not just a SpaceX story.

It is a market story.

It tells us where we are in the cycle.

Investors are still willing to pay enormous valuations for exciting growth stories.

Retail investors are still eager to access anything connected to Elon Musk, AI, space, and the next big technology platform.

Wall Street is still very good at turning a great story into a major market event.

But Friday’s sell-off reminds us that valuation still matters.

The market may love a story when everything is going up.

But when rates move higher, inflation becomes sticky, or investors start reducing risk, the market becomes much less forgiving.

That is why this week is so important.

It is not just about whether inflation comes in hot or cold.

It is not just about whether the Fed sounds hawkish or dovish.

It is not just about whether AI stocks bounce or keep falling.

It is about whether investors are still willing to pay premium valuations in a market where the macro backdrop is becoming more complicated.

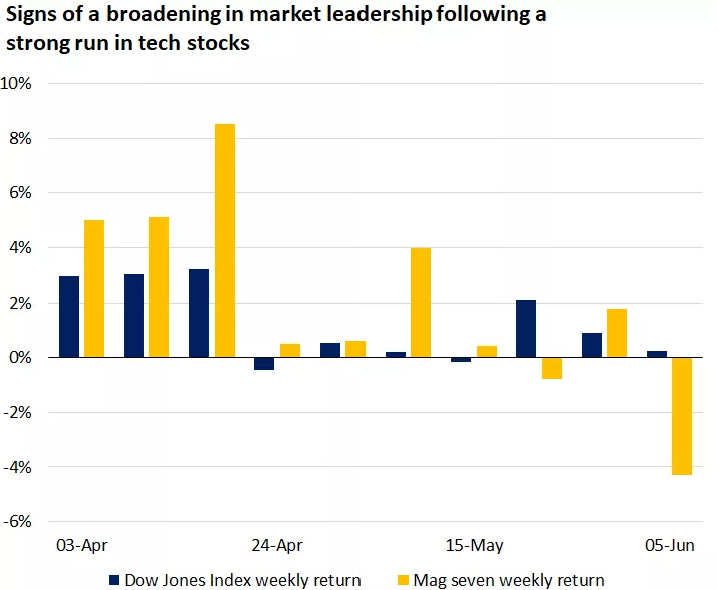

Market Leadership May Be Changing

One of the most interesting developments is the possibility that market leadership is starting to broaden.

For a long time, the market has been dominated by mega-cap technology and AI-related stocks.

But recently, there have been signs that other areas of the market are starting to participate.

That could be healthy.

A market led by only a handful of stocks can work for a while.

But it also creates concentration risk.

If those leaders start to weaken, the index can fall even if many individual stocks are holding up.

That is exactly what we saw on Friday.

So the question now becomes:

Is this just a short-term pullback in tech?

Or is it the beginning of a broader rotation?

I do not know the answer yet.

But I think investors should be paying close attention.

Because if leadership broadens, there may be opportunities outside the most crowded AI names.

Dividend stocks.

Defensive compounders.

Financials.

Healthcare.

Consumer staples.

Industrial businesses.

And high-quality companies that have been ignored while investors chased the hottest technology names.

This Week Could Create Opportunities

I am not treating this week as a reason to panic.

I am treating it as a reason to prepare.

The real opportunity this week may not come from predicting the inflation number perfectly.

It may not come from guessing exactly what the Fed will do.

And it may not come from chasing the SpaceX IPO.

The real opportunity may come from watching which high-quality stocks get dragged down unfairly.

That is what I am focused on.

If a weak business falls, that is not automatically an opportunity.

But if a high-quality company with strong cash flows, a durable competitive advantage, and a reasonable valuation falls simply because the market is under pressure, that is where things can get interesting.

Volatility only helps you if you already know what you want to own.

That is why I prefer to build watchlists before the panic.

Not during it.

What I Am Watching Now

This week, I am watching four things closely.

First, inflation.

If inflation comes in hotter than expected, higher-for-longer rate fears could return very quickly.

Second, bond yields.

If yields keep moving higher, expensive growth stocks may remain under pressure.

Third, AI leadership.

If the AI winners keep selling off, the market may start questioning whether valuations have moved too far ahead of fundamentals.

Fourth, market breadth.

If more stocks begin participating while mega-cap tech cools off, that could be a healthy sign.

But if the weakness spreads from tech into everything else, then the market may have a bigger problem.

Final Thoughts

This is a huge week for the stock market.

Inflation is back in focus.

Interest rates are back in focus.

AI valuations are back in focus.

And the SpaceX IPO is arriving as one of the biggest tests of investor appetite for extreme growth stories.

The business may be incredible.

The story may be exciting.

The long-term potential may be huge.

But the price still matters.

That is the lesson investors cannot forget.

A great company can still be a poor investment if the valuation already assumes perfection.

And in a market where fear is rising, rates are shifting, and crowded technology trades are under pressure, valuation discipline becomes more important, not less.

My plan is simple.

I am staying patient.

I am staying selective.

And if volatility creates opportunities in high-quality businesses, I want to be ready.

Because the best opportunities usually appear when the market gets emotional.

And this week, there is a real chance the market gives investors a lot to think about.

For the free section, I wanted to focus on the bigger market setup: inflation, rates, AI valuations, and why the SpaceX IPO could become a major test of investor appetite.

For paid subscribers, I want to go one step further and look at the actual stocks I would rather watch than chase the SpaceX IPO.