Visa, Mastercard or Amex? I’d Only Buy One Today

I ranked all three by valuation, downside risk, dividend growth, future protection, and their odds of outperforming the S&P 500 over the next decade.

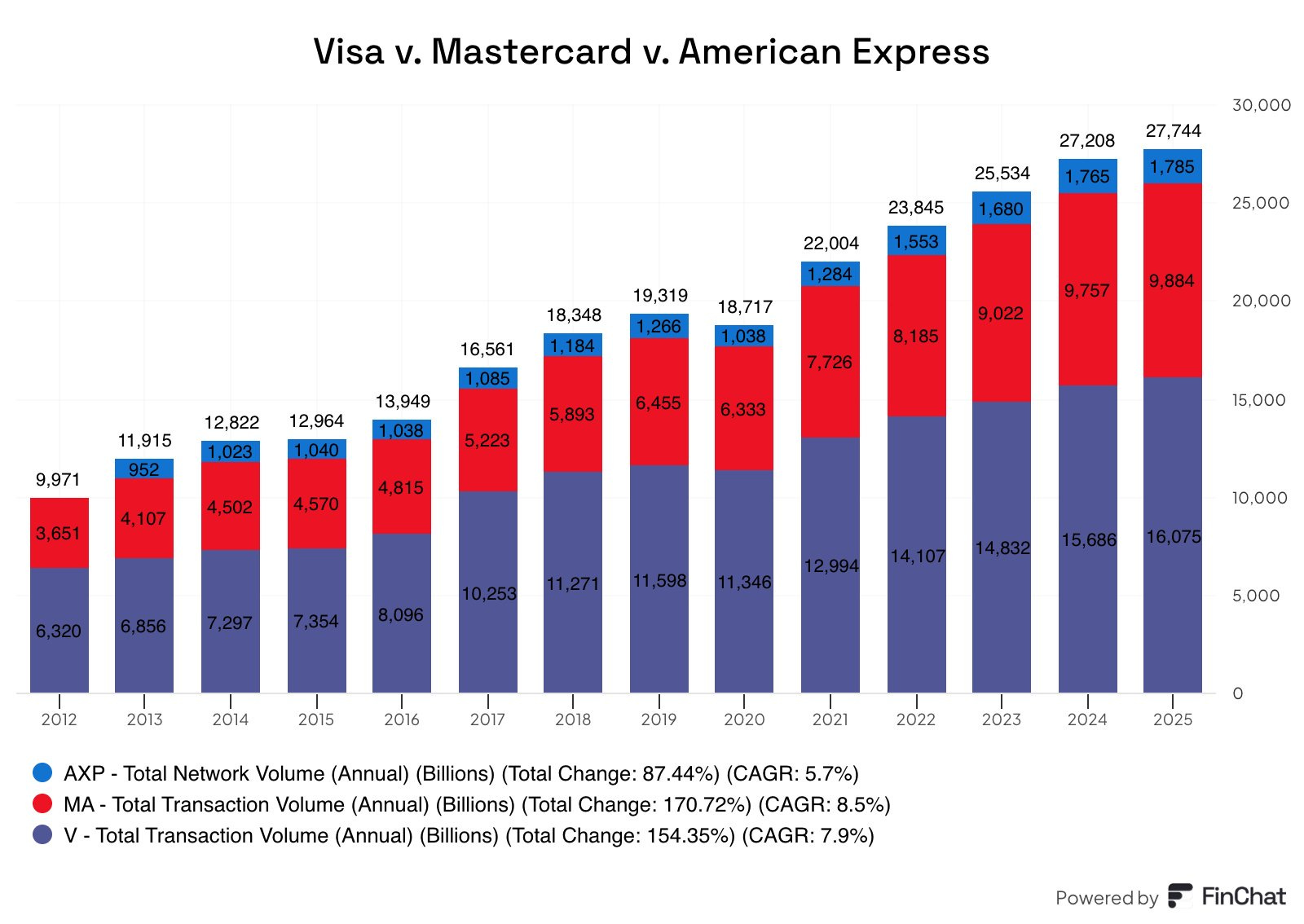

Visa, Mastercard and American Express are often grouped together as “payment stocks.”

But that description undersells what these businesses really are.

And with Visa and Mastercard both reporting earnings this week, this comparison feels especially timely.

Investors are about to get a fresh look at payment volumes, cross-border spending, consumer resilience, margins, and whether these premium valuations are still justified.

But short-term earnings are only part of the story.

The bigger question is far more important:

If I could only buy one of these three payment giants today, which one offers the best mix of quality, future protection, valuation, dividend growth, and long-term market-beating potential?

At their best, these companies are not just exposed to consumer spending.

They sit underneath global commerce itself.

Every time someone taps a card, pays online, books a hotel, buys groceries, travels abroad, pays for software, or spends through a digital wallet, one of these networks can benefit.

That is what makes this group so powerful.

These are not ordinary financial companies. They are some of the most entrenched businesses in global payments, supported by scale, trust, acceptance, brand power, and the long-term shift away from cash.

And that long-term trend is still visible in the numbers.

Payment volumes have continued to climb over time, even through recessions, inflation shocks, rate cycles, and major changes in consumer behaviour.

That is the appeal of this group.

As more spending moves away from cash and into digital payment networks, Visa, Mastercard and American Express all have a structural tailwind behind them.

But here is where investors need to be careful.

One of the biggest mistakes investors can make is treating Visa, Mastercard and American Express as interchangeable businesses.

They are not.

Visa and Mastercard are open-loop payment networks. They sit between banks, merchants and consumers, processing enormous transaction volumes without taking the same direct lending risk as a card issuer.

American Express is different.

Amex operates a closed-loop model, meaning it acts as the network, the issuer, and the relationship owner. That gives American Express more control over the customer relationship, especially with affluent consumers, but it also gives the business more exposure to credit cycles, lending risk, and consumer stress.

That difference matters.

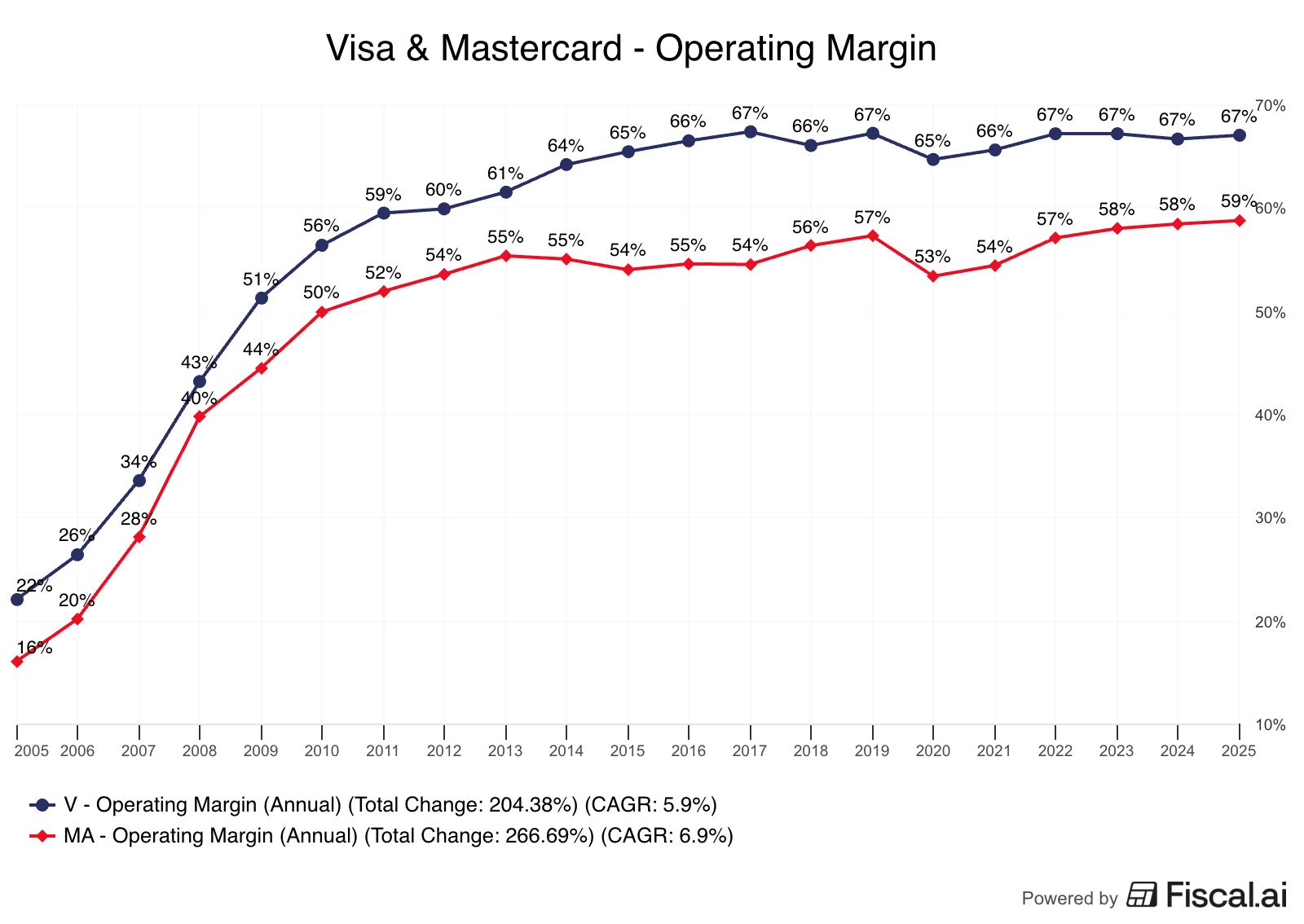

Visa and Mastercard often look more like global toll roads than traditional financial companies. They benefit from scale, network effects, and high incremental margins, without carrying the same balance-sheet risk as a lender.

That is why their profitability profile is so exceptional.

Very few businesses can sustain margins like this over long periods of time.

And that is exactly why Visa and Mastercard usually trade at premium valuations.

The market knows these are exceptional businesses.

American Express is different again.

It does not have the same pure toll-road model as Visa or Mastercard, but it does have a powerful premium brand, a loyal customer base, and a closed-loop network that gives it deeper insight into both cardholders and merchants.

That can be a real advantage.

But it also means the stock needs to be judged differently.

So this comparison is not simply about asking which company is “best.”

A great business can still be a poor investment if too much optimism is already priced in.

And a cheaper stock can still be a value trap if the market is correctly discounting higher risk.

That is why I wanted to compare Visa, Mastercard and American Express through the lens that actually matters for investors today:

Business quality

Future protection

Downside and recession risk

Dividend growth potential

Current valuation

Potential to outperform the S&P 500 over the next decade

Each company has a different strength.

Visa may be the safest and most predictable.

Mastercard may be the strongest long-term compounder.

American Express may look like the obvious bargain.

But once I adjusted for business model, credit exposure, valuation, dividend growth and downside risk, only one stood out as the stock I would be most willing to buy today.

Paid members get the full ranking, valuation breakdown, buy zones, downside risks, and my top pick today.