How I Find Dividend Stocks That Can Beat the S&P 500

My step-by-step framework for separating quality income stocks from dividend traps

Most dividend investors don’t underperform because they pick bad companies.

They underperform because they pick:

stable businesses

with decent yields

at the wrong price…

with the wrong balance sheet…

and limited upside.

Over time, that combination quietly lags the S&P 500.

Over the last 20 years:

- The S&P 500 returned ~7.5% annually

- The average investor achieved just ~2.9%

That gap isn’t about access.

It’s about decision-making.

So the goal isn’t just to find “good dividend stocks”.

The goal is to find:

dividend stocks that compound capital AND income - while being mispriced today

That’s a very different filter.

In this article, I’ll walk through the full framework I use - the same one behind my recent screen:

Here’s the exact framework I use to find dividend stocks that can actually outperform the S&P 500 - not just provide income.

Over the last 12 months, applying this framework has consistently led me toward:

- Companies trading below historical valuation ranges

- Businesses with stronger balance sheets than peers

- Stocks with clear upside vs current expectations

In fact, in my latest screen:

119 stocks → 30 qualified → just 5 stood out.

That’s less than 5% of the market.

That’s the level of selectivity required to outperform.

Step 1: Start With Total Return - Not Yield

This is where most investors go wrong.

They optimise for:

Yield

Dividend history

Stability

But the market doesn’t reward yield.

It rewards:

earnings growth + multiple expansion

Dividend is just a component of total return.

So the first question I always ask is:

👉 “Can this business outperform the S&P 500 from here?”

If the answer is unclear - I move on.

Step 2: Growth Drives Everything (Even for Dividend Stocks)

A dividend stock without growth becomes a bond proxy.

That means:

Limited upside

High sensitivity to rates

Underperformance in strong markets

So I focus on:

What actually matters:

5–10Y revenue CAGR

EPS growth consistency

Margin expansion (or stability)

What I avoid:

Flat revenue + “financial engineering” EPS

Cyclical spikes mistaken for growth

Because over time:

growth is what drives both dividend increases AND valuation rerating

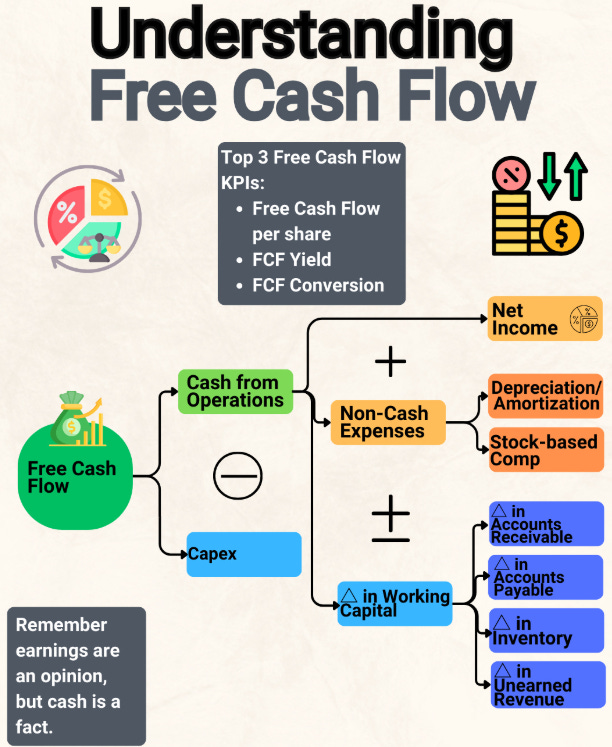

Step 3: Free Cash Flow Is the Truth

Earnings can be managed.

Cash flow is harder to fake.

Free cash flow tells you what a business actually generates after reinvestment.

It strips away accounting noise and shows:

- what’s real

- what’s sustainable

- and what can actually fund dividends

At a basic level:

This is why I always prioritise:

- consistent FCF generation

- strong FCF conversion (earnings → cash)

- and coverage of the dividend

Because when cash flow weakens, the dividend is usually next.

This is one of the biggest edges most investors ignore.

I look for:

Consistent free cash flow generation

FCF growing faster than dividends

Low conversion risk (i.e. earnings ≈ cash)

Why this matters:

A company can:

look cheap on P/E

show a “safe” payout ratio

…but still be at risk if cash flow doesn’t support it.

This is exactly how dividend cuts catch people off guard.

Step 4: The Balance Sheet (This Is Where Most Investors Fail)

This is the part most investors underestimate - until it’s too late.

Two companies can look identical on valuation…

But have completely different risk profiles based on:

Debt levels

Refinancing timelines

Interest coverage

Liquidity

This is why I always stress:

The balance sheet matters more than valuation

I broke this down in detail here:

If you ignore this step, you’re not investing - you’re guessing.

Step 5: Dividend Safety ≠ Dividend Yield

High yield is often a warning sign, not an opportunity.

Instead, I focus on:

FCF payout ratio (not earnings)

Stability of the underlying business

Capital allocation discipline

Because:

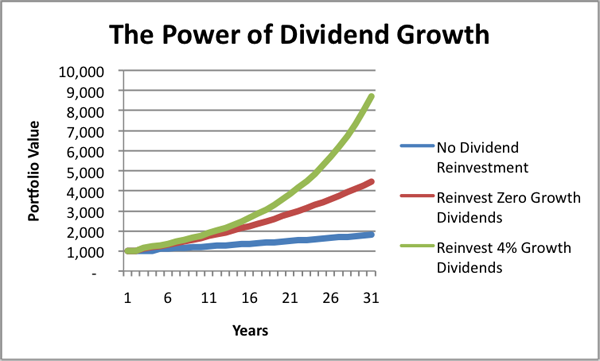

a growing 2–4% yield will outperform a declining 7% yield over time

This is what most investors underestimate.

It’s not the starting yield that matters -

it’s what that yield becomes over time.

The difference comes from:

- underlying business growth

- cash flow expansion

- and the ability to consistently increase the dividend

This is why I prioritise dividend safety and growth over headline yield.

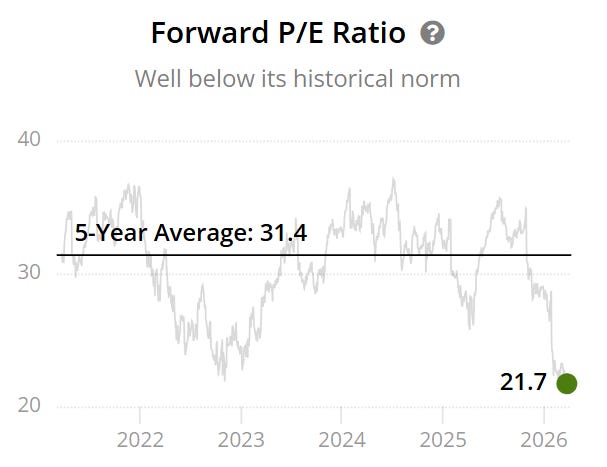

Step 6: Valuation - The Actual Driver of Outperformance

This is where everything comes together.

Even the best companies underperform if you overpay.

So I compare:

Forward P/E vs 5-year average

FCF multiple vs historical range

Current sentiment vs fundamentals

What I’m really looking for is:

valuation compression in high-quality businesses

This is what valuation compression looks like in practice.

A high-quality business…

trading well below its historical multiple.

Nothing about the business has fundamentally broken.

But sentiment has changed - and the multiple has compressed.

That’s where the opportunity comes from.

Because if the business continues to perform…

the valuation doesn’t need to expand much for strong returns.

That’s where asymmetry exists:

downside protected by quality

upside driven by rerating

Step 7: Expectations vs Reality (The Final Filter)

Stocks don’t move based on what is happening.

They move based on:

what changes vs expectations

So I always ask:

What does the market expect today?

What would need to go right for upside?

What is already priced in?

This is where the edge comes from.

Putting It All Together

When a stock meets all of these criteria, you get:

Growth

Cash flow strength

Balance sheet resilience

Dividend safety

Attractive valuation

Mispriced expectations

That’s the combination that can:

outperform the S&P 500 - not just match it

So the real question is:

👉 Which dividend stocks actually pass all 7 filters today?

Because most don’t.

When I applied this framework across 119 stocks:

- Only 30 made it through

- Just 5 ranked highest for risk-adjusted upside

These aren’t just “good dividend stocks” -

they’re the ones where valuation, balance sheet, and expectations all align.

Instead of repeating the picks here, I’ve already broken that down in full detail.

Most investors won’t look this deep.

That’s where the edge comes from.

If you want to find dividend stocks that can actually outperform the market - not just generate income - that’s exactly what I focus on inside the paid newsletter.

Each month, I break down:

- The few stocks that actually pass this framework

- Where the market is mispricing risk vs upside

- Which opportunities I have the highest conviction in

You don’t need more stock ideas.

You need a better way to filter them.

That’s what this gives you.

Most investors don’t underperform because they lack access.

They underperform because they lack a framework.

This is mine.

What you get as a paid subscriber:

Monthly stock screens (like this one)

Full valuation models (DCF + comps)

Buy / Hold / Avoid ratings

Positioning + conviction levels

If this helped you, share it:

If you found this framework useful, feel free to share it with others:

👉 Share this post

👉 Forward to a friend

It helps more than you think.