Revenue Is Vanity. Margins Are Reality.

Why most high-growth companies aren’t actually strong — and the one metric that reveals it instantly.

Markets reward growth.

But they reward quality of growth even more.

And most investors don’t know the difference.

They focus on:

revenue growth

EPS beats

headline numbers

All useful.

None sufficient.

Because none of them answer the question that actually matters:

Is this business structurally strong - or just temporarily growing?

That answer doesn’t sit in the headline numbers.

It sits in the income statement - and more importantly, how you read it.

Why Growth Alone Misleads

In strong markets, growth covers everything.

weak margins get ignored

inefficient businesses get rewarded

capital discipline disappears

Because:

Growth creates the illusion of strength.

But margins reveal the truth.

And when conditions tighten, reality shows up fast.

Not gradually.

All at once.

Two companies can grow at the same rate:

same revenue

same narrative

same investor excitement

But produce completely different outcomes.

The difference is simple:

One converts growth into profit.

The other converts growth into cost.

The 10-Second Income Statement Test

If I only had a few seconds to assess a business, I’d look at one thing first:

Operating Margin Trend

Not the level.

The direction.

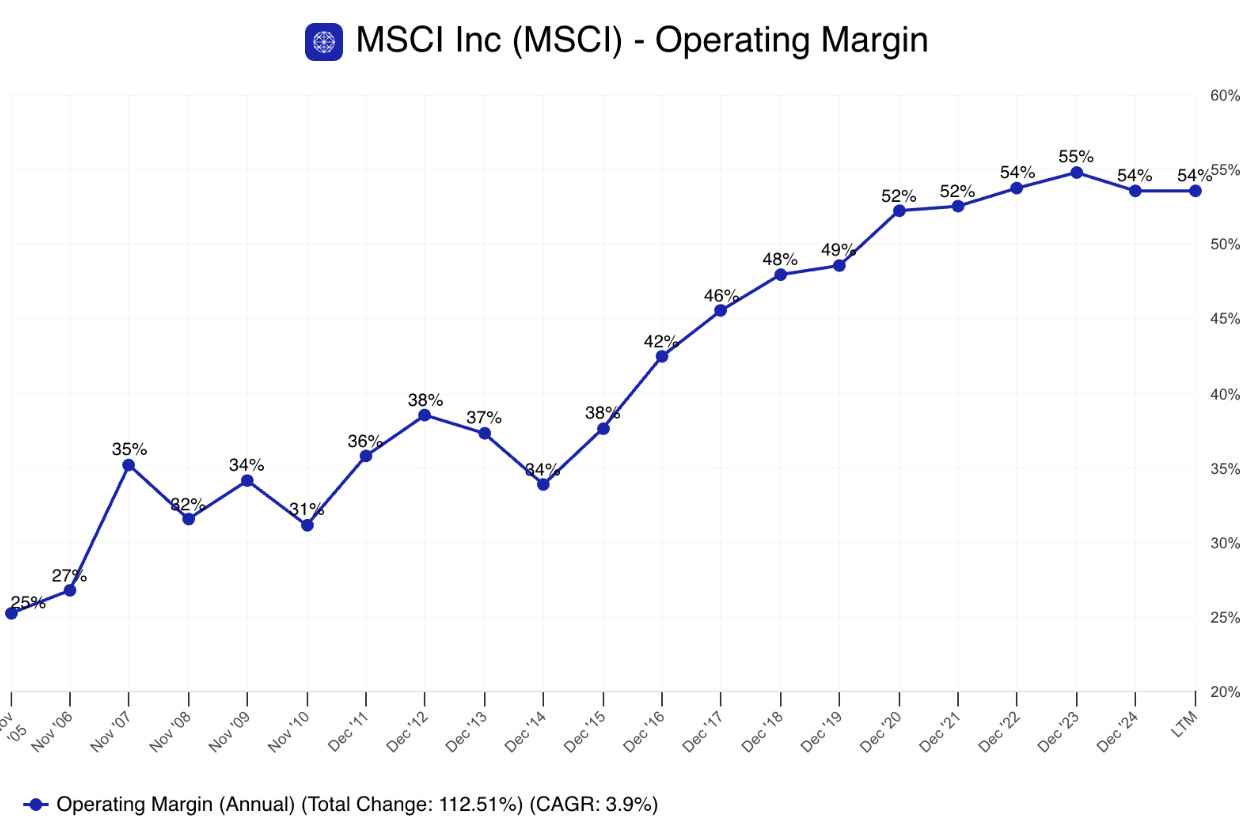

This is what strength looks like: margins expanding over time, not just revenue growing.

Simple framework:

Expanding margins → strength

Flat margins → stability (but limited upside)

Declining margins → early warning sign

Why this matters:

Margins tell you what happens after growth.

Anyone can grow revenue.

Very few businesses can grow profitably - and sustain it.

Revenue Quality (Not All Growth Is Equal)

One of the biggest mistakes investors make:

Treating all revenue growth as the same.

It isn’t.

Ask three questions:

1. Is it organic?

Or driven by acquisitions?

Growth through acquisition often looks strong…

…but comes with:

integration risk

higher costs

lower visibility

2. Is it pricing or volume?

Pricing power → strength

Volume-driven growth → often cyclical

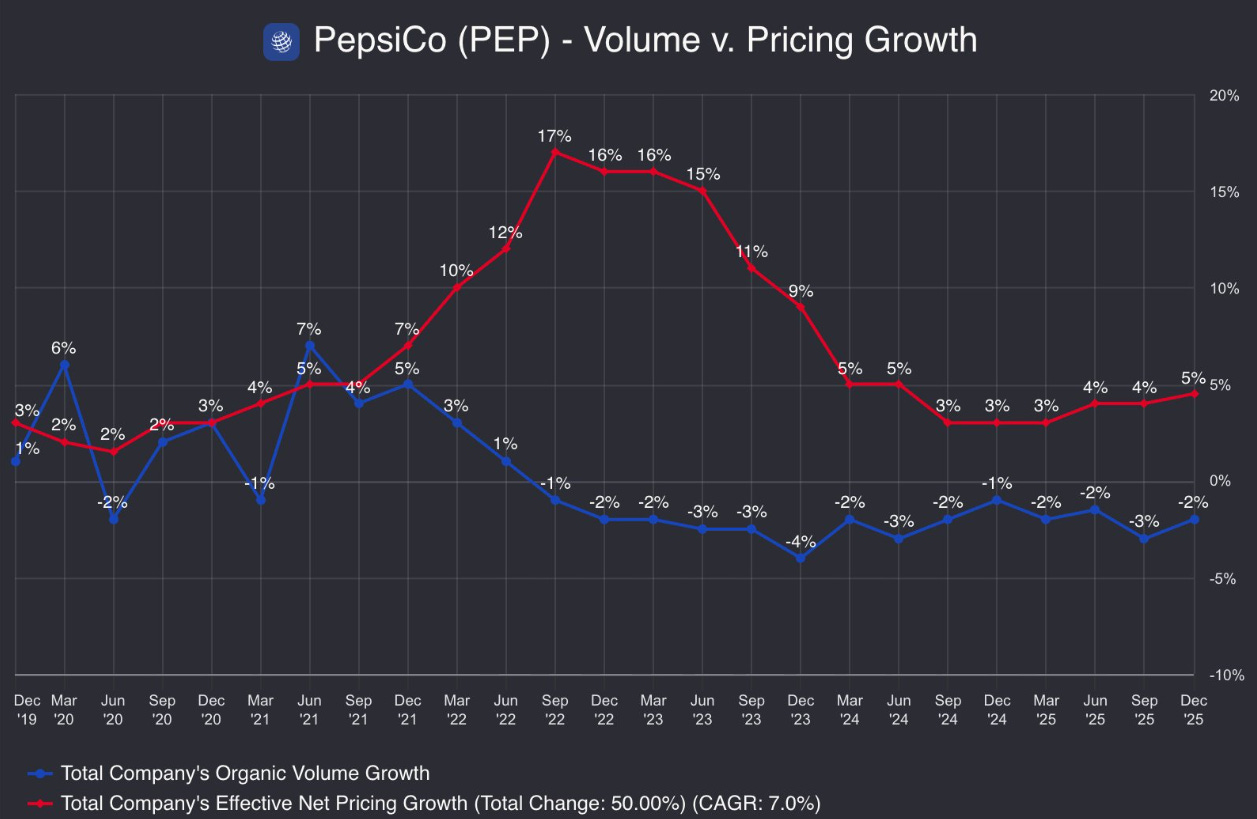

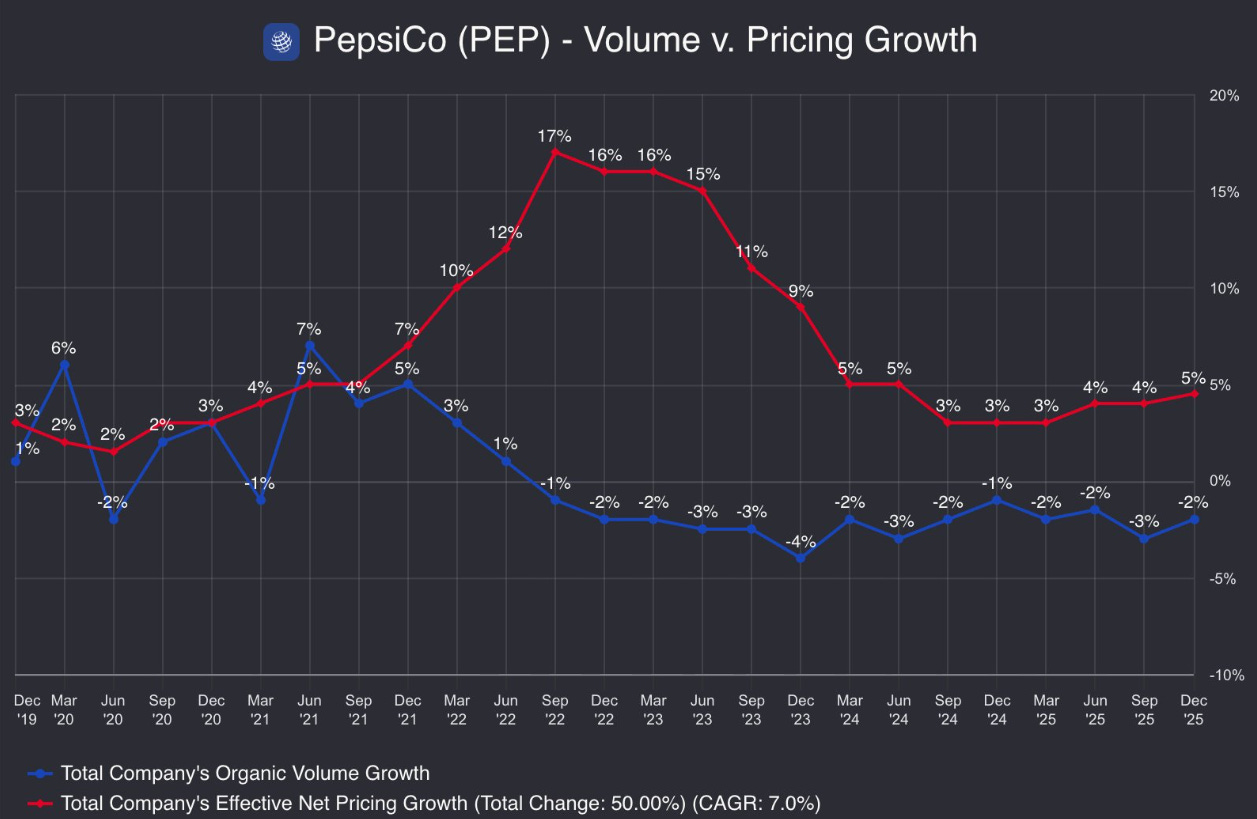

This is pricing-led growth - strong in the short term, but harder to sustain than volume-driven expansion.

3. Is it durable?

subscription / recurring → high quality

one-off / project-based → less predictable

Adobe’s shift to subscription revenue created predictable, recurring growth - this is what durability looks like.

👉 Key idea:

Good businesses grow. Great businesses grow predictably.

Margins: Where the Truth Lives

Revenue tells you what a company sells.

Margins tell you how good the business actually is.

Break it down simply:

Gross Margin → Product Strength

High = pricing power

Low = commoditised / competitive

High and rising gross margins like this typically signal pricing power - not commoditisation.

Operating Margin → Business Model

Efficiency

scalability

cost discipline

Net Margin → Financial Structure

interest costs

tax

capital decisions

But if you had to pick one?

👉 Operating margin tells you the most.

Because it reflects:

How well the business converts revenue into real operating profit.

When Growth Becomes a Problem

Here’s where most investors get caught:

Revenue is growing… but margins are falling.

This is the trap: growth looks strong - but the business is getting weaker.

This usually means:

rising costs

competitive pressure

over-expansion

weakening pricing power

And this is the key shift:

Growth stops being a tailwind…

and starts masking deterioration.

That’s when you see:

earnings misses

multiple compression

sudden repricing

Not because the business collapsed.

But because:

The quality of growth was never there.

Earnings Quality (This Is Where It Gets Missed)

Even margins don’t tell the full story.

Because:

Earnings ≠ cash flow

A company can look profitable…

…but still not generate real cash.

Look for:

stock-based compensation

“adjusted” earnings

one-off add-backs

capitalised costs

👉 Key idea:

If earnings require explanation, they’re usually weaker than they look.

Connecting This to the Balance Sheet

This is where most investors stop.

And where mistakes happen.

The income statement tells you:

Is this business strong?

The balance sheet tells you:

Can it survive if it isn’t?

If you haven’t read it yet, this is the framework I use to assess risk in under 60 seconds:

You need both.

Because:

strong margins with weak balance sheets → fragile

strong balance sheets with weak margins → stagnant

But when both align:

You get durability and upside.

Bringing It Together

A strong business isn’t defined by growth.

It’s defined by alignment:

high-quality revenue

expanding (or stable) margins

clean earnings

resilient balance sheet

When all four are present:

The business compounds.

When they aren’t:

Growth becomes noise.

The Real Risk Isn’t Slow Growth

It’s misleading growth.

Because that’s what causes:

overvaluation

misplaced confidence

permanent capital loss

A Better Way to Think About It

Most investors ask:

“How fast is this company growing?”

A better question is:

“How much of that growth actually turns into profit?”

Because that’s what drives:

valuation

durability

long-term returns

How I Apply This in Practice

This is exactly why, in my monthly screens:

I don’t just look for:

revenue growth

or cheap valuations

Every company must show:

strong or improving margins

durable earnings

and a resilient balance sheet

Because:

Upside without quality isn’t opportunity.

It’s risk.

What This Looks Like Right Now

In my latest screen:

119 companies analysed

30 passed initial filters

a smaller group met my execution threshold

From those:

👉 Five stand out most clearly.

Not just because of upside -

but because downside is controlled.

👉 If you’re allocating real capital,

entry price matters.

downside matters.

and quality determines outcomes.

Unlock the Full Breakdown

🔒 Paid members get access to:

Top 5 ranked stocks

Exact buy ranges

Downside modelling

Full 30-stock dataset

Allocation framework

Final Thought

Growth gets attention.

Margins determine outcomes.

And over time:

The market rewards businesses that convert growth into profit - consistently.

Markets reward discipline.

Not growth. Not narratives. Not hype.

👉 If you found this valuable, consider subscribing to get the full monthly reports and future frameworks.

Subscribe to Dividend Talks

Get:

Monthly valuation screens

High-upside stock ideas

Deep-dive frameworks like this

I really like your posts! I subscribe to your service. How do i receive your spreadsheets? Keep up the good work!!

Thanks for the post, I enjoyed it. What about the cash flow statement and FCF margins? Do you think they are more important than op margins?